|

|

|

*Advertisement* |

|

|

|

|

|

25 Mar, 2015 (Wednesday) |

BAIC MOTOR(1958)

Analysis¡G

BAIC Motor (1958) announced the first results after listing, which revenue increased by 3.4 times to RMB 56.37 billion; profit attributable to shareholders increased by 66.2% to RMB 4.51 billion. The sales of BAIC`s own brand achieved 309,600 units, an increase of 53.1%, the segment loss narrowed sharply from RMB 977 million in 2013 to RMB 68.92 million. The Group will have a number of new car launching this year, including Saab D80, Saab X65, Saab X55, Saab C33, Saab CC, the new generation of Beijing Benz GLK SUV, the standard-wheelbase type new C-Class sedan, GLA SUV and the ninth generation Sonata of Beijing Hyundai etc. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $9.00, Target Price: $10.00, Cut Loss Price: $8.40

|

|

HI SUN TECH(818)

Analysis¡G

Inland bankcard transaction value under the consumer segment has been increasing greatly. Meanwhile, the mobile payment business is more robust. We believe that this will provide broad growing space for the market of the third-party offline merchant-acquiring business. With the e-payment environment becoming more mature, the specialized third-party payment institutions are expected to occupy a larger share of the merchant-acquiring market. Hi Sun Technology holds the third position in this industry and is predicted to benefit from the trend. What`s more, the SXF of the company has been approved to take in new merchants, the volume of its POS installing may double in 2015. With the release of the scale effect, the profitability of this business is expected to obviously promote.

