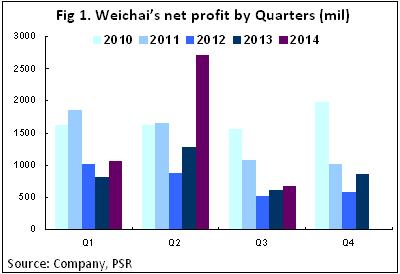

-Q3's revenue upped 77.5% yoy to 22.034 billion, and the net profit attributable to the parent company was 680 million, an increase of 9.8% yoy, with EPS of 0.34 YUAN, which was 0.31 YUAN over the same period of last year. The Weichai revenue rate of increase was 26.5% yoy in first quarter and was -1.6% yoy in the second quarter. The growth rates of net profits attributable to the parent company were 29.7% and 113% respectively, with a corresponding EPS of 0.53 YUAN and 1.36 YUAN respectively.

-The revenue of the first three quarters increased nearly 30% yoy to 56.148 billion. The net profit attributable to the parent company was 4.445 billion, upping 64% yoy, with EPS of 2.22 yuan, which was 1.35 yuan in 2013M9. If the disposable investment income brought by consolidating financial statements with KION was excluded, the net profit of the first three quarters was approximately 3.156 billion, upping 16.7% yoy, with corresponding EPS of 1.58.

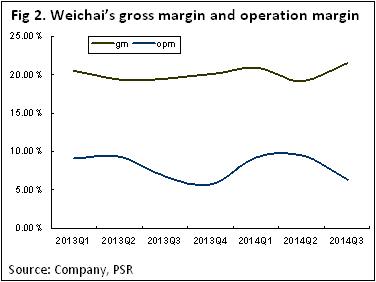

-The overall gross margin of Weichai of the first three quarters improved by 0.74 ppts to 20.93%; and the gross margin of each of the first three quarters are 21.4%, 19.5% and 21.7%.

-However, headquarters` heavy truck engine's profitability does not appear to be positive. Although the headquarters` income still maintains a slightly increase, the gross margin apparently worsens.

How we view this

The greatly increased profit of the second quarter was mainly caused by the disposable investment income of 1.67 billion brought by including KION in the consolidated financial statement, and the income of the third quarter increased greatly was largely because that KION started the financial statement consolidation in this quarter.

In November of this year, the construction project of Linde Hydraulics Weifang Plant was officially launched. With benefits from the upgrade trend to import substitution of Chinese high-end equipment manufacturing industry, we are optimistic about the profit contribution generated by launch of Linde Hydraulics equipment.

