Summary

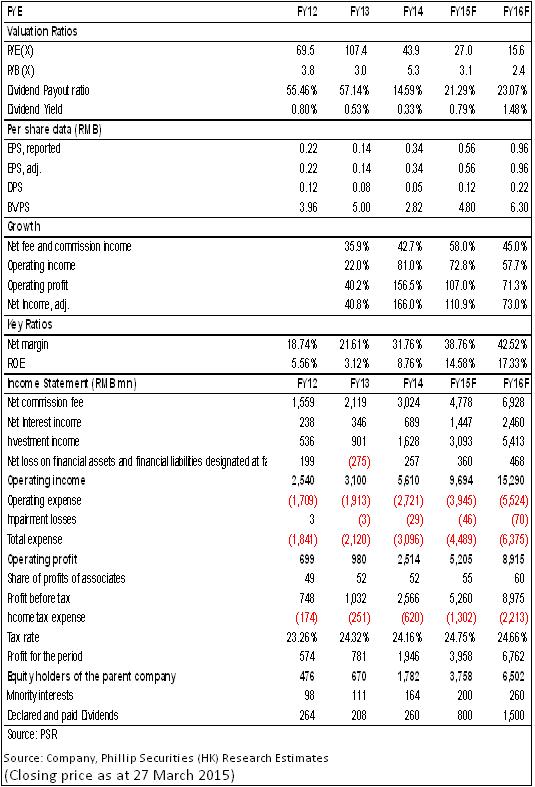

-Last week Industrial Securities (IS or the Group) had the investor presentation, and according to annual results, IS's profit increased sharply benefited from the rapid development of the market environment, better than our previous expectation. By the end of 2014, IS's net profit grew 166% approximately y-y to RMB1.78 billion, equivalent to the EPS of RMB0.34, and especially, incomes of proprietary trading and brokerage increased significantly;

-In addition, the management stated that IS's main advantages relied on investment and research. By the end of 2014, the Group's investment gains increased by 81% y-y to RMB1.628 billion. As one of major three key strategies, IS's research ended up at the sixth best domestic research team in 2014 from the seventh in 2013;

-Meanwhile, IS's asset also increased sharply, total assets grew around 102% y-y to RMB73.488 billion, and net assets increased by 13% to RMB14.683 billion, with the parent company's net capital of RMB13.571 billion. Due to the rapid growth of businesses currently, IS faces the large demand of the capital, and therefore the Group announced the rights issue of RMB10-15 billion in A Shares, and the capital pressure would go down obviously after the rights issue;

-Recently, CSRC stated domestic banks would have the license of brokerage in future, and the market believe it would increase the competitive pressure to brokerage firms, bur the management said the network advantage of banks would be diminished under the current development trend of internet finance, the key is the professionalization of the service and quality;

-In our view, even the banks get the brokerage license in the short term, the impact would be small on the brokerage firms, meanwhile, considering the same major shareholder of both IB and IS, Financial Bureau of Fujian Province, it would be very helpful for the business development due to the possibility of the business integration. Moreover, considering the positive development of the market in 2015, we have the confidence in IS's performance in future, and estimate its 12-m target price to HK$25.00, around 66% higher than the current price, equivalent to 26.0xP/E and 4.0xP/B in 2016 respectively, recommend Buy rating. (Closing price as at 27 March 2015)

Strong profit growth in 2014 with the core competitiveness of investment and research

IS's profit increased sharply benefited from the rapid development of the market environment, better than our previous expectation. By the end of 2014, IS's net profit grew 166% approximately y-y to RMB1.78 billion, equivalent to the EPS of RMB0.34, and especially, incomes of proprietary trading and brokerage increased significantly.

The incomes of proprietary trading increased sharply by 222% approximately y-y to RMB1.34 billion. Operating incomes of securities and future businesses grew 52.66% y-y to RMB2.4 billion. In addition, the margin trading increased rapidly, amounted to RMB13.81 billion in 2014, up 228% significantly, with the market share of 1.35% from 1.22% in 2013, and interest incomes increased by 179% to RMB570 million. The management estimated IS's margin trading would continue to increase sharply in 2015, currently, the amount is larger than that of the whole year of 2013, with the amount of RMB19 billion. Therefore, we believe IS's margin trading is going to increase significantly this year.

Investment banking business increased rapidly, especially for the underwriting of equity and bond, the incomes increased by 51% y-y to RMB550 million. Meanwhile, gains of equity investment and changes at fair value amounted to RMB1.882 billion, up 201% y-y approximately.

As one of major three key strategies, IS's research ended up at the sixth best domestic research team in 2014 from the seventh in 2013, the management stated IS would continue to focus on investment and research, not only for the public funds, but also for the private funds and overseas clients.

IS's asset also increased largely, total assets grew around 102% y-y to RMB73.488 billion, and net assets increased by 13% to RMB14.683 billion, with the parent company's net capital of RMB13.571 billion. Due to the rapid growth of businesses currently, IS faces the large demand of the capital, and therefore the Group announced the rights issue of RMB10-15 billion in A Shares, and the capital pressure would go down obviously after the rights issue. However, the profits should be diluted in the next two years due to the increase of the capital, and we estimate IS's net profit would maintain the rapid growth as over 100% in 2015.

Recently, CSRC stated domestic banks would have the license of brokerage in future, and the market believe it would increase the competitive pressure to brokerage firms, bur the management said the network advantage of banks would be diminished under the current development trend of internet finance, the key is the professionalization of the service and quality.

IS is one of domestic brokerage firms who gains the qualification of internet business. The management stated that the Group was studying the realistic strategy, and the key was the changes of the business culture and concepts of the management, and the construction of the service platform. Internet finance will mainly rely on the customer experience, and the competitive advantage is the differentiation strategy, and IS will focus on the private wealth management and institutional investors. Due to the high base of the clients in the private wealth management, IS made great efforts to develop the products, including the construction of the product platform, IT, R&D of mobile terminal, and the construction of the industry platform and so on.

Risk

The large volatility of profits of stock brokerage business and investment banking business;

Capital pressure increases due to the growth of the financing demand, which affects the business development in future;

The increase of the competition in the industry, with the lack of the talent reserve, and the experience of internationalization;

Share price decreases sharply due to the deterioration of markets in the short run.

FINANCIALS

Click Here for PDF format...