Total Auto Sales Mildly Declined by 1.7% yoy, SUV Sales Rose by 12.8% yoy

Great Wall Motor's (GWM) July auto sales dropped by 1.7% yoy. Sales of sedans and pick-up trucks plunged by 52% and 37% yoy respectively. The sales of major product SUVs increased by 12.8% yoy. The growth was lower than industry's average (+34%) and that of GMW's previous growth rates.

Preliminary Financial Data: Net Profit increased by 24%

The company released its preliminary financial data for 2015H1 recently: total revenue rose by 30.21% yoy to RMB37.145 billion; net profit grew by 23.96% yoy to RMB4.901 billion; EPS was RMB1.61. The increase in profit was mainly due to a close to 50% increase in the sales volume of SUVs. Benefiting from the launch of more new models since the second half of last year, the quarterly sales volumes of SUV models of the company rose by 54% and 43% yoy respectively.

Multi Factors Curbing the Growth Momentum

Starting from June, the share price of GWM has underperformed the market. Apart from a weaker auto sales growth in China that has intensified the competition in the SUV sub-segment, we believe that it is also mainly caused by the worse than expected sales of GWM's major sales model, H6, even after the launch of H6 CoupeC. Moreover, the sales of H8 and H9, which are models strategically targeted for the high-end market, were below its initial sales target. As the domestic auto market has yet to see a turnaround, we expect the SUV sales growth of GWM will continue to slow down due to its higher volume base from 3Q15. In mid-June, GWM announced to decrease the official selling prices of most of its vehicle models. If the price cuts fail to stimulate sales growth afterwards, the pricing pressure will erode profitability of the company.

Private Placement of RMB16.8 Billion for Business Transformation

The company announced by circular to raise RMB16.8 billion from the private A-Share placement on 11 July. The issuance price would not be lower than RMB43.41 per share. The capital raised will be used for new energy vehicles & related core auto components and smart vehicles. Besides, the major shareholders also announced by circular that they will seek opportunities to increase stakes in the company. We believe that developing new energy and smart vehicles will the major trend of the auto industry. This huge fund-raising exercise demonstrated the determination of the management team to transform GMW's business model. It will be help the company fill in the gap of technological innovation in the auto industry and build up a solid foundation for its long-term development. However, its earnings in the near term will inevitably be affected by the earnings dilution and the uncertainties of the progress of new projects.

Investment Thesis

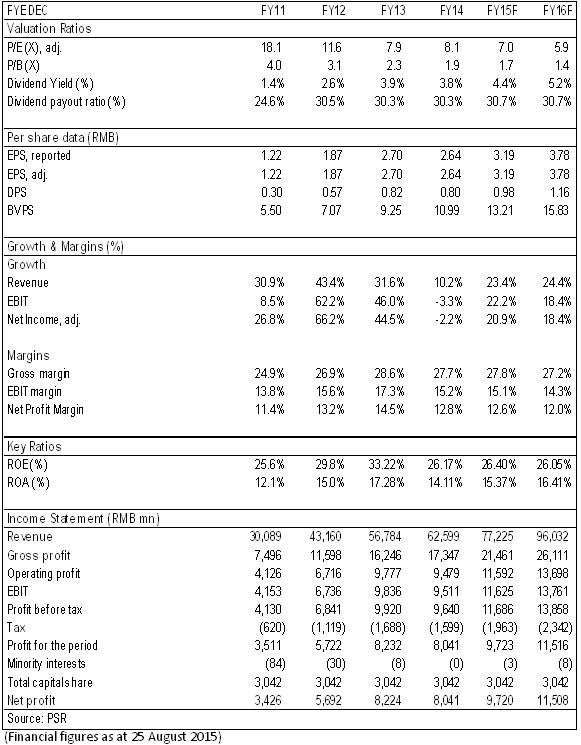

As analyzed above, we revised EPS expectation of the Company to RMB 3.19, 3.78 of 2015/2016. And we accordingly revised the target price to 27, respectively 7/5.9x P/E for 2015/2016. We upgrade it to "Buy" rating. (Closing price as at 25 August 2015)

Total Auto Sales Mildly Declined by 1.7% yoy, SUV Sales Rose by 12.8% yoy

Based on the sales data of Great Wall Motor (GWM) in July, monthly auto sales dropped by 1.7% yoy. Sales of sedans and pick-up trucks plunged by 52% and 37% yoy respectively. But as the proportion of these two types of vehicles further shrank to below 16% of total auto sales, the impact on overall auto sales was further lessened. There has not been a turnaround in exports yet, which dropped by 47% yoy to 2,344 units.

