Comba Telecom recently announced their positive profit alert, expecting a mid-year net profit recorded in 1H15 increases no less than 40% as compared to the same period in last year, which is mainly due to the advantage that China is entering an initial construction cycle of 4G network, more effort on enhancing wireless network construction is needed. In 2015, not only China Mobile has changed its goal of constructing 4G base stations to one million and FDD license is also released throughout the whole country. Investment on 4G by China Telecom and China Unicom is also experiencing speedy expansion. It is anticipated that yearly 4G clients will be increased over 300 million and this will support the Company's wireless enhancement business to keep booming in medium term.

The wireless enhancement segment will also optimize the product mix of the Company and push up profitability. Moreover, with the advantages induced by economies of scale, in addition to effective cost control measures, the opex ratio of the Company declined nearly 5 percentage points as compared to the peak recorded in 2012. This also strongly pushed up the profitability of the Company. Looking forward, the Company will continue to be benefitted from economies of scale, and the drop in interest rate also helps saving financial costs. Rules and regulations for operators will assist to control expenses including marketing expenses. The opex ratio of the Company will probably keep declining.

In June, Comba entered an agreement with Guangzhou Zainar Info Tech Limited and Mapout Info Tech (HK) Limited, under which a joint-venture located in Beijing would be established. This joint-venture mainly works on indoor location-based service system throughout the whole country (including indoor mobile internet positioning system and indoor location-based big-data and map system). Comba possesses 20% of the equity of this joint-venture. Currently, operators in the market focus on 4G indoor coverage and mobile internet. Comba's Smallcell product is in line with the strategies of the operators. It is expected to help the joint-venture grow toward to leading provider of solutions concerning indoor location-based service system and brought new growth of profit for the Company.

Safe valuation with high margins

Benefitted from the emerging peak of 4G infrastructure investment, Comba Telecom started to earn profit, getting away from previous loss. It even demonstrated more speedy growth in 2015. It is worth to note that the Company occupies the leading position in the domestic Chinese market of wireless enhancement. Telecom operators accelerated on the construction of 4G network and boosted up the demand in this aspect, probably leading to rise in both its revenue and profit.

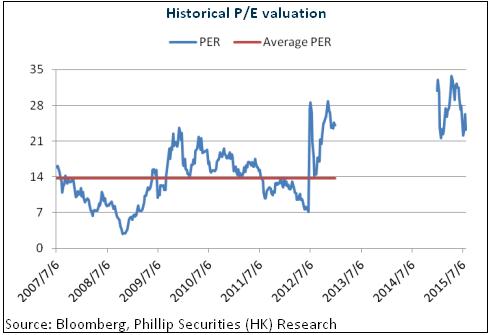

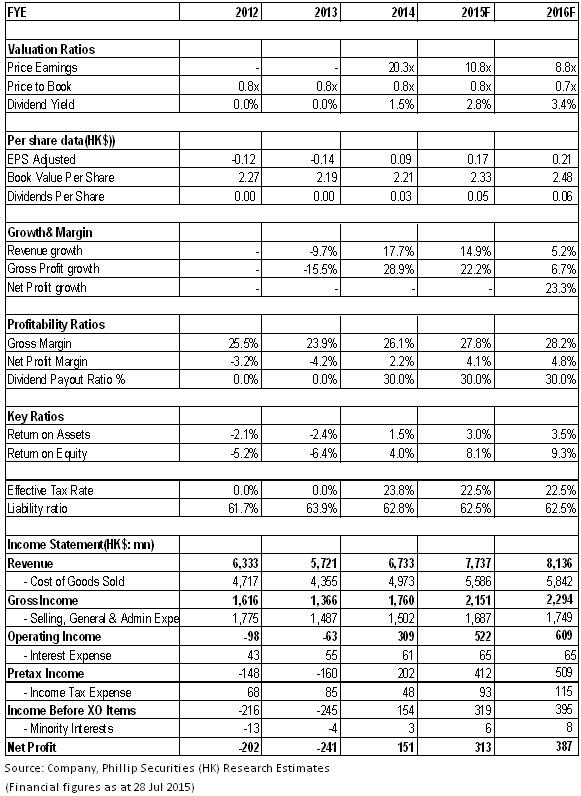

As the Company has regained growth, we take reference to P/E ratio. In the era of 3G, the Company was traded between 15x to 20x of P/E. However, after the recent slump of the stock market, the valuation of the Company is only about 10x of P/E, which is apparently being undervalued. We grant a valuation of 15x of EPS in 2015 and set the target price as HK$2.54, with the rating upgraded to ¡§Buy¡¨. (Closing price as at 28 July 2015)

Wireless enhancement business brought prosperous performance in 1H15

Comba Telecom recently announced their positive profit alert, expecting a mid-year net profit recorded in 1H15 increases no less than 40% as compared to the same period in last year, which is mainly due to the advantage that China is entering an initial construction cycle of 4G network, more effort on enhancing wireless network construction is needed. Since the award of TD LTE license in the year-end of 2013, the development of 4G has been far faster than 3G. New 4G clients recorded approximately 100 million in 2014. The construction target of the 4G base stations of China Mobile was also raised to 700,000 from the initial plan of 500,000. As the frequency of 4G is higher than 3G, worsening 4G radio wave's diffraction capability, and thus greater demands for its depth coverage and network optimization are required compared to 3G. In 2015, the 4G network which initially arranged by China Mobile would advance into that stage.

