|

|

|

*Advertisement* |

|

|

|

|

|

19 Nov, 2014 (Wednesday) |

361 DEGREES(1361)

Analysis¡G

361 Degrees (1361) issued a profit alert, expecting consolidated operating profit will increase significantly this year, mainly due to the overall improvement of the receivables, thus no further impairment expenses. Its performance returned to growth in the first half, with revenue RMB 2.09 billion, an increase of 4.6%, while profit attributable to shareholders grew by 28.3% to RMB 263 million, which was already more than the annual profit in 2013. The Group previously announced the third-quarter operating data, the total order amount in 2015 spring / summer will receive 11% growth yoy, which was accelerated compared with 8% growth in 2014 winter orders. Moreover, the average selling price of loan products had increased, among which the sales footwear products was particularly improved due to the significant improvement in product quality. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $2.20, Target Price: $2.50, Cut Loss Price: $2.05

|

|

GOME(493)

Analysis¡G

Gome (493) announced the first three quarter results ended by the end of September, with turnover rose by 7.17% to RMB 44.645 billion, gross profit rose by 7.19%, consolidated gross profit margin stayed flat to 18.57%, net profit rose 74.7% yoy. Based on the financial data, Gome`s quarterly growth has slowed down, causing the share price to fall from September, and a slump on the day the company announced to buy 5.41% stake of Huishang Bank with $2.4 billion. However, the management believed that the acquisition was for integrating the platforms of procurement and logistics that supports online and offline business, and serve customers and suppliers from the financial aspects, which would help GOME to enter the big data era. Current valuation is still not too high, which forecasted PE is about 13 times.

