Summary

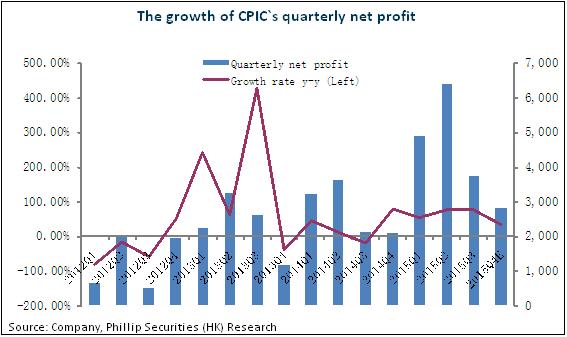

-CPIC (or the Group) maintained the strong growth in 2015. According to the latest announcement, as at the end of Dec 2015, the Group's net profit amounted to RMB17.8 billion compared with that of 2014, up 60% y-y approximately, better than our previous expectation;

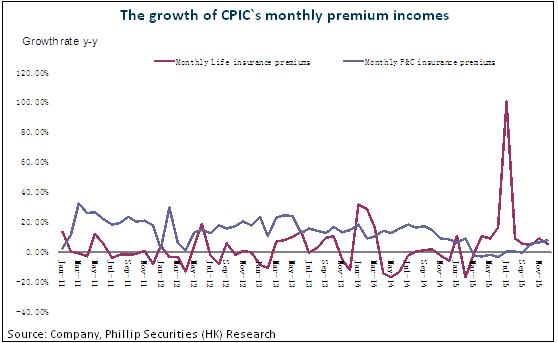

-According to CIRC's records, CPIC's accumulated premiums of life insurance and P&C insurance amounted to RMB203 billion , increased by 6% y-y. The strong net profit growth was mainly benefited from the large increase of investment gains in 2015;

-Considering the Group's stable operating performance in 2015 and the current price is low, the valuation becomes attractive, and we still hold the positive view on CPIC's future performance. We decrease the 12-m TP to HK$35.00 to reflect the current market risks, around 32% higher than the latest closing price, equivalent to 10.8xP/E and 1.7xP/B in 2016E respectively. Maintain at Buy rating. (Closing price as at 28 Jan 2016)

The strong growth of investment gains

According to CIRC's records, as at the end of Dec 2015, CPIC's accumulated premiums of life insurance and P&C insurance amounted to RMB203 billion , increased by 6% y-y. The premiums of life insurance and P&C insurance businesses increased by 5.34% y-y and 8.13% y-y to RMB4.614 billion and 9.045 billion respectively. The strong net profit growth was mainly benefited from the large increase of investment gains in 2015. By the end of 3Q, investment gains increased by 53.6% y-y to RMB43.83 billion, and we expect it should increase by around 60%-70% y-y in 2015.

According to the latest announcement, by the end of 2015, the Group's net profit amounted to RMB17.8 billion compared with that of 2014, up 60% y-y approximately, better than our previous expectation, and we will discuss it in details after the official announcement of annual results.

Risk

The growth might be lower than our expectation due to the large volatility of investment gains;

Share price drops obviously in the short run due to the deterioration of the market environment.

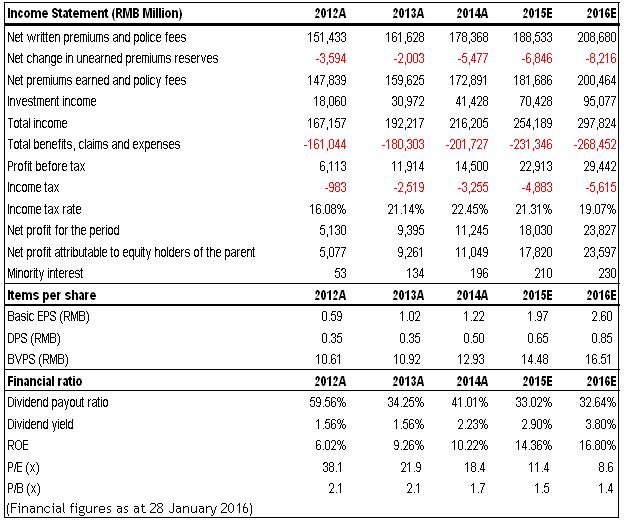

Financials

Click Here for PDF format...