-During the 7-day Spring Holiday, CSA's passengers for international routes and Hong Kong/Macao routes have reached more than 270,000 with up over 20% yoy, Mainly benefiting from the hot demand of outbound tourism.

-Plus with the continuous low oil price, it is expected that the results of the company in 1Q2015 will be significantly improved.

-CSA's Jan passengers` turnover is up 7.6% yoy, among which the international routes is up 20% yoy. Both traffic and capacity grew fast for international routes.

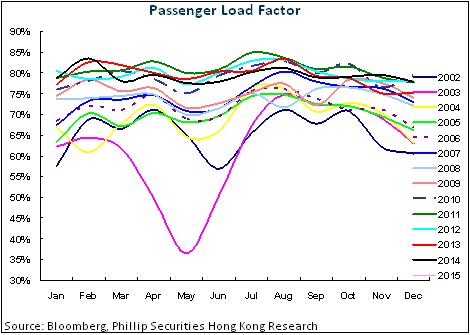

-Jan P L/F decreased by 0.5 ppts to 78.3%, which is the smallest falling range among the Big-threes. The international routes and regional routes increased respectively by 1.5 ppts and 5 ppts yoy and amounted to 79.3% and 73.2% respectively, both of which rank first among the Big-threes. The domestic routes down 1.3 ppts yoy and fell to 78.2%.

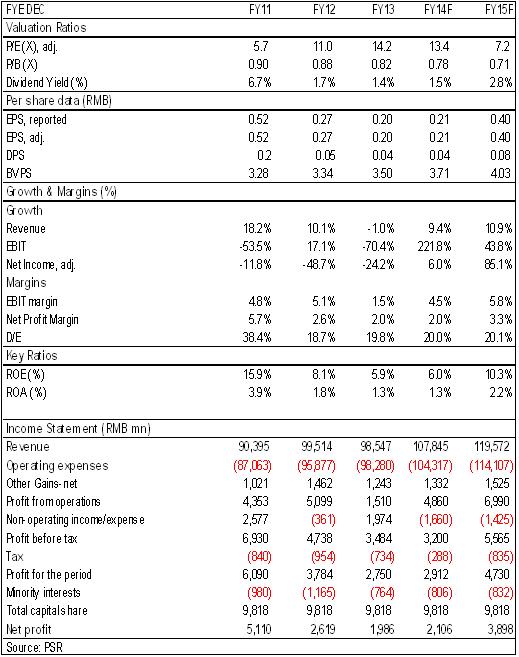

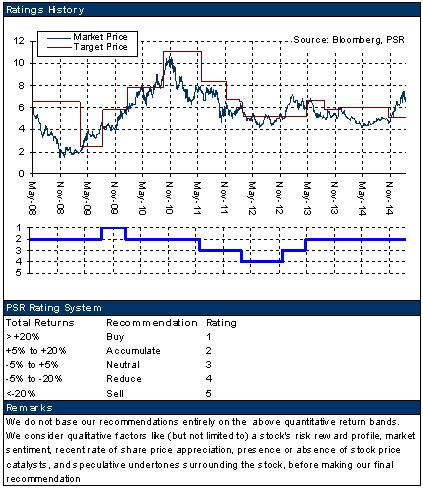

-And we accordingly revised the target price to 3.79, respectively 14/7.5x P/E and for 2014/2015. The positive factors have been priced-in. We maintain the "Neutral" rating.

Better-than-expect outbound tourism ignites the Spring Festival

We`ve learned that benefiting from exchange depreciations of many multiple currencies against RMB, the travel and shopping costs in Russia, Japan, South Korea, Europe, Australia, etc. have decreased. Coupled with the favorable factors of easier visa rules as well as consumption upgrading, the number of Chinese visitors of outbound tourism has a spurt this Spring Festival. There are different levels of increases in short-range routes of Southeast Asia and North Asia and long-range routes of Australia and America. Take CSA as an example: during the seven-day holiday of this Spring Festival, the international routes and Hong Kong/Macao routes of this company have transported passengers of more than 270,000 person-times with up over 20% yoy. Among them, the number of passengers that transferred from Guangzhou exceeded 58000 with up 16.8% yoy.

The operation data of January is the best in the industry

The operation data of January of CSA shows that: the passengers` turnover is up 7.6% yoy, among which the international routes is up 20% yoy. Under the background of sharply increased capacity, the international routes maintained a double-digit growth for 24 months. The Hong Kong/Macao routes grew 17% yoy, and the domestic routes rose 3.78% yoy. The capacity supply is up 8.3% yoy, and the international, Hong Kong/Macao, and domestic routes rose 18%, 9% and 5.5% yoy respectively. Because of the more capacity, the overall passenger load factors decreased by 0.5 ppts to 78.3%, which is the smallest falling range among the three major airlines.

On a closer look, the passenger load factors of the international routes and regional routes increased respectively by 1.5 ppts and 5 ppts yoy and amounted to 79.3% and 73.2% respectively, both of which rank first among the Big-threes. The load factor of the domestic routes down 1.3 ppts yoy and fell to 78.2%, which is far higher than the 76.5% of CEA but slightly lower than the 78.6% of AC.

The results for 1Q15 will be improved significantly

Just as the previous analysis, benefiting from the boom of outbound tourism and the continuous low oil price, it is expected that the results of the company in 1Q2015 will be significantly improved. For the future outlook, we consider that the Strategy of "The Canton Route" of CSA aiming at strengthening its international business has being pushed forward to a new high level and the company has elevated itself to a new higher footstep in terms of brand, market share and profitability. On the other hand, the third runway of Baiyun International Airport was officially put into use at the beginning of this year. It will greatly increase CSA's flight capacity in Guangzhou and improve the operational efficiency after the run-in period ends. However, we still predicted the fact that relatively weak domestic macro economy, the restriction on the three kinds of expenditure using public funds and the expansion of the high speed railways will still constitute restraints on the demand for the domestic routes of CSA in future.

Valuation

Considering the reduced fuel cost, we revised EPS forecast to RMB 0.21/0.40 of 2014/2015. We accordingly lifted our target price to HK$3.79, respectively 14/7.5x P/E for 2014/2015. We maintain our "Neutral" rating.

Financials

Click Here for PDF format...