|

|

|

*Advertisement* |

|

|

|

|

|

23 Nov, 2015 (Monday) |

|

|

SAMSONITE(1910)

Analysis¡G

With the condition of fixed exchange rate, Samsonite`s sales turnover in Q3 grew by 9.3% yoy to USD 624 million. If sales turnover of the Gregory brand, which was acquired by Samsonite in July 2014, is excluded, then the growth rate of sales turnover in Q3 would be 8.5%. Meanwhile, with the USD being strong, the Q3 sales turnover which is denominated in USD dropped 0.6% yoy. Samsonite`s four major intercontinental business segments kept their growth in Q3. Sales turnover recorded in Asia, North America, Europe and Latin America grew 10.1%, 2.2%, 18.7%, and 2.3% respectively. Contributions of income from sales recorded in in Asia, North America, Europe and Latin America amounted to 39.3%, 32.1%, 24.2% and 4.1% respectively. In the period under review, the double-digit growth rate recorded in Asia and Europe effectively boosted the overall business results of the Company. Samsonite diversifies its products and brands combination through acquisitions. Such act effectively increased the Company`s competitiveness. The Company`s solid balance sheet is contributed by lower financial leverage, limited capital expenditure and sufficient cash flow, and it would definitely bring more comparative advantages to the Company. We certainly need to be cautious and objective towards the difficulties brought by the consolidation of diversified business, and the operation risk caused by the uncertainty of global economic growth. We maintain the rating of ¡§Accumulate¡¨ and adjust the 12-month target price slightly downward to HKD28, which is equivalent to 21x and 19x of the prospective P/E in 2015/2016.

