Summary

-As at the end of 2015Q1, the profit attributable to shareholders of China Minsheng Bank (¡§Minsheng¡¨ or ¡§the Group¡¨ in the following text) recorded RMB13.377 billion, up 5.53% yoy, which was slightly lower than our previous expectation, representing EPS amounted to RMB0.45. The main reason for keeping steady growth of profit in the period under review was the robust surge of income from intermediate business, from which the net commission fee indicated a significant yoy growth of 38%, to RMB12.026 billion. Net interest income in the same period merely recorded a yoy growth of approximately 9.2%;

-Total asset of the Group slightly increased by 0.04% to RMB4.02 trillion as compared to the year-end of 2014. All types of Minsheng's assets, particularly inter-bank lending business, showed significant drop, leading to a shrink of asset scale. Net asset of the Group amounted to RMB254.079 billion, representing net asset per share as RMB7.42, up 5.55% as compared to the year-end of 2014;

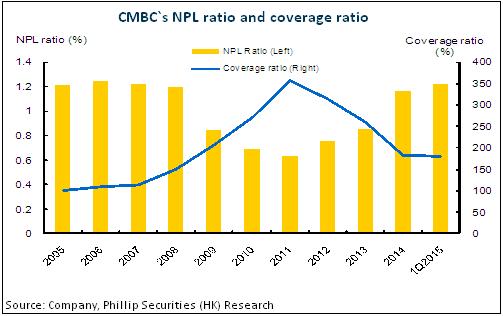

-Due to the environment of real economy remains in the doldrums, the business environment of domestic SMEs is getting worse than before, causing the deterioration of the quality of bank loans. As at the end of 2015Q1, the Group's non-performing loan (NPL) ratio recorded 1.22%, up 0.05ppts as compared to the year-end of 2014. Although the detailed composition of NLP of Q1 was not released, based on the information recorded in the year-end of 2014, both subprime loan and loss loan in the Group's NPL showed significant increase: from RMB9.221 billion and 1.081 billion recorded in the year-end of 2013 increased to RMB16.591 billion and RMB1.276 billion respectively. The weight of subprime loan and doubtful loan on the total NPL increased from 0.58% and 0.07%, to 0.92% and 0.07% respectively. Due to the consistent rise on the Group's NPL recorded in 2015Q1, we expect the amount of outstanding NLP and the NLP ratio would keep an uptrend, causing higher risk on worsening asset quality;

Overall, Minsheng's profit growth is being slowed down, but the business of loans to small and micro enterprises etc. enjoys stable development. While the standard of capital is relatively good, quality of asset is facing the risk of deterioration. Having considered the current market volatility, the bank's valuation is low, and we maintain the rating of Minsheng as ¡§Accumulate¡¨, granting a 12-month target price of HK$10.50, which is 19% higher than the latest closing price, and equivalent to 5.8x of the EPS and 1.0x of the BVPS of 2016 respectively. (Closing price as at 29 July 2015)

Worsening of asset quality is the greatest challenge to Minsheng currently

As at the end of March 2015, the profit attributable to shareholders of Minsheng recorded RMB13.377 billion, up 5.53% yoy, representing earning per share amounted to RMB0.39. Among this, the net income from handling fee and commission indicated a significant yoy growth of 38%, to RMB12.026 billion. Net interest income in the same period merely recorded a yoy growth of approximately 9.2%. We expect Minsheng's net profit growth in 2015H1 would consistently slow down, probably lower than 5%.

In terms of asset, the total asset of the Group slightly increased 0.04% to RMB4.02 trillion as compared to the year-end of 2014. All types of Minsheng's assets, particularly inter-bank lending business, showed significant drop, leading to a shrink of asset scale. Net asset of the Group was RMB254.079 billion, representing net asset per share as RMB7.42, up 5.55% as compared to the year-end of 2014.

Loans to small and micro enterprises are a special-featured business of Minsheng. As at the end of 2015Q1, the Group's outstanding loans to small and micro enterprises amounted to RMB407.828 billion, increased RMB5.092 billion as compared to the year-end of 2014, with the number of small and micro clients reaching 3.0255 million (increased 113,600). We expect the Group's business of loans to small and micro enterprises would keep stable growth in the future, but the rate of growth would be slowed down.

Nevertheless, due to the environment of real economy remains in the doldrums, the business environment of domestic SMEs is getting worse than before, particularly after the recent slump of the Chinese share markets, causing a big challenge to the Group's quality of asset. Beside the government capital entering the stock markets through bank credits, a large portion of capital from civic wealth-management products, and enterprises and personal loans also entered the share markets. The uncertainty of these capitals is high, which greatly raised banks` business risk in the future. As at the end of 2015Q1, the Group's NPL ratio recorded 1.22%, and the coverage ratio decreased to 180.58%. We expect the NPL ratio would increase to around 1.3% in 2015H1.

Overall, the business of Minsheng would be maintained at the comparatively stable level. We will review the Group's asset quality after the announcement of interim results.

Risk

Significant increase of the amount of NPL leading to worse-than-expected deterioration of asset quality;

Consistent slowdown of income growth of interest and intermediate businesses;

Big drop of share price due to market volatility in the short term.

Click Here for PDF format...