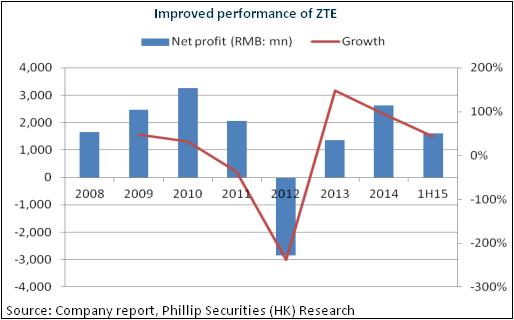

ZTE reported a 21.76% increase in revenue to RMB45.9 billion in 1H15. Net profit attributable to shareholders increased by 43.26% yoy to RMB1.616 billion. The result was in line with expectations. As for the breakdown by business segments, reported revenue from carriers` networks was up by 30% yoy to RMB28.5 billion, mainly driven by continued investments in 3G/4G networks from both local and overseas operators. Meanwhile, benefiting from sales of video and network terminal products, revenue from telecommunications software systems, services and other products was up by 41% yoy to RMB7.4 billion.

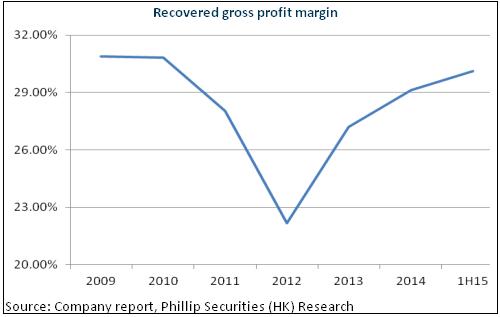

The gross margin increased by 0.6%-point to 30.1%, mainly driven by improved domestic and overseas profit margins from carriers` network businesses, as the merger of Nokia and Alcatel eased the competition among telecommunications equipment suppliers. Moreover, revenue mix was improved following a higher revenue contribution from carriers` networks.

We remain positive on the profit outlook of the company. Firstly, domestic carriers will speed up construction of 4G networks. Besides, in overseas markets, demand for the 4G network construction is shifting from developed countries to developing markets. Being the leading player in the telecommunications industry with overseas recognition of its technological edge, ZTE is expected to increase its market share and benefit from a booming global demand for network construction. Moreover, the company actively develops the terminal business and expands its services to government and corporate customers.

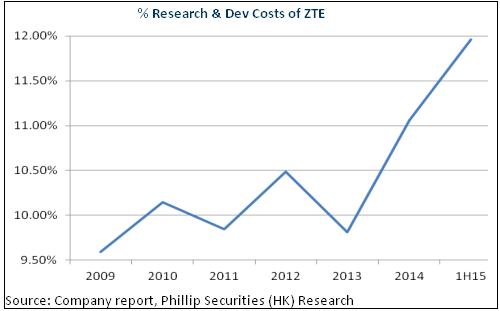

The R&D expenses of the company broke its record again in 2015H1. After spending RMB25.7 billion in R&D in Q1, R&D expenses reached RMB2.92 billion in Q2 and accounted for 12% of total revenue, exceeding its previous record of 10%. We believe consistently high investment in R&D will help the company build up its long-term competitive advantages in telecommunications and new technological arenas.

Speeding Up in Research Development in New Arena

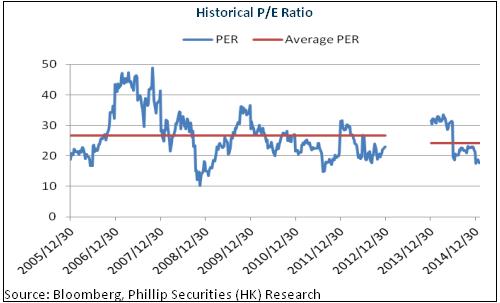

The traditional communication business of the company is still booming. The development of its overseas markets may be better than expected due to favorable policies. We expect that its profit will continue to grow steadily. It is worth noting that the company is expanding its investment in research and development and actively developing into new arenas such as wireless charge, Smart City, big data platforms, etc. Its future development will no longer be confined to being a pure equipment supplier. We recommend a ¡§BUY¡¨ rating with target price of HKD21.72, which is based on a P/E ratio of 20x to its 2015 EPS. (Closing price at 1 Sep 2015)

Rapid Profit Growth in H1

Based on the interim report, ZTE reported a 21.76% increase in revenue to RMB45.9 billion. Net profit attributable to shareholders increased by 43.26% yoy to RMB1.616 billion. The result was in line with expectations.

