Benefitted from the construction of 4G network and speed enhancement of optical fiber broadband by the domestic telecommunication operators, the revenue from telecommunications infrastructure service of China Communications services (CCS) in 1H15 surged 16.6% to RMB 18 billion, the total revenue increased by 11.3% to RMB 37.6 billion. Being adversely affected by the increase of labor cost, the Company's gross profit margin dropped by 0.5 ppts to 13.8%. It is mainly due to the significant increase of subcontracting cost as 21.4%, which marked as the highest level since the same period in 2012. Therefore, net profit attributable to shareholders in 1H15 only increased slightly by 2.7% to RMB 1.27 billion, with basic EPS recorded as RMB 0.184.

As a fundamental industry supporting economic restructuring, we believe the IT industry would continually receive policy support and the Company would also be benefitted. The former Chairman of China Telecom, Wang Xiaochu, was transferred to China Unicom. This may help the Company to gain more orders from China Unicom. Moreover, China Tower has basically completed the acquisition of telecommunication tower assets from the top three telecommunication operators. It may bring new opportunities for CCS's business development. Meanwhile, the overseas market would become one of the growth momentums in the future.

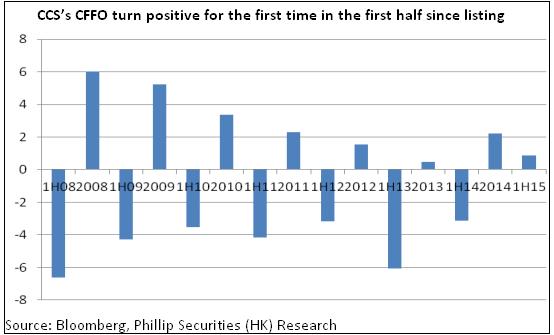

We expect improvement in the upcoming future: Firstly, the rate of increase of subcontracting charge has been too high in recent years. Such pressure may be eased with the release of bonus to domestic engineers. Secondly, through strict cost control, the overall growth of other cost items of the Company is mild, which effectively offset the pressure from the increase of subcontracting charge. Moreover, the Company continued to strengthen the management of operating capital, the cash flow of operating activities in 1H15 recorded a positive figure, which is the first time in the first half year since listing. The financial condition of the Company is getting healthier, so the financial costs may decrease.

Growth prospect still expectable, with valuation under-estimated

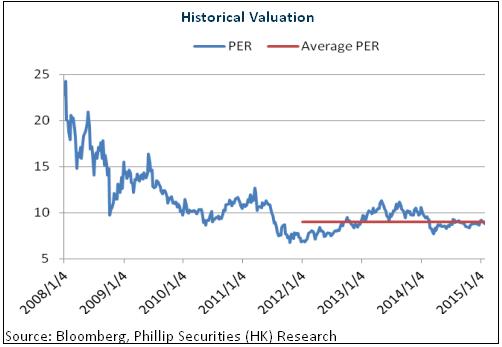

China will speed up construct communication networks, the overseas business may also become growth momentum gradually for CCS. In addition, persistent decline of profitability is unlikely and thus we consider the Company will keep steady growth. The Company's range of P/E ratios has gradually dropped from 10.6x in 2010-2011 to 9x since 2012. We set the 12-month target price as HKD 4.18, based on the valuation corresponding to 10x 2015e EPS, and maintain the rating of ¡§Buy¡¨. (Closing price as at 24 Nov 2015)

High subcontracting charges affected performance growth

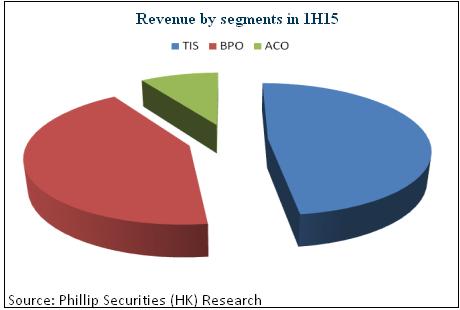

Benefitted from the construction of 4G network and speed enhancement of optical fiber broadband by the domestic telecommunication operators, the revenue from telecommunications infrastructure service of CCS in 1H15 surged 16.6% to RMB 18 billion. However, the revenue from business process outsourcing services only grew by 7.6% to RMB 16.1 billion; while the income from a variety of other services including applications, content and others even merely grew by 3.3% yoy to RMB 3.5 billion. In sum, the Company's total revenue only increased by 11.3% to RMB 37.6 billion, which was slightly lower than our expectation.

