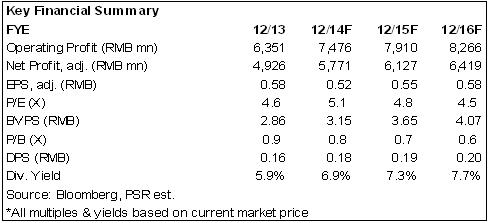

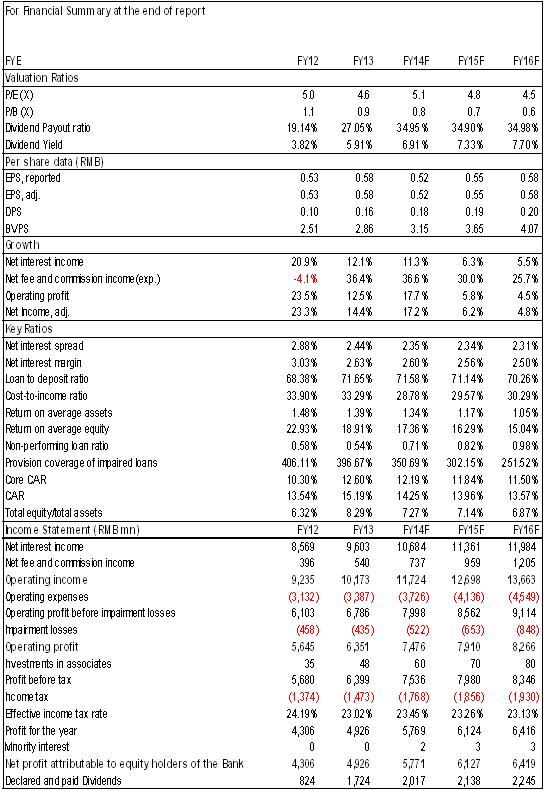

-In recent years, HSB¡¦s profit growth rate is higher than the industry average. From 2009 to 2013, its operating income increased at a CAGR of 21.99% from RMB4.594 billion to RMB10.173 billion. As at the end of 1H2014, HSB¡¦s net profit was RMB2.839 billion, up 15.78% y-y, and we estimate HSB¡¦s net profit growth rate will go up slightly in 2014 with the amount of RMB5.771 billion, up 17.15% y-y, equivalent to the EPS of RMB0.52, which would be lower than RMB0.58 in 2013 due to the dilution of the increased capital after the IPO in 2013;

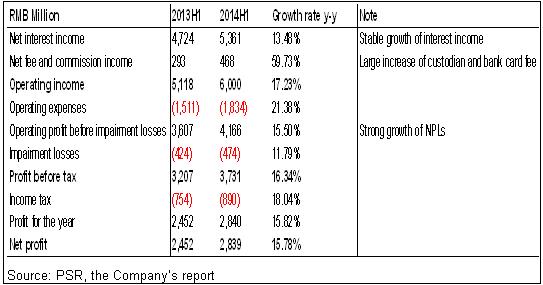

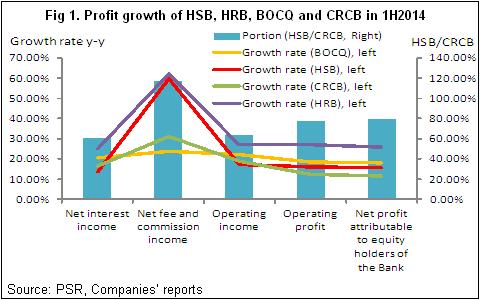

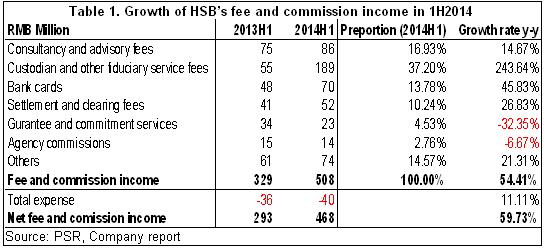

-By the end of 1H2014, HSB¡¦s net fee and commission incomes increased strongly by 59.73% y-y to RMB468 million, comparing with HRB¡¦s 62.37%, BOCQ¡¦s 24.00% and CRCB¡¦s 31.29%. The main reason of the strong growth was the sharp increase of custodian and bank card fees;

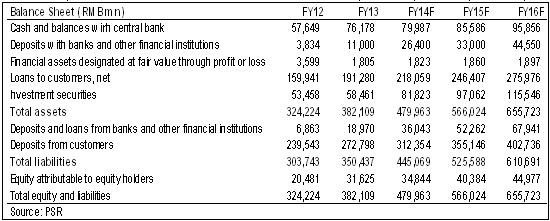

-HSB¡¦s assets increased strongly, as at the end of 1H2014, total assets increased by 15.93% to RMB442.966 billion compared with the end of 2013, and net assets grew 5.21% to RMB33.274 billion, with the BVPS of RMB3.01;