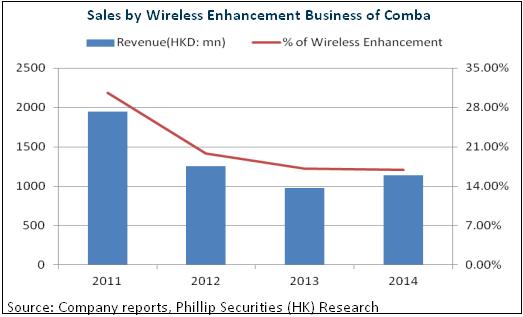

Previously, in the mid and later stage of 3G network construction, the Company's wireless enhancement business weighted more than 30%. However, after the peak of 3G network construction, demand dropped continually. It weighted only 17% in 2014. With the current development of 4G network, that business regained momentum and moved toward another boom, with the hope that its contribution to revenue would rebound to previous peak level. It is worth to mention that not only China Mobile has changed its goal of constructing 4G base stations to one million in 2015, and FDD license is also released throughout the whole country. Investment on 4G by China Telecom and China Unicom is also experiencing speedy expansion. It is anticipated that yearly 4G clients will be increased over 300 million and this will support the Company's wireless enhancement business to keep booming in medium term.

Profitability keeps improving

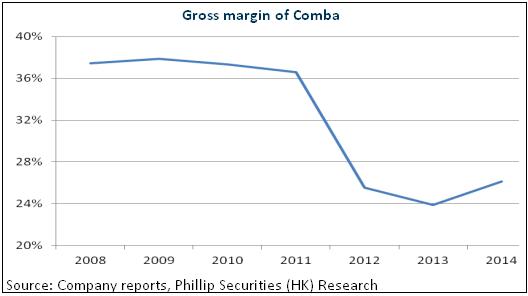

The wireless enhancement segment will also optimize the product mix of the Company and push up profitability. The mid and later stage of 3G network construction is key stage for contribution by the segment of wireless enhancement: profitability of the Company is strong, with gross profit margin recorded as high as around 37%. Subsequently, with the decline in the weighting of wireless enhancement, the gross profit margin significantly shrunk by around 10 percentage points and fell to 26% in 2014. We anticipate that, with the growth of business in wireless enhancement in the future, the profitability of the Company would keep improving.

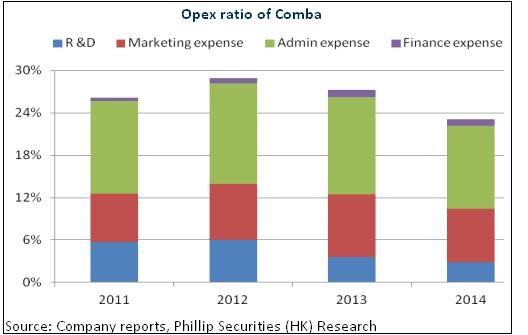

It is worth to note that, with the advantages induced by economies of scale, in addition to effective cost control measures, the opex ratio of the Company declined over 3 percentage points in recent years, and it even declined nearly 5 percentage points as compared to the peak recorded in 2012. This also strongly pushed up the profitability of the Company. Looking forward, the Company will continue to be benefitted from economies of scale, and the drop in interest rate also helps saving financial costs. Rules and regulations for operators will assist to control expenses including marketing expenses. The opex ratio of the Company will probably keep declining.

Layout location-based services brought new growth of profit

In June, Comba entered an agreement with Guangzhou Zainar Info Tech Limited and Mapout Info Tech (HK) Limited, under which a joint-venture located in Beijing would be established. This joint-venture mainly works on indoor location-based service system throughout the whole country (including indoor mobile internet positioning system and indoor location-based big-data and map system). Comba possesses 20% of the equity of this joint-venture.

Currently, operators in the market focus on 4G indoor coverage and mobile internet. Comba's Smallcell product is in line with the strategies of the operators. It is expected to help the joint-venture grow toward to leading provider of solutions concerning indoor location-based service system and brought new growth of profit for the Company.

Catalyst

4G construction progress is beyond expectation;

Better-than-expected development of overseas market.

Risk

More fierce competition leads to market loss.

Financials

Click Here for PDF format...