Strategy¡G

Buy-in Price: $2.52, Target Price: $3.00, Cut Loss Price: $2.28

|

| |

|

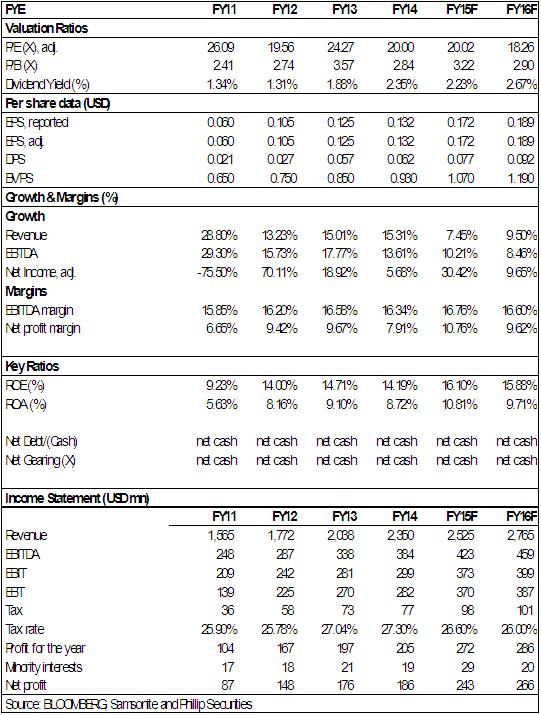

Samsonite International SA (1910.HK) - Better performance in 2014 than forecast

Summary-The result of Samsonite in 2014 shows that the sales revenue reaches up to 2.351 billion dollars with a growth of 15.4% yoy, which is the new revenue record. The EBITDA reaches up to 384 million with a growth of 13.8% yoy. And the profits that the shareholders should occupy reach up to 186 million dollars with a growth of 5.8% yoy. The net sales and EBITDA of Samsonite exceed our expectations by 2.8% and 1.3% respectively. The profit margin of EBITDA is 16.4%, a little lower than our expectation of 16.6%. Overall, the result of Samsonite is a little higher than our expectation. -In this period, the revenues of Asia, North America, Europe and Latin America have growths of 16.1%, 22.4%, 8.3% and 5.7% yoy respectively. The businesses in Latin America and Europe are significantly affected by the exchange rate fluctuation. From the perspective of brand division, the revenue proportion of the core brand Samsonite has reduced from 69.4% in 2013 to 65.3%, which reflects the brand diversification trend of the company. The new acquired brands Speck and Gregory have contributed revenue of more than 100 million dollars, the revenue proportion of which is 8.3%. -Samsonite has completed the acquisitions of three brands in 2014, see details in the above table. We can see that Samsonite is walking forward firmly on the road of diversification of products and brands, which provides potential power for the business development and result growth of the company in emerging markets. In finance, the three transactions` takeover price altogether equals to about 200 million dollars. In 2014, 110 million dollars of revenue and 1.1 million dollars of profit were made. Although it is hard to describe the acquisition price is cheap, it is good for rising the enterprise's value and establishing more advantages in competitions. -In 2014, the liability scale of Samsonite increased and the total liability was amount to 67 million by the end of the period, which grew 346% compared to the 15 million at the end of 2013; mostly on account of the remarkable rising short-term liability, the leverage ratio increased from 1.3% in 2013 to 5.2%; however, due to that the liability scale is relatively small, the whole is still in the state of net cash. At the end, the company's cash dropped from 225 million to 140 million dollars. -Samsonite continuously carries out acquisition to make its product and brand combinations diverse and effectively expand its "defense river" for competition. Yet, the company's steady balance sheet benefits from lower financial leverage, limited capital costs and sufficient cash flow; it is good for helping the company to establish more advantages in competitions. Organic growth and denotative expansion drive Samsonite's continuous and healthy growth. We maintain Samsonite's "Accumulate" rating with 30HKD target price for 12 months, equivalent to 20 times and 18 times of 2014 and 2015's prospective PE ratio. Financials

Click Here for PDF format...

| Recommendation on 25-3-2015 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 26.550 | | Suggested purchase price | N/A | | Target Price | $ 30.000 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | Industrial Bank | | 24/03/2015 | Buy | 25 | 17.63 | | Ping An Insurance (Group) Company of China | 2318 | 16/03/2015 | Buy | 105 | 83.5 | | | Dongfeng | 489 | 12/03/2015 | Accumulate | 14 | 11.82 | | China Southern Airlines | 1055 | 05/03/2015 | Neutral | 3.79 | 3.65 | | | COUNTRY GARDEN | 2007 | 18/03/2015 | Accumulate | 3.3 | 2.9 | | Gemdale Group | 600383 | 11/03/2015 | Accumulate | 9.8 | 9.14 | | | CPIC | 2601 | 11/11/2014 | Buy | 33.7 | 28.1 | | New China Insurance | 1336 | 15/08/2014 | Buy | 36.6 | 28 | | | FORTUNE REIT | 778 | 14/10/2014 | Accumulate | 7.32 | 6.92 | | Hysan Development | 0014 | 18/03/2014 | Accumulate | 36.8 | 33.35 | | | Wisdom Group | 1661 | 05/01/2015 | BUY | 6.55 | 4.6 | | Galaxy Entertainment | 27 | 19/11/2014 | Accumulate | 56 | 51.75 | | | Huaneng Renewables | 958 | 23/03/2015 | Accumulate | 2.9 | 2.7 | | Xinyi Glass | 868 | 19/03/2015 | Accumulate | 5.29 | 4.71 | | Food, Beverage and Retail | | | |

| | Samsonite International SA | 1910 | 25/03/2015 | Accumulate | 30.00 | 0.000 | | Guizhou Yibai Pharmaceutical | 600594 | 20/03/2015 | Accumulate | 53.46 | 44.59 | | | Hi Sun Technology | 818 | 13/03/2015 | BUY | 2.86 | 2.2 | | ZTE | 763 | 26/02/2015 | BUY | 21.24 | 17.1 | | | SPT Energy | 1251 | 24/02/2015 | Reduce | 1.5 | 1.74 | | CIMC ENRIC | 3899 | 27/10/2014 | Buy | 10 | 7.67 | | | Goldpac Group | 3315 | 18/02/2015 | N/A | | 4.77 | | KINGDEE INT`L | 268 | 02/12/2014 | Accumulate | 2.75 | 2.45 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2015 Phillip Securities (HK) Ltd. All Rights Reserved.

|