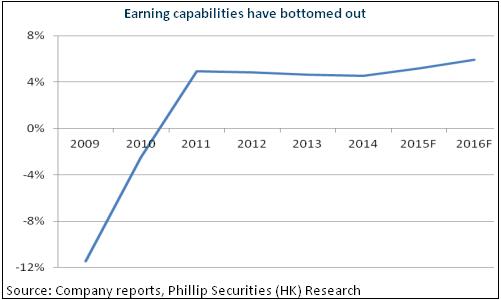

In 2015H1, Chinasoft's overall revenue recorded a growth of 23.3% yoy to RMB2.39 billion. Affected by the increased portion of hardware sales which profitability was lower, the Company's gross profit margin dropped by 1.6 ppts yoy to 28.4%. However, rate of sales and management fee decreased by 2ppts yoy to 18.8% because of economies of scale. Therefore, the Company's net profit surged 37.9% yoy to RMB0.14 billion, with net profit margin improved by 0.6 ppts yoy to 5.8%.

The Company has announced an issuance of new shares to acquire 40% equity of Chinasoft International Service owned by Huawei (the number of new shares would not exceed 5% of the post-issuance total share). Chinasoft International Service mainly provides services to Huawei. In our views, Huawei would become a strategic shareholder of the Company, but no longer an ordinary business partner, after such issuance of new shares. The strategic operation between Huawei and the Company is expected to be consolidated and enhanced. In the future, more of the outsourcing services of Huawei would be allocated to Chinasoft. Moreover, the cooperation field will develop into new services including cloud computing, big data, industry 4.0 etc.

Joint Force platform transforms human resources, from a management system to interest relations: IT operators, teams and enterprises gain income based on the jobs acquired. The Company then collects fixed commission in the due course. With the Company's business gradually transiting to the Joint Force platform, the overall cost of human resources would become stable. The business of the platform can enhance the gross profit margin, and boost up the profitability of the Company. In addition, the platform would also serve long tail markets of small-scaled IT projects, and accumulate data for systems, and then access the exchange volume, credit and cash flow etc of new enterprises and micro enterprises. Big data analysis could help lower the credit risk. The Company would plan to provide capital in the future, for provision of high-quality supply chain financial services to small and micro enterprise, nurturing new momentum for profit growth.

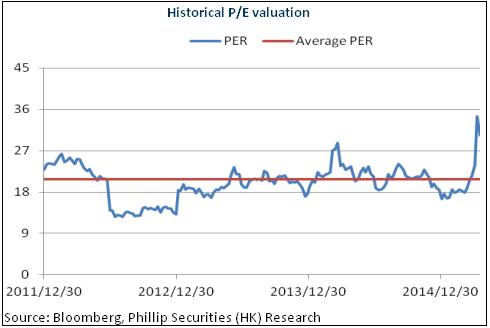

High stock margin of safety

In 2015H1, large-scale institutes continued to acquire Chinasoft's equity in large quantity at the price between HKD3.68 and 3.93, indicating the Company's stock price has higher margin of safety. In August, Chinasoft was successfully included as one of the constituent stocks of the Hang Seng Composite SmallCap Index, demonstrating the Company being recognized by the international capital market. We believe that the Company would continue to be benefitted from the informatization of China, localization of IT, expanded off-shore IT outsourcing market, and the robust growth of new emerging industries like cloud computing. Plus with the enhancement of efficiency of platform, as well as profitability, fast growth of the Company's business is expected. We grant the Company a valuation corresponding to 25x EPS in e2015, with a target price of HKD4.35, and a rating of ¡§Buy¡¨. (Closing price as at 6 Oct 2015)

Prosperous growth of business in H1

In 2015H1, Chinasoft's overall revenue recorded a growth of 23.3% yoy to RMB2.39 billion, in which the business of cloud computing and mobile internet indicated robust growth, boosting the income from emerging services up 47% yoy to RMB0.22 billion. Based on business segments of the Company, professional services business, outsourcing services business and emerging services business accounted for 40.3%, 48.6%, 9.2% of the Company's results respectively.

Affected by the increased portion of hardware sales which profitability was lower, the Company's gross profit margin dropped by 1.6 ppts yoy to 28.4%. However, rate of sales and management fee decreased by 2ppts yoy to 18.8% because of economies of scale. Therefore, the Company's net profit surged 37.9% yoy to RMB0.14 billion, with net profit margin improved by 0.6 ppts yoy to 5.8%.