As for the breakdown by business segments, reported revenue from carriers` networks was up by 30% yoy to RMB28.5 billion, mainly driven by continued investments in 3G/4G networks from both local and overseas operators, investments in wireline switch & access system and optical communication systems. At the same time, benefiting from sales of video and network terminal products, revenue from telecommunications software systems, services and other products was up by 41% yoy to RMB7.4 billion. However, undermined by a decrease in domestic handset sales compared with the same period of last year, the reported revenue from the company's handset terminals was just RMB10 billion, representing a 4% yoy decline. As for the revenue breakdown by regions, the company has been rapidly expanding its business in Africa, which recorded a 45% yoy increase in revenue. Moreover, revenue growth in China and Asia (ex-China) remained strong at 28% yoy and 23% yoy respectively.

As for profitability, gross margin of the company increased by 0.6%-point to 30.1%, mainly driven by improved domestic and overseas profit margins from carriers` network businesses, as the merger of Nokia and Alcatel eased the competition among telecommunications equipment suppliers. Moreover, revenue mix was improved following a higher revenue contribution from carriers` networks, which also led to a faster growth in the company's profit than revenue.

H2 Growth Momentum Continued to be Strong

We remain positive on the profit outlook of the company. Firstly, domestic carriers will speed up construction of 4G networks. Investments in transmission and indoor network coverage are also expected to increase. In domestic markets, China Telecom and China Unicom already announced that they will speed up construction of 4G networks in H2. The former plans to complete its strategy to build 460,000 units of 4G base stations, while the latter expects to complete its strategy to build 1.2 million units of base stations, of which 400,000 to 500,000 units are 4G base stations. This will support the booming trend of the domestic telecommunications equipment market.

Besides, in overseas markets, demand for the 4G network construction is shifting from developed countries to developing markets. As China rolls out the ¡§One Belt, One Road¡¨ Strategy, the telecommunications industry, being one of China's pioneering industries, will speed up its overseas expansion. Being the leading player in the telecommunications industry with overseas recognition of its technological edge, ZTE is expected to increase its market share and benefit from a booming global demand for network construction.

Moreover, the company actively develops the terminal business and expands its services to government and corporate customers. In the handset terminals business, the company focuses its branding and sales strategy on the high-end segment, which will expect to improve its profitability. By the end of July, the company released its flagship product AXON, which is expected to improve its sales. At the same time, growth in overseas sales of 4G terminal products is expected to continue. As for the government and corporate business, the company will strengthen its ¡§M-ICT¡¨ development strategy by speeding up the development and construction of railway transport and Smart City. There was already a pick-up in the growth trend of orders in H1.

Sustained Increase in R&D Investment to Build Up Its Long-Term Competitive Advantages

The R&D capability of ZTE has been ahead of its peers. As of 2014, the company ranked the third globally in the applications for PCT patents for 5 years in a row. It filed over 60,000 applications for international patents and was granted 17,000 patents. The R&D expenses of the company broke its record again in 2015H1. After spending RMB25.7 billion in R&D in Q1, R&D expenses reached RMB2.92 billion in Q2 and accounted for 12% of total revenue, exceeding its previous record of 10%.

At present, the company gradually rolls out R&D in LTE, SDN, pre5G, Internet of Things. It also develops into new arenas such as Smart City, new energy and wireless charge. This will broaden the development prospects of the company. We believe consistently high investment in R&D will help the company build up its long-term competitive advantages in telecommunications and new technological arenas.

Catalysts

Continued booking of large orders from overseas;

Progress of FDD-LTE tenders;

Gradual roll-out of projects in new arenas.

Risks

Volatility in exchange rates affecting profitability;

Higher operating costs from new business development;

Handset sales volume and average prices are below expectations.

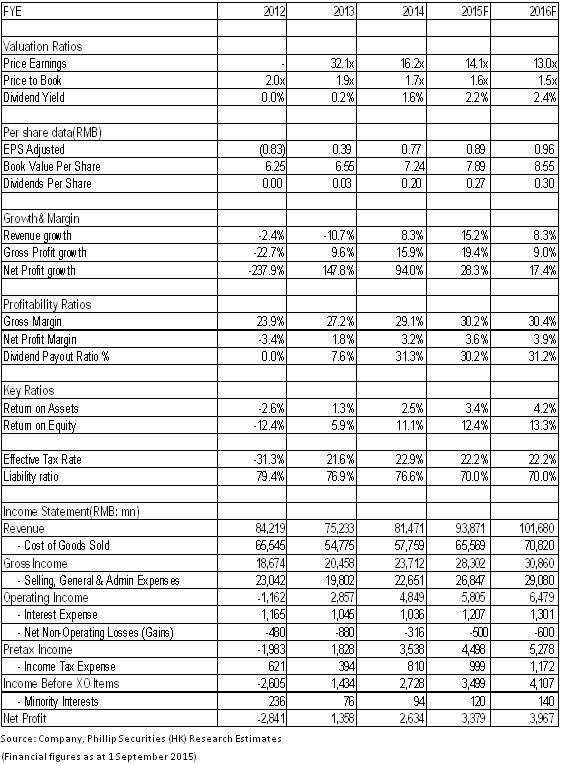

Financials

Click Here for PDF format...