In the first three quarters, the company recorded revenue of 8.139 billion HK dollars, which was up 9.5% yoy, and the net profit belonging to the parent company was 920 million HK dollars, which was up 21.2% yoy. After deducting the antibiotic business sales which was separated from the parent company in 2013, the actual revenue growth was 15.9%, and the net profit increase excluding nonrecurring items was also as high as 41.6%.

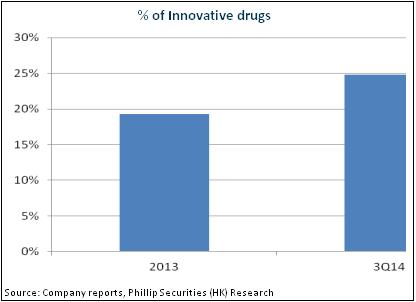

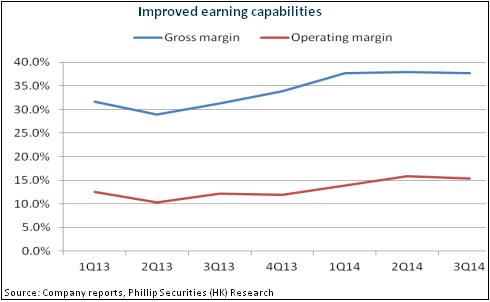

The outstanding achievement was mainly attributed to the strategic transformation that has been constantly promoted in recent years, i. e. the transformation from bulk drug to innovative drugs. In the first three quarters, the innovative drugs increased by 47.8% as a whole which also optimized the company's product structure and promoted the improvement of profitability. The gross profit margin increased by 7.1 percentages to 37.8% on a yoy basis.We believe that it is a high probability to achieve the target that management authority maintains the profit growth target of 30% in 2015. The existing innovative drugs are expected to continue to maintain high-speed growth momentum. Furthermore, the company has an abundant production line reserve, and the company is expected to launch several first-class new drugs into the market in succession in the coming years. Recently, the antitumor drug, Imatinib Mesylate has obtained the written approval from CFDA, thus the company becomes the third manufacturer in China who has obtained the generic drug approval.

Innovative drugs recently get support from favorable policies continuously. The NDRC announced to abolish the setting of maximum drug retail price, and the pricing power of innovative drugs will be promoted. Besides, the National Health and Family Planning Commission has recently planned to recommend 18 drug varieties under special support including Famitinib as priority review varieties; and among them, CSPC's SKLB1028 that has been applied for clinical trials is also included. We think that it may be a try of adjusting the evaluation method of new drugs. The declaration period of new drugs is expected to be shortened, innovative drug companies such as CSPC are expected to save plenty of time and costs, and the progress of new drug listing may be accelerated.

Rating Accumulate for attractive valuation

The continued rapid growth in the past two years proved the success of the company's strategy of transformation to innovative drugs. The strong research and development strength and product reserve will support the sustained growth. And the management authority's accumulation of over 600 million shares in October also showed their confidence to the company. We grant the company a valuation corresponding to 28X 2015EPS, with a target price of 7.77 HK dollars, and raise the rating to "Accumulate".

Rapid growth in 3Q14

According to the third quarterly report of CSPC, in the first three quarters, the company recorded revenue of 8.139 billion HK dollars, which was up 9.5% yoy; and the net profit belonging to the parent company was 920 million HK dollars, which was up 21.2% yoy. But, after deducting the antibiotic business sales which was separated from the parent company in 2013, the actual revenue growth was 15.9%, and the net profit increase excluding nonrecurring items was also as high as 41.6%, maintaining the momentum of high speed growth.

The outstanding achievement was mainly attributed to the company's strategic transformation that has been constantly promoted in recent years, i. e. the transformation from bulk drug to innovative drugs. In the first three quarters, the innovative drugs increased by 47.8% as a whole to 2.02 billion HK dollars. Among them, the flagship products (including NBP, Oulaining and Xuanning) recorded a total revenue growth of 39% yoy, and the oncology drugs gained the revenue up to 181 million HK dollars. At the same time, the faster growth of the innovative drugs optimized the product structure and also promoted the improvement of profitability. The gross profit margin increased by 7.1 percentages to 37.8% on a yoy basis.