Strategy¡G

Buy-in Price: $23.40, Target Price: $28.00, Cut Loss Price: $22.00

|

| |

|

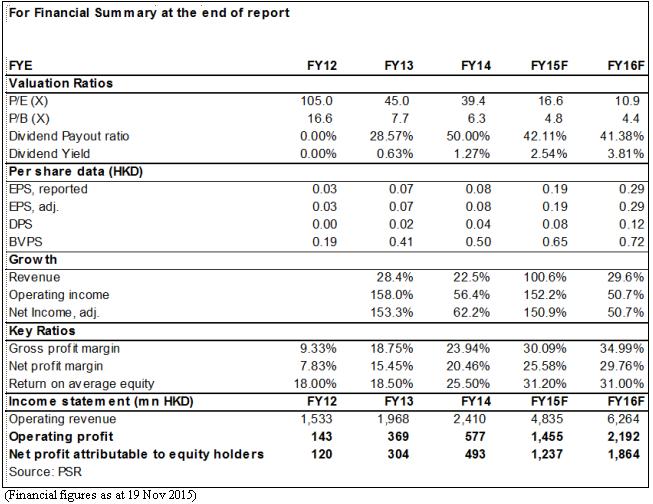

Xinyi Solar (968.HK) - Leader in the Solar Glass Industry

The company is the world's largest solar glass manufacturer. With reported revenue of RMB1.88 billion in 2014, it was the world and China's second largest solar glass producer, accounting for global and domestic market shares of 17.1% and 23.7% respectively. As the company significantly expanded its production capacity in 2014 to reach 3,800 tonnes, it has become the largest global and national producer, with market shares of 20.2% and 27.5% respectively. It is expected that the revenue of the company will be the highest among global players in 2015. Rapid Growth of the Solar Glass IndustryFollowing the rapid growth of the photovoltaic industry, the production volume of solar glass has also increased annually. In 2010, the production volume of China's solar glass was 99 million sq.m. and it has already increased to 275 million sq. m. by the end of 2014, representing a CAGR of 28.9%. In the next 5 years, with the expected installed capacity of solar plants maintaining at 18GW per year, the production volume of solar glass will also increase mildly, though the pace of increase may slow. Capacity Expansion being a Catalyst of Profit GrowthIn 2015H1, the reported revenue of the company surged by 106.5% yoy to HKD2.05 billion. Net profit attributable to shareholders jumped by 200% yoy to HKD601 million and EPS was HKD0.0943. The 1,800 tonnes of new capacity that commenced operation since 2014H1 contributed to the remarkable increase in profit and secured the company's leading position in the solar glass industry. The gross margin of the company's solar glass business improved from 33.7% in the same period of last year to 35.5%. Although the selling prices of solar glass fell in 2015H1, economies of scale from the increased capacity helped boost the gross margin. ValuationAs of 2015H1, the company has 280MW of solar plants in operation and targets to increase its aggregate installed capacity to 1GW by the end of 2015, which will be a new catalyst of profit growth. The company's new production line in Max`laysia will commence operation next year. We believe that as the solar glass industry is highly competitive, the company is unlikely to further increase its domestic production capacity. It will re-invest its profits from glass production to build more solar farms and eventually be a solar power operator. We recommend a ¡§BUY¡¨ rating, with a target price of HKD4.35, which is equivalent to a prospective 2016 P/E of 15x. (Closing price as at 19 Nov 2015) Financials

Click Here for PDF format...

| Recommendation on 23-11-2015 | | Recommendation | Buy | | Price on Recommendation Date | $ 3.150 | | Suggested purchase price | N/A | | Target Price | $ 4.350 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | China Galaxy Securities | 6881 | 18/11/2015 | Buy | 12.5 | 7.35 | | Haitong Securities | 6837 | 11/11/2015 | Buy | 23.9 | 15.02 | | | GWM | 2333 | 12/11/2015 | Accumulate | 10.73 | 9.74 | | Brilliance China | 1114 | 05/11/2015 | Neutral | 10.85 | 10.34 | | | COLI | 688 | 20/11/2015 | Reduce | 25 | 26.6 | | Longfor Properties | 960 | 16/11/2015 | Accumulate | 12.5 | 11.16 | | | | LESSO | 2128 | 23/09/2015 | Buy | 7.9 | 6.02 | | FORTUNE REIT | 778 | 14/10/2014 | Accumulate | 7.32 | 6.92 | | | HSBC | 5 | 09/08/2013 | Accumulate | 100.4 | 84.25 | | HSBC Holdings PLC | 0005 | 09/05/2013 | Accumulate | 95 | 87.7 | | | KPC Pharmaceuticals | 600422 | 03/11/2015 | BUY | 42.63 | 33.67 | | Yibai Pharmaceutical | 600594 | 29/09/2015 | Buy | 21.55 | 15.9 | | | Galaxy Entertainment | 27 | 29/10/2015 | Buy | 35 | 26.8 | | Galaxy Entertainment | 27 | 08/07/2015 | Buy | 42 | 33.55 | | | Xinyi Solar | 968 | 23/11/2015 | Buy | 4.35 | 0.000 | | Keda Clean Energy | 600499 | 17/11/2015 | Buy | 27 | 21.41 | | Food, Beverage and Retail | | | |

| | SAMSONITE | 1910 | 10/11/2015 | Accumulate | 28 | 24.05 | | China Tianyi Holdings | 756 | 16/10/2015 | Buy | 2 | 0.97 | | | AAC Technologies | 2018 | 19/11/2015 | Neutral | 54.64 | 55.05 | | China Unicom | 762 | 13/11/2015 | Buy | 12 | 9.74 | | | TSC GROUP | 206 | 28/07/2015 | Buy | 2.8 | 2.11 | | SPT Energy | 1251 | 24/02/2015 | Reduce | 1.5 | 1.74 | | | Goldpac Group | 3315 | 18/02/2015 | N/A | | 4.77 | | KINGDEE INT`L | 268 | 02/12/2014 | Accumulate | 2.75 | 2.45 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2015 Phillip Securities (HK) Ltd. All Rights Reserved.

|