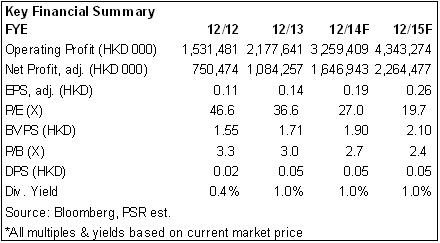

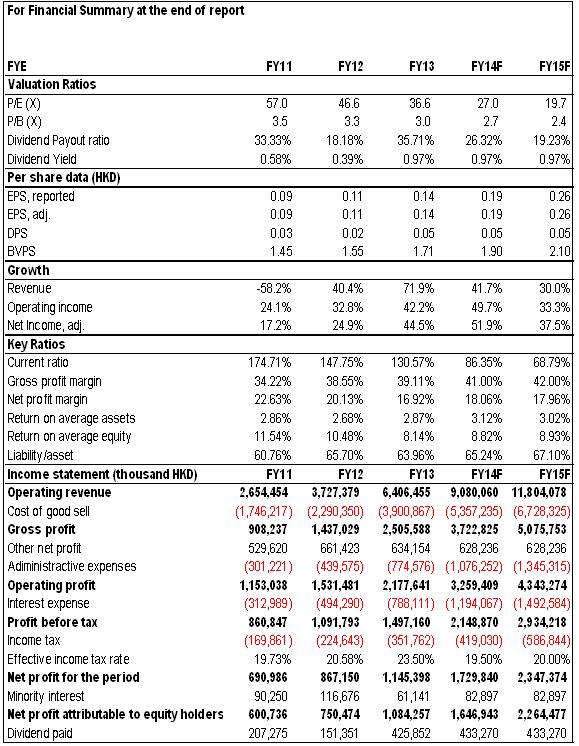

-The Company¡¦s revenue amounted to HK$3.815 billion in 1H2014, up 38% y-y, the gross profit was HK$1.596 billion, increased by 44% y-y with the gross margin of 41.8%, slightly higher than that of 1H2013, and net profit achieved to HK$714 million, up 39% y-y, equivalent to the EPS of HK$8.31 cents, higher than our expectation.

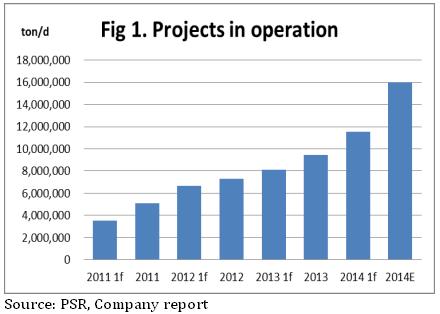

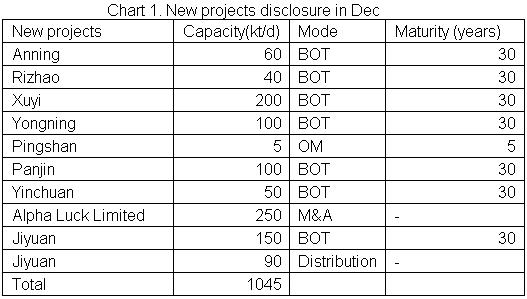

-In domestic projects, total design capacity achieved to 17.98 million tons/day in 1H 2014, increased by 1.334 million tons/day compared with the end of 2013. The capacity under operation was 11.53 million tons/day, up 2.104 million tons/day, increased by 22%, we believe the growth of projects under operation would maintain over 30% in the next three years. The project which were not put into operation was 6.45 million tons/day, down 0.77 million tons/day, mainly due to the large quantity of projects had already been put into operation. The Company announced to sign 10 new projects on 8th Dec, with the capacity of 1.045 million/day. The capacity of newly added projects was 3.80 million tons/day including new projects of 2.76 million tons/day before 30th Oct. We expect the capacity of new projects would achieve to 3 million/day annually in future.

-The Company¡¦s incomes in sewage treatment business was HK$1.48 billion in 1H, up 74%, and the construction income of BOT project amounted to HK$1.36 billion, up 240% sharply, the Company had 50 projects under construction, and would have more projects put into operation in the next two years. Construction and service incomes of comprehensive treatment projects was HK$420 million, down 69% y-y largely, and we can see the Company focused on the construction and operation in BOT project.

Investment Action

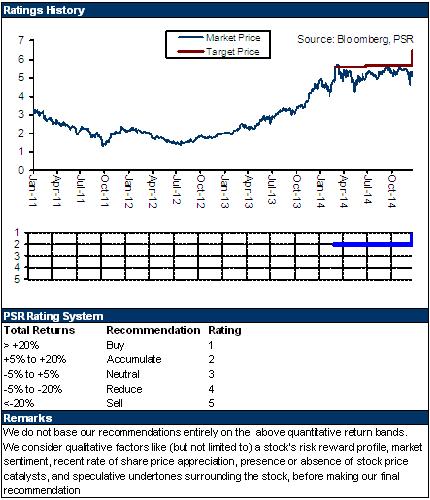

The Company is a leader of domestic water service enterprises, and sewage treatment industry will develop rapidly in the next two years benefited from the national environmental policies, the quantity of the Company¡¦s projects under construction and new projects maintain at the high level, which would increase rapidly as expected. We increase the Company¡¦s 12-month target price to HK$6.45, equivalent to 25xP/E in 2015E, recommend Buy rating.

Better-than-expected performance

The Company¡¦s revenue amounted to HK$3.815 billion in 1H2014, up 38% y-y, the gross profit was HK$1.596 billion, increased by 44% y-y with the gross margin of 41.8%, slightly higher than that of 1H2013, and net profit achieved to HK$714 million, up 39% y-y, equivalent to the EPS of HK$8.31 cents, higher than our expectation.

Rapid growth of the projects

In domestic projects, total design capacity achieved to 17.98 million tons/day in 1H 2014, increased by 1.334 million tons/day compared with the end of 2013. The capacity under operation was 11.53 million tons/day, up 2.104 million tons/day, increased by 22%, we believe the growth of projects under operation would maintain over 30% in the next three years. The project which were not put into operation was 6.45 million tons/day, down 0.77 million tons/day, mainly due to the large quantity of projects had already been put into operation. The Company announced to sign 10 new projects on 8th Dec, with the capacity of 1.045 million/day. The capacity of newly added projects was 3.80 million tons/day including new projects of 2.76 million tons/day before 30th Oct. We expect the capacity of new projects would achieve to 3 million/day annually in future.

Large profit growth of businesses

The Company¡¦s incomes in sewage treatment business was HK$1.48 billion in 1H, up 74%, and the construction income of BOT project amounted to HK$1.36 billion, up 240% sharply, the Company had 50 projects under construction, and would have more projects put into operation in the next two years. Construction and service incomes of comprehensive treatment projects was HK$420 million, down 69% y-y largely, and we can see the Company focused on the construction and operation in BOT project.

Valuation

The Company is a leader of domestic water service enterprises, and sewage treatment industry will develop rapidly in the next two years benefited from the national environmental policies, the quantity of the Company¡¦s projects under construction and new projects maintain at the high level, which would increase rapidly as expected. We increase the Company¡¦s 12-month target price to HK$6.45, equivalent to 25xP/E in 2015E, recommend Buy rating.

Click Here for PDF format...