Investment Action

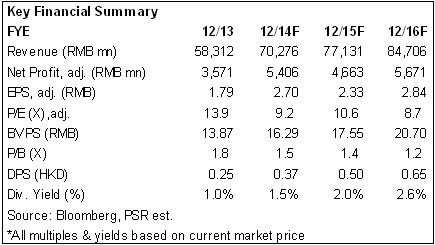

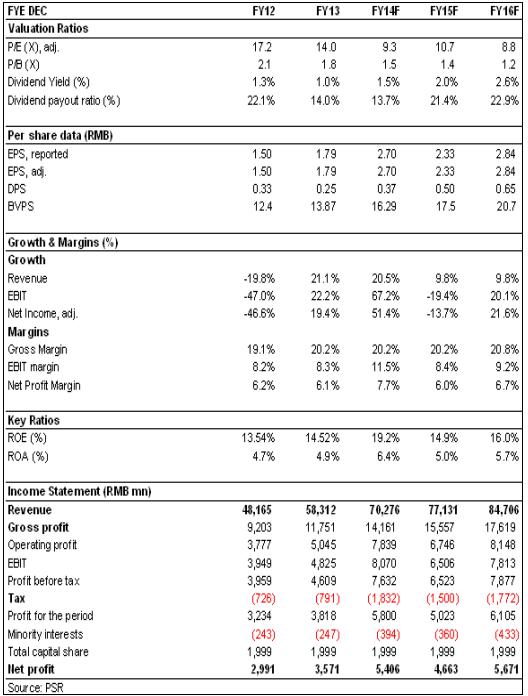

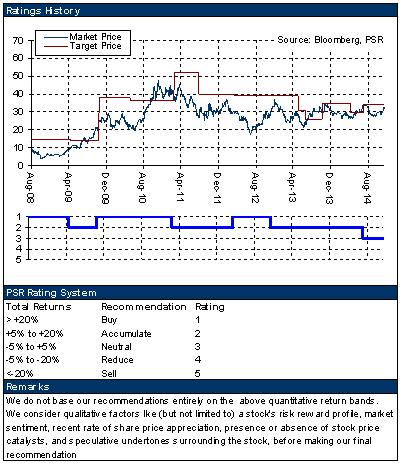

According to the analysis above, we revised our target price to HK$35, based on 10.2/11.8/9.7xP/E and 1.7/1.6/1.3xP/B in 2014/2015/2016, and the suggestions of ¡§Accumulate¡¨ rating be given.

Review of Q3's performance

Q3's result of Weichai Power grew steadily. The revenue upped 77.5% yoy to 22.034 billion, and the net profit attributable to the parent company was 680 million, an increase of 9.8% yoy, with EPS of 0.34, which was 0.31 over the same period of last year. The Weichai revenue rate of increase was 26.5% yoy in first quarter and was -1.6% yoy in the second quarter. The growth rates of net profits attributable to the parent company were 29.7% and 113% respectively, with a corresponding EPS of 0.53 and 1.36 respectively. The greatly increased profit of the second quarter was mainly caused by the disposable investment income of 1.67 billion brought by including KION in the consolidated financial statement, and the income of the third quarter increased greatly was largely because that KION started the financial statement consolidation in this quarter. The revenue of the first three quarters increased nearly 30% yoy to 56.148 billion. The net profit attributable to the parent company was 4.445 billion, upping 64% yoy, with EPS of 2.22 yuan, which was 1.35 yuan over the same period of last year. If the disposable investment income brought by consolidating financial statements with KION was excluded, the net profit of the first three quarters was approximately 3.156 billion , upping 16.7% yoy, with corresponding EPS of 1.58 .

Although overall gross margin increased, the overhead rate also went up

Benefited from the improved sales structure brought about by KION consolidated supervision and updated emission standard, the overall gross margin of Weichai of the first three quarters improved by 0.74 ppts to 20.93%; speaking from the third quarter's conditions, the whole gross margin's improvement is remarkable, and the gross margin of each of the first three quarters are 21.4%, 19.5% and 21.7%. However, on the other hand, the expense ratio also rose after it. The growth of the first three quarters` sell + administrate expense upped 43.5% yoy or 2.1 billion, and the proportion of the sum of the two in the total income also improved by 1.2 ppts.

The headquarters` engine business shrinks

However, with the background of heavy truck industry keeping going down due to the soft macro economy at home, headquarters` heavy truck engine's sales volume also decreases, and the profitability does not appear to be positive. Although the headquarters` income still maintains a slightly increase, the gross margin apparently worsens. And in the third quarter, the headquarters` gross margin sharply declined to about 20% from about 30% in the past. Although the company strictly controlled the expense cost, in the third quarter, the headquarters` profit has downed 21% yoy.

Construction of Linde Project began: official launch of its transition strategy

In November of this year, the construction project of Linde Hydraulics Weifang Plant owned by Weichai Group was officially launched, marking the official set-up of high-end hydraulic localization project that will change the condition of long-term dependence on the import of Chinese high-end hydraulic product. The project is expected to be commissioned at the end of May next year, the production of 8000 units will be for Phase 1 and it is expected to be 80,000 units in 2018. With benefits from the upgrade trend to import substitution of Chinese high-end equipment manufacturing industry, we are optimistic about the profit contribution generated by launch of Linde Hydraulics equipment.

Investment Action

According to the analysis above, we revised our target price to HK$35, based on 10.2/11.8/9.7xP/E and 1.7/1.6/1.3xP/B in 2014/2015/2016, and the suggestions of ¡§Accumulate¡¨ rating be given.

Click Here for PDF format...