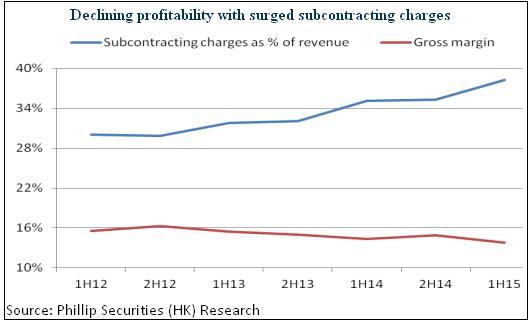

What's more, being adversely affected by the increase of labor cost, the Company's gross profit margin dropped by 0.5 ppts to 13.8%. It is mainly due to the significant increase of subcontracting cost as 21.4%, which marked as the highest level since the same period in 2012. The proportion of subcontracting cost in total revenue also moved up 3.2 ppts, from 35.1% in the same period last year increased to 38.3%. Such figure is far higher than that recorded in 2012 which was approximately 30%. Therefore, net profit attributable to shareholders in 1H15 only increased slightly by 2.7% to RMB 1.27 billion, with basic EPS recorded as RMB 0.184.

TIS business will still keep growing fast

As a fundamental industry supporting economic restructuring, we believe the IT industry would continually receive policy support and the Company would also be benefitted. Recently, NDRC pointed out the need to speed up the nurturing of strategical newly-emerged industries so as to shape them as key driving forces of economic development, and to create a new generation of five emerging pillar industries of ¡§ten trillion class¡¨, covering information technology, high-end equipment and materials, digital innovations etc. Specifically, in medium-/short- term, after the issuance of FDD license, China Telecom and China Unicom will also speed up the construction of 4G network. It is worth to note that the former Chairman of China Telecom, Wang Xiaochu, was transferred to China Unicom. This may help the Company to gain more orders from China Unicom. Moreover, China Tower has basically completed the acquisition of telecommunication tower assets from the top three telecommunication operators. It may bring new opportunities for CCS's business development. Previously, the Company has signed cooperation agreement with the ten provincial-level subsidiaries of China Tower.

It is also worth to point out that overseas market would become one of the growth momentums in the future. The Chinese Government supports the overseas development of advantageous industries including high-speed rail, nuclear power, aviation and telecommunications, to satisfy the market demand overseas. Particularly in markets with relatively backward telecommunication infrastructure, for example South-east Asia, South America, Middle East and Africa etc, the market demand is huge. CCS has comparative advantages in telecommunications infrastructure, and it is expected to be benefitted from the policies including ¡§One Belt and One Road¡¨. However, revenue from overseas in 1H15 decreased 9.2% yoy, with its proportion in total revenue dropped from 5.2% recorded in the same period last year to 4.2%. It is expected to resume to the level of approximately 5%, and further increase to more than 10% in long term.

Persistent decline of profitability unlikely

Being adversely affected by the pressures from the increase of outsourcing low-end business and labor cost, the Company's profitability in recent years declined continually. However, we expect improvement in the upcoming future: Firstly, the rate of increase of subcontracting charge has been too high in recent years. Such pressure may be eased with the release of bonus to domestic engineers. Secondly, through strict cost control, the overall growth of other cost items of the Company is mild, which effectively offset the pressure from the increase of subcontracting charge. Since 2012, even though the proportion of subcontracting cost to revenue increased by more than 8 ppts, the proportion of total cost to revenue merely increased about 2 ppts. The Company's decrease of EBIT profit margin also dropped from the previous 0.5 ppts to the current 0.2 ppts.

Moreover, the Company continued to strengthen the management of operating capital, changing the previous trend of uprising. Cash flow of operating activities in 1H15 recorded a positive figure, which is the first time in the first half year since listing. The financial condition of the Company is getting healthier, so the financial costs may decrease.

Catalyst

4G projects are released faster than expected;

Development of overseas projects beats expectation.

Risks

Profitability continues to decline significantly;

Political and exchange rate risks of overseas projects.

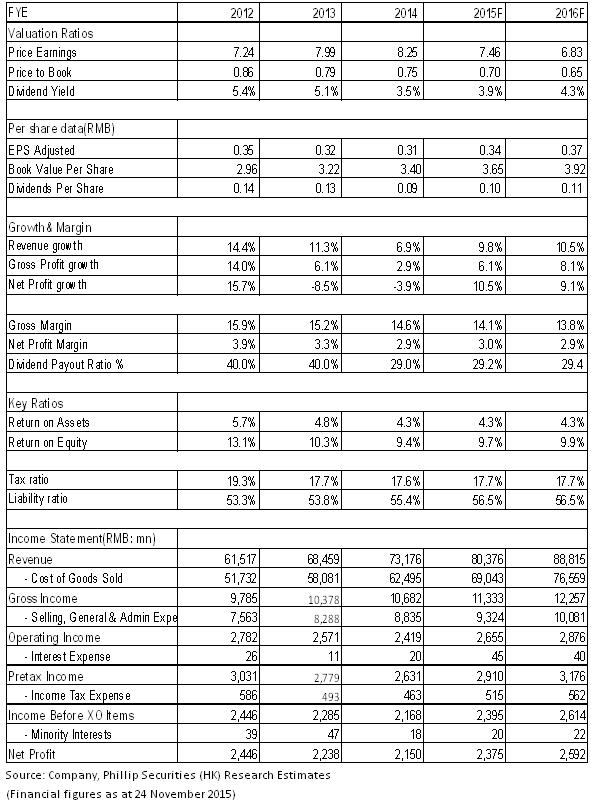

Financials

Click Here for PDF format...