The sales of major product SUVs increased by 12.8% yoy. The growth was lower than industry's average (+34%) and that of GMW's previous growth rates. For the breakdown by models, sales of models H2, H1, H9 and H8 were 10,024, 2,544, 655 and 1,059 units. But the sales performance of older models H6, H5 and M series was disappointing, which dropped by 13%, 49% and 77% to 23,088, 1,471 and 1,070 units respectively.

For the 7 months in this year, GWM totally sold 463,000 units of vehicles, representing an increase of 17% yoy. The cumulative sales of SUVs rose by 43.8% yoy to 375,000 units. Sales of sedans and pick-up trucks fell by 51% and 21% yoy to 30,000 units and 58,000 units.

Preliminary Financial Data: Net Profit increased by 24%

The company released its preliminary financial data for the interim period of 2015 recently: From January to June this year, total operating revenue rose by 30.21% yoy to RMB37.145 billion; its net profit grew by 23.96% yoy to RMB4.901 billion; EPS was RMB1.61. The increase in profit was mainly due to a close to 50% increase in the sales volume of SUVs. By the end of June, the total assets of the company reached RMB61.553 billion.

On a quarterly basis, net profits of Q1 and Q2 were RMB2.536 billion and RMB2.365 billion respectively, representing an increase of 26% yoy and 21% yoy. Benefiting from the launch of more SUV models since the second half of last year, the quarterly sales volumes of SUV models of the company rose by 54% and 43% yoy respectively.

Multi Factors Curbing the Growth Momentum

Starting from June, the share price of GWM (-62%) has underperformed the market (-23%). Apart from a weaker auto sales growth in China that has intensified the competition in the SUV sub-segment, we believe that it is also mainly caused by the worse than expected sales of GWM's major sales model, H6, even after the launch of H6 CoupeC. Moreover, the sales of H8 and H9, which are models strategically targeted for the high-end market, were below its initial sales target.

Although H6 continued to rank the first in the domestic SUV market and widened the gap with the second top-selling model in July, market competition of SUVs intensified amid a slow down domestic auto market. With the influx of competitive products from local-foreign JV brands and other independent brands, the competition landscape of GWM became more rugged. In addition, as the company has been the leading SUV brand for several years, its market share in the SUV sub-segment began to slip due to the high-base effect. The quarterly growth of H6 also slowed down from 29% to 12%.

As the domestic auto market has yet to see a turnaround, we expect the SUV sales growth of GWM will continue to slow down due to its higher volume base from 3Q15. In mid-June, GWM announced to decrease the official selling prices of most of its vehicle models. If the price cuts fail to stimulate sales growth afterwards, the pricing pressure will erode profitability of the company. However, based on the development path of its foreign peers, it is difficult and tortuous to nurture a high-end brand. And this strategy cannot be realized within an investment horizon of 3-5 years and patience should be needed.

Private Placement of RMB16.8 Billion for Business Transformation

The company announced by circular to raise RMB16.8 billion from the private A-Share placement on 11 July. The issuance price would not be lower than RMB43.41 per share. The capital raised will be used for new energy vehicles & related core auto components and smart vehicles. Of the net proceeds raised, RMB5.08 billion will be used for the research and development of new energy vehicles, RMB4.142 billion for smart transmission system for new energy vehicle with annual production capacity of 500,000 units, RMB1.762 billion for new energy vehicle motor and management device with annual production capacity of 500,000 sets, RMB1.044 billion for driving battery system for new energy vehicle with annual production capacity of 1 million packs and RMB5.02 billion for research and development of smart vehicles. Besides, the major shareholders also announced by circular that they will seek opportunities to increase stakes in the company.

We believe that developing new energy and smart vehicles will the major trend of the auto industry. This huge fund-raising exercise demonstrated the determination of the management team to transform GMW's business model. It will be help the company fill in the gap of technological innovation in the auto industry and build up a solid foundation for its long-term development. However, its earnings in the near term will inevitably be affected by the earnings dilution and the uncertainties of the progress of new projects.

Investment Thesis

As analyzed above, we revised EPS expectation of the Company to RMB 3.19, 3.78 of 2015/2016. And we accordingly revised the target price to 27, respectively 7/5.9x P/E for 2015/2016. We upgrade it to "Buy" rating.

Financials

Click Here for PDF format...