Latest operating output statistics review:

Domestic routes downturned slightly while international routes continued to grow in December.

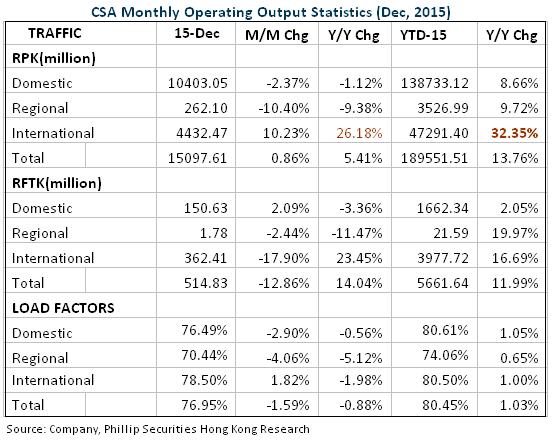

In December, as driven by the high growth rate of international routes, the RPK (revenue passenger kilometres) of passenger traffic of China Southern Airlines (CSA) increased by 5.4% yoy; of which international routes continued to grow significantly while domestic routes downturned slightly and regional routes declined apparently. Due to the low-season of airline industry and the high comparison benchmark of the previous year, passenger load factor dropped by 0.9 ppts to 77%. Except the 1.8 ppts mom increase for international routes, other data demonstrated certain downturn generally.

Annual passenger traffic grew by 13.8% yoy

RPK recorded in 2015 increased by 13.8% yoy, of which the growth for international routes was significant, while domestic routes and regional routes kept steady growth. With the Company's effort spent on developing international routes for years, their proportion now reaches a quarter of the total RPK. The allocation of capacity basically matched market demand for the whole year. The overall passenger load factor grew by 1 ppts to 80.5%. International routes, domestic routes and regional routes recorded growth of 1 ppt, 1.05 ppts and 0.65 ppts respectively, to 80.5%, 80.6% and 74.1% respectively.

Investment thesis

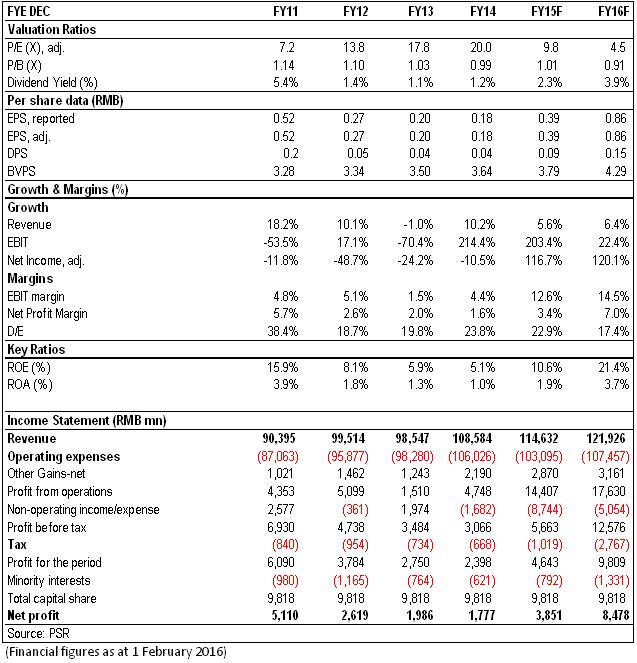

CSA issued a positive profit alert, and the net profit for the year 2015 is expected to increase 110% to 130% yoy to 3.7billion to 4.1billion, which means the 15Q4 turn to net loss of 0.58billion to 0.93billion. Affected by the depreciation of RMB, the Q3 results of CSA (RMB1.17 billion) shrank 50% in comparison to the same period last year (RMB2.274 billion), and dragged down the profit growth for the first nine months of 2015. The Company recorded a profit of RMB4.66 billion, which increased 2.7x yoy. Overall, we adjusted the Company's EPS forecast of 2015/2016 to RMB0.39/0.86, and accordingly marked down target price to HKD5.66, which is based on 1.25x/1.12x of eP/B and 12x/5.6x of eP/E for the two years, but upgrade rating as ¡§BUY¡¨. (Closing price as at 1 FEB 2016)

Spending big sum on purchasing aircrafts in order to enhance capacity

In order to satisfy the growing demand of air travel, CSA's plan of substantial expansion of transportation capacity is progressing. According to a recent announcement by the Company, CSA will purchase 110 units of Boeing 737 aircrafts (30 units of NG series and 80 units of MAX series) and 10 units of A330-300 aircrafts. Meanwhile, CSA will sell 13 units of Boeing 757 aircrafts, 3 units of Boeing 737 aircrafts, and some of the aircraft parts. According to the price on catalog, these two transactions will involve approximately USD10.1 billion and USD2.27 billion respectively. Yet, we considered such purchase as a bulk purchase and thus CSA's actual cost of purchase should be far lower than the price announced. New aircrafts will be delivered successively between 2017 and 2021. By then the total transportation capacity of the Company would increase by about 20% and the composition of aircraft fleet would be further upgraded.

Spring Festival effect and outbound travel are CSA's two major long-term focuses

CSA has the highest number of domestic routes among the three major Chinese airlines and is the least affected by the speed enhancement of Beijing-Shanghai express rail. Therefore, CSA is benefited the most from the strong seasonal demand of Spring Festival. Meanwhile, the Company's routes to Australia and South-east Asia were popular among outbound leisure passengers. In view of the depreciation of currencies in the above regions, increase of consumption power of passengers, and sufficient transportation capacity of the Company, prosperous development of outbound air travel can have bright prospect amid slowdown of macro-economic growth.

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Irrational inter-industrial price war;

Financials

Click Here for PDF format...