Strategy¡G

Buy-in Price: $1.15, Target Price: $1.30, Cut Loss Price: $1.10

|

| |

|

Galaxy Entertainment (27.HK) - Q3 performance was driven by VIP powerfully

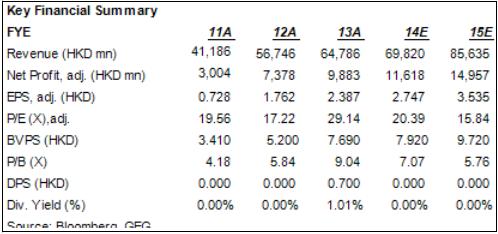

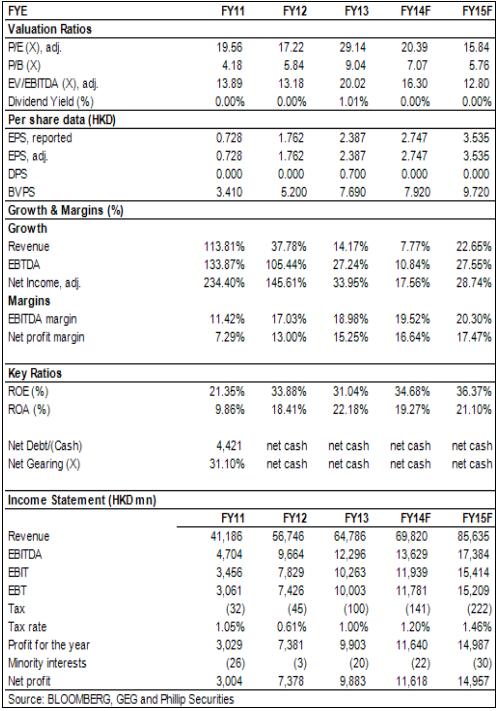

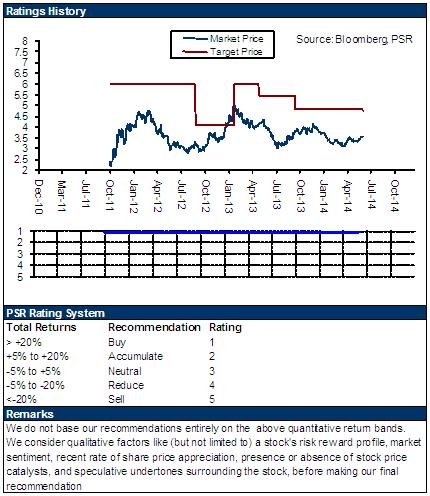

The Q3 performance of GEG showed that: the YoY income growth was 6%, reaching HKD17.3 billion. The YoY EBITDA growth adjusted was 1%, reaching 3.3 billion. The Q3 results are basically in line with the market expectations and even higher than that of the same trade or business; The speed increasing of VIP business is better than that of the same trade or business. The YoY growth of VIP gaming revenue of Galaxy Macau was 11%, reaching 7.2 billion, which is higher than the average growth rate of the industry. While the VIP business income of Star World Hotel declined by 2% to 4.4 billion. Thus, the overall YoY growth of VIP business was 5%, reaching 11.8 billion, which strengthened the relative competitive advantages of GEG. In addition, the growth of the midfield gambling and the slot machine increased by 12% and 6% to reach 4.8bn and 0.5bn respectively, which remains stable; The second phase of Galaxy Macau will be open in the middle period of 2015. So far, of the total capital expenditure plan of 19.6 billion, 9 billion has been put in. At present, the company holds the cash of HKD11 billion, and is in good condition of assets and liabilities; The YoY decline of the Macao gaming revenue in October 2014 was 23%, and the decline range exceeded market expectations, which is the worst level in history. We think that apart from the economic factors, the demonstrations in Macao and HK and the high base are also the main causes. We believe the YoY decline will be narrowed in several months this year, improving the confidence of investors. How we view thisWe believe the weakness in Macao gaming market will continue before the middle of 2015. However, we also believe the income decline range is expected to be narrowed gradually. While GEG is the best choice for Macao gaming stocks, both the VIP business and the midfield business are expected to win that of the same trade or business, while the profit rate can remain unchanged. Investment ActionWe believe that the valuation of GEG has a certain attraction, while it is constrained by the weakness of the whole gaming market. We maintain "Accumulate" rating of GEG with 12m TP at HKD56, which is equivalent to 12.8 times of the ratio of EV/EBITDA and 16 times of the prospective P/E ratio of 2015.

Click Here for PDF format...

| Recommendation on 19-11-2014 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 51.750 | | Suggested purchase price | N/A | | Target Price | $ 56.000 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | Huishang Bank | 3698 | 18/11/2014 | Buy | 4.1 | 3.34 | | China Construction Bank | 939 | 31/10/2014 | Accumulate | 6.5 | 5.72 | | | GAC Group | 2238 | 13/11/2014 | Accumulate | 8.52 | 7.47 | | Dongfeng Group | 489 | 05/11/2014 | Buy | 14.4 | 11.28 | | | China South City | 1668 | 04/11/2014 | Buy | 5.5 | 3.52 | | Wanda Commercial Properties Group | 169 | 29/09/2014 | Accumulate | 2 | 1.73 | | | CPIC | 2601 | 11/11/2014 | Buy | 33.7 | 28.1 | | New China Insurance | 1336 | 15/08/2014 | Buy | 36.6 | 28 | | | FORTUNE REIT | 778 | 14/10/2014 | Accumulate | 7.32 | 6.92 | | China State Construction International Holdings Ltd | 3311 | 16/05/2014 | Buy | 15.8 | 13.16 | | | Galaxy Entertainment | 27 | 19/11/2014 | Accumulate | 56.00 | 0.000 | | | Xinjiang Goldwind | 2208 | 10/11/2014 | Accumulate | 15.56 | 13.46 | | China Suntien Green Energy | 956 | 21/10/2014 | Buy | 2.33 | 1.93 | | Food, Beverage and Retail | | | |

| | Samsonite International SA | 1910 | 12/11/2014 | Accumulate | 31 | 27 | | Sa Sa International | 178 | 16/09/2014 | Reduce | 5.07 | 5.81 | | | AAC Technologies | 2018 | 17/11/2014 | Accumulate | 48.55 | 43.85 | | BYD Electronic | 285 | 07/11/2014 | Buy | 10.78 | 8.84 | | | CIMC ENRIC | 3899 | 27/10/2014 | Buy | 10 | 7.67 | | Anton Oilfield Service | 3337 | 10/10/2014 | Neutral | 2.2 | 2.29 | | | BOYAA | 434 | 14/11/2014 | Accumulate | 8.52 | 7.39 | | HC INTERNATIONAL | 2280 | 06/11/2014 | Buy | 14.92 | 8.8 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2014 Phillip Securities (HK) Ltd. All Rights Reserved.

|