But, because the major new drugs were still in the promotion period, the number of hospitals covered by the new drugs increased; for example, Duomeisu, jinyouli and Ailineng respectively covered 24, 27 and 11 new hospitals, which increased the marketing expense, with the expense ratio increasing from 12.8% to 15.8% on yoy basis, partially influencing the performance. Because promotion is still needed in supporting new drugs, we expect that the marketing expenditure rate would still remain at a high record of over 15.5%.

Innovative drugs will support the continuous increase

Recently, the company management authority maintains a profit growth target of 30% in 2015, among which, the growth of NBP is more than 30%, the growth of Oulaining and Xuanning are over 20%, and the growth of oncology drugs is expected to be doubled. Generally speaking, we believe that the probability of realizing the company target is relatively high.

At first, it is expected that innovative drugs will still keep rapid growth momentum. For example, oral tablets of NBP penetrate only 1300 hospitals at present and have potential to be expanded in the future. Duomeisu, a flagship product of antitumor drugs, is expected to continue to compete for market shares. Although it has not been a long time since this drug was launched into the market, the sales in a single quarter have reached 40 million HK dollars. Estimated annually, the drug would have been a type with its sales of over 0.1 billion HK dollars.

Secondly, company product line has rich reserves, mainly focusing on medical fields such as anti-infection, cardiovascular and cerebrovascular diseases, neuroses and psychoses, diabetes and antitumor and so on. Currently, there are 170 new drug research and development projects going on, among which 25 projects are about first-class new drugs and 34 are about domestic pioneered new drugs.

In the coming years, the company expects that many first-class new drugs will be listed in succession. Recently, an antitumor drug Imatinib Mesylate acquired CFDA approval document. This company is the third domestic manufacturer who got the approval document for generic drugs, having a wide market. In addition, for "Sofosbuvir Tablets", all preclinical studies have been completed and clinical study application has been reported to Center for Drug Evaluation of China Food and Drug Administration. The drug, at present, has not been approved for import in China. Besides, no domestic enterprises have got approval for production. CSPC may become the first company to get approval for listing Sofosbuvir Tablets.

Policy Support for Innovative Drugs

Generally speaking, innovative drugs recently get support from favorable policies continuously. Except for innovation encouragement of the country, NDRC (National Development and Reform Commission) has also announced the abolishment of setting the highest drugs retail price. Thus the pricing power of innovative drugs will be promoted.

Moreover, in order to speed up the progress of producing significant special innovative achievements of important new drug preparation technology, recently, National Health and Family Planning Commission has planned to recommend 18 drug varieties under special support such as famitinib to become the priority review varieties, and among them, CSPC's SKLB1028 (a multitargeted tyrosine kinase inhibitor used for the treatment of non-small cell lung cancer and acute meroblastic leukemia) that has been applied for clinical trials is also included. We think that it may be a try of adjusting the evaluation method of new drugs. The declaration period of new drugs is expected to be shortened, innovative drug companies such as CSPC are expected to save plenty of time and costs, and the progress of new drug listing may be accelerated.

Catalyst

New drug expansion exceeds expectations;

More supporting policies.

Risks

Bidding progress is uncertain from place to place;

Sales of innovative drugs slow down.

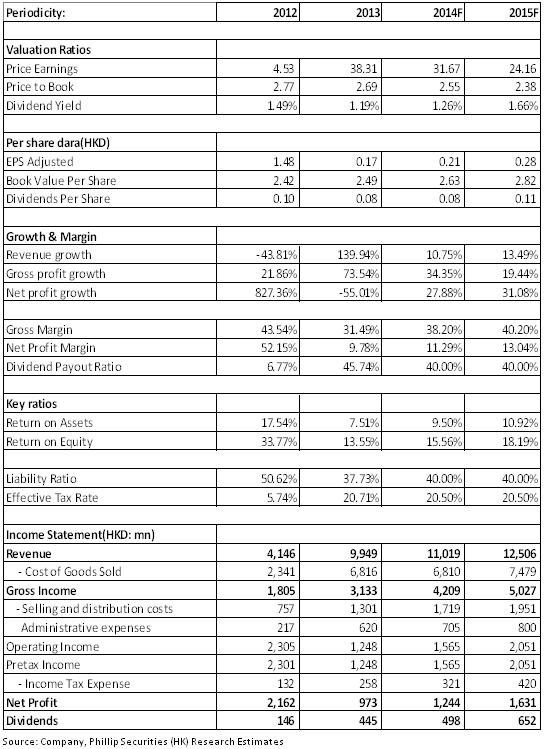

Financials

Click Here for PDF format...