Huawei would upgrade as strategic shareholder

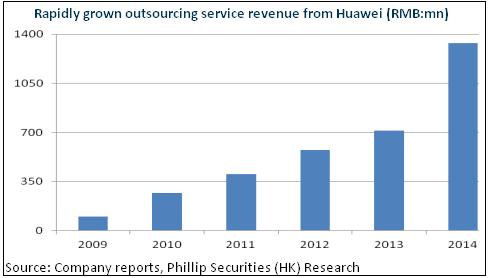

Chinasoft is the largest outsourcing services provider of Huawei, and Huawei is also the major client of Chinasoft's outsourcing services business. Since 2012, the CAGR of the outsourcing business from Huawei has reached 52.8%, accounted for 66% of total income of outsourcing business in 2014. In 2015H1, ChinaSoft's revenue from Huawei surged 32% yoy, still far higher than the growth rate of income of outsourcing business which is 20.8%. Currently, the Company has announced an issuance of new shares to acquire 40% equity of Chinasoft International Service owned by Huawei (the number of new shares would not exceed 5% of the post-issuance total share). Chinasoft International Service mainly provides services to Huawei. In our views, Huawei would become a strategic shareholder of the Company, but no longer an ordinary business partner, after such issuance of new shares. The strategic operation between Huawei and the Company is expected to be consolidated and enhanced. In the future, more of the outsourcing services of Huawei would be allocated to Chinasoft.

Huawei has already formulated a development goal, income in the coming three years is expected to be USD100 billion to USD120 billion. Income recorded in 2014 was merely about USD45 billion. In other words, an income growth of more than double is expected and this would bring momentum to the development of the related business of Chinasoft International. Previously, Huawei's business mainly focus on the Company's outsourcing aspect, but the recent cooperation between the Company and Huawei has been developed into new services including cloud computing, big data, industry 4.0 etc. It is worth to note that Huawei is now implementing a staff enhancement policy: the number of staff would keep unchanged with the expanded scale of operation in the future. Therefore, Huawei would release medium- and high-end services to outsourcing companies and Chinasoft could grasp more clients directly. Such client groups are in large quantity, allocated in domestic Chinese markets as well as overseas.

Speedy development of the Joint Force platform

The Company's Joint Force platform was successfully launched on 19 June and it demonstrated a trend of fast growth. As at the end of August 2015, the platform recorded the number of registered programmers as over 42,000 (which includes 12,000 staffs of the Company), and over 1800 registered enterprise-users. The yearly goal of the Company is making the number of enterprise business customers over 10,000 and the number of registered programmers over 100,000.

Currently, the goal of the platform concentrates on administrative cloud and industry internet, in order to gather IT service providers and operators, and boost up industrial efficiency. One point to highlight is that the platform would also serve long tail markets of small-scaled IT projects, and accumulate data for systems, and then access the exchange volume, credit and cash flow etc of new enterprises and micro enterprises. Big data analysis could help lower the credit risk. The Company would plan to provide capital in the future, for provision of high-quality supply chain financial services to small and micro enterprise, nurturing new momentum for profit growth.

Overall, Joint Force platform transforms human resources, from a management system to interest relations: IT operators, teams and enterprises gain income based on the jobs acquired. The Company then collects fixed commission in the due course. With the Company's business gradually transiting to the Joint Force platform, the overall cost of human resources would become stable. The business of the platform can enhance the gross profit margin, and boost up the profitability of the Company.

Catalyst

Better-than-expected development of outsourcing markets;

Better-than-expected development of the Joint Force platform.

Risks

Intensified market competition drags down profitability;

Labor cost increases too quickly;

Operation risk of Joint Force platform and cloud computing.

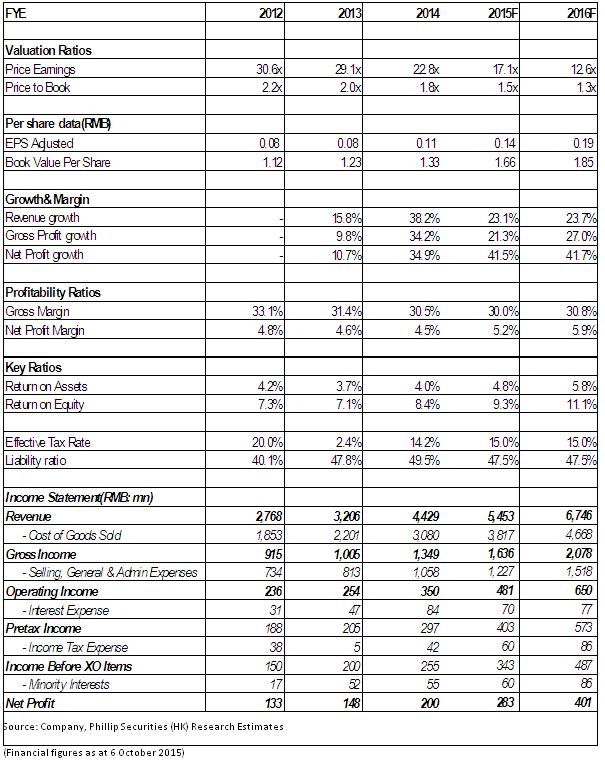

Financials

Click Here for PDF format...