Summary

-Based on the 2015H1 earnings result reported by China Merchants Bank (CMB / Group), CMB maintained a stable trend of profit growth. As of June 2015, net profit attributable to shareholders increased by 8.3% to RMB32.976 billion;

-The asset size of CMB maintained its high growth trend. As of 2015H1, the total assets of the Group greatly grew by 10.34% from 2014 to RMB5.22 trillion. During the period, shareholders` net assets reached RMB332.075 billion, which were equivalent to a book value (NAV) per share of RMB13.17, representing a 16.14% increase from 2014;

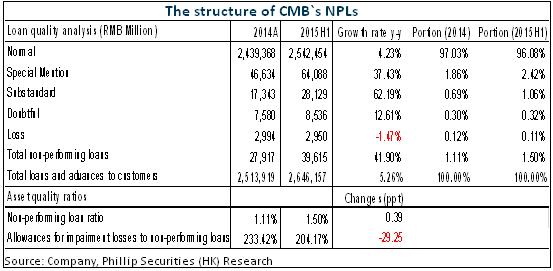

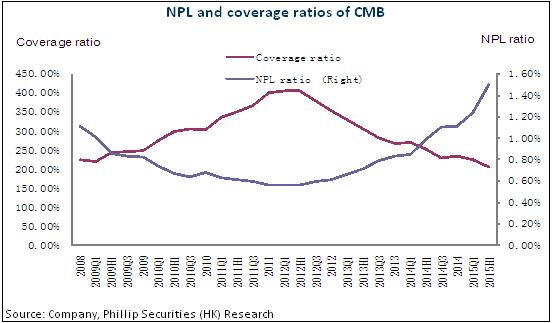

-The asset quality of the bank remains our main concern. As of June 2015, NPL ratio of the Group jumped by 0.39ppts from 2014 to 1.5%, which was higher than our previous expectation. However, NPL allowance coverage ratio dropped by 29.25ppts to 204.17%;

-The capital adequacy ratio of CMB has been persistently lower than its peers. Although the bank has delivered stable growth, it still faces relatively higher fund-raising pressure. As of June, the core Tier 1 capital adequacy ratio and capital adequacy ratio of CMB rose by 0.07ppts and 0.03ppts from 2014 to 9.67% and 11.77% respectively. We expect that CMB will have higher funding needs in future;

-Overall speaking, CMB delivered stable growth, but its asset quality and capital adequacy will continue to be the major operating risks in future. We are still positive on the outlook of CMB's operating performance. Factoring its stable dividend payout record into the three-stage dividend discounting model, and considering the risks associated with huge volatility of the stock market, our target price is downgraded to HKD25.00. It is higher than the latest closing price by 36% and equivalent to a prospective 2016 P/E of 8.7x and P/B of 1.3x. We maintain a ¡§BUY¡¨ rating. (Closing price as at 27 Aug 2015)

Stable Profit Growth and Continuous Deterioration in Asset Quality

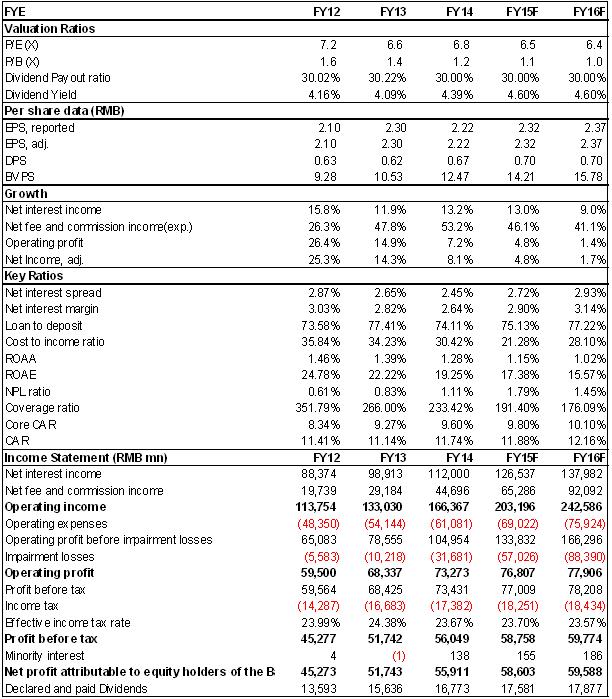

As of June 2015, net profit attributable to shareholders grew by 8.3% yoy to RMB32.976 billion, which was equivalent to EPS of RMB1.31.

Regarding its operating income, CMB's net interest income grew by 17.7% yoy to RMB6.104billion while net fee and commission income significantly grew by 45.4% yoy to RMB31.097 billion. The higher than expected growth was mainly driven by the bull market in H1 that led to a surge in fee-based business. However, net profit of CMB was lower than expected. This was mainly due to significant increases in operating expenses, especially from the sharp increase in impairment losses of loans, which surged by 78.7% yoy to RMB291.71 billion. Considering that the asset quality of CMB will continue to deteriorate, we expect its impairment losses on loan will continue to grow at a high level in the coming two years and thus significantly affecting the profitability of CMB. We expect that net profit growth of CMB will maintain at low-teens in the coming two years.

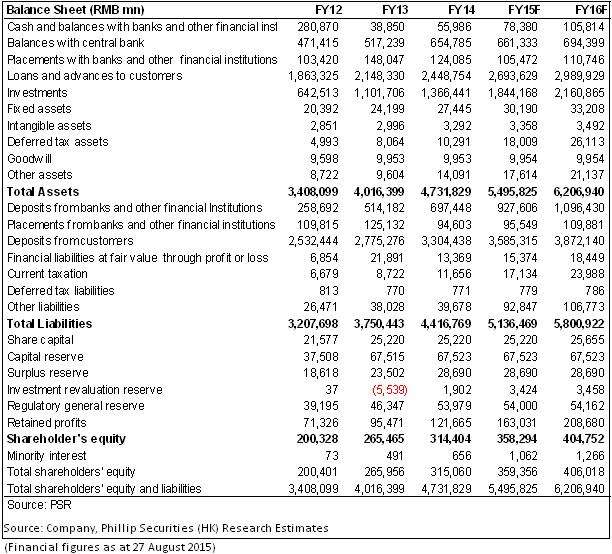

On the other hand, looking into the assets, CMB maintained a relatively high growth trend in its asset size. As of Jun 2015, the total assets of CMB greatly grew by 10.34% from 2014 to RMB5.22 trillion. During the period, shareholders` net assets reached RMB332.075 billion, which were equivalent to a book value (NAV) per share of RMB13.17, representing 16.14% increase from 2014.

The asset quality of the bank remains our main concern. As of June 2015, NPL ratio of the Group jumped by 0.39ppts from 2014 to 1.5%, of which substandard and doubtful loans increased by 62.2% and 12.6% to RMB28.129 and 8.536 billion respectively. However, NPL allowance coverage ratio dropped by 29.25ppts to 204.17%. We expect that both NPL volume and ratio of CMB will continue to rise in the upcoming two quarters in 2015H2.

At the same time, CMB's capital adequacy ratio has been persistently low. Although it delivered stable growth, it is still facing relatively higher funding-raising pressure. As of June, the core Tier 1 capital adequacy ratio and capital adequacy ratio of CMB rose by 0.07ppts and 0.03ppts from 2014 to 9.67% and 11.77% respectively. We expect that CMB will have higher funding needs in future.

Risk

Surge in NPL volume, worse than expected deterioration in asset quality;

Slower than expected growth in Interest and non-interest income;

Sharp share price correction amid volatile market in the near term

FINANCIALS

Click Here for PDF format...