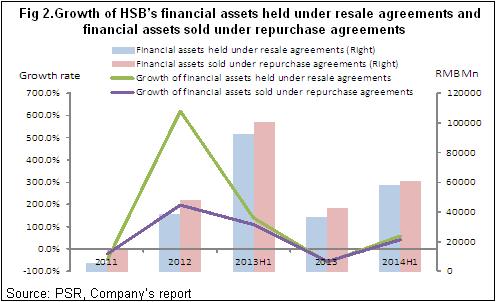

-One of the main reasons of large increase of assets is the significant growth of ¡§Financial assets held under resale agreements¡¨ and ¡§Investment securities classified as loans and receivables¡¨, which increased by 57.31% and 2160.08% to RMB57.848 billion and RMB16.363 billion respectively;

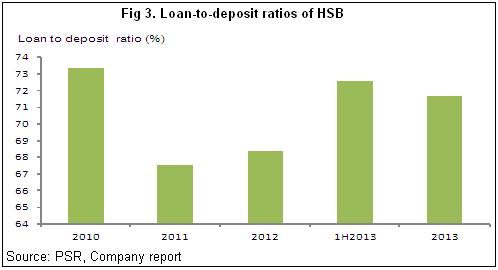

-In 1H2014, HSB¡¦s net loans increased by 8.33% to RMB207.222 billion compared with the end of 2013 while the deposits increased by 12.35%. The loan-to-deposit ratio dropped due to the larger growth of deposits, which decreased from 71.65% in 2013 to 69.10%;

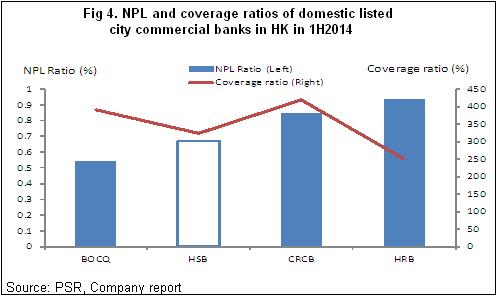

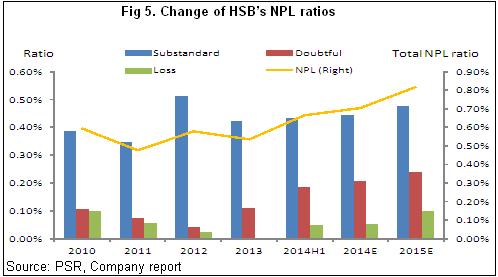

-HSB owns quite good ability of risk control, and both ratio and the amount of the NPLs are much lower than the peers, but started to go up. As at the end of 1H2014, the Group¡¦s NPL ratios increased from 0.54% in 2013 to 0.67%, and the ratios of allowance for impairment losses to NPLs dropped from 396.67% to 323.30%;

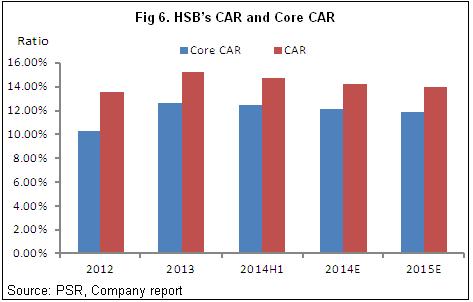

-By the end of 1H2014, according to the new method, HSB¡¦s CAR and Core Tier-1 CAR were 14.68% and 12.43%, still maintained at the high level although they decreased slightly, and we believe the ratios will go down this year;

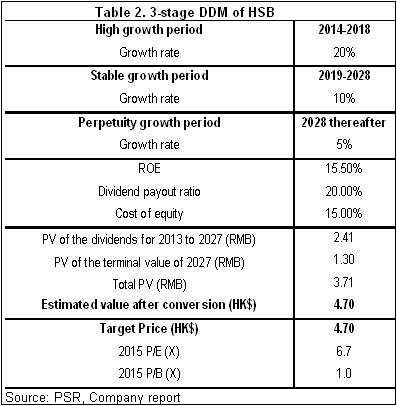

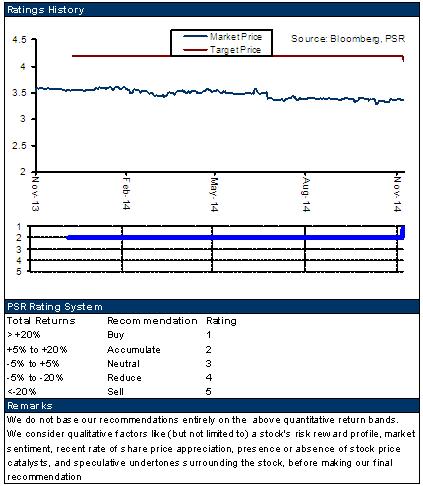

-According to 3-stage DDM and P/B method, we estimate the 12-m target price of HSB would be HK$4.10, around 22.8% higher than the latest closing price, equivalent to 5.8xP/E and 0.9xP/B in 2015 respectively, the valuation is attractive and we upgraded it to Buy rating.

How we view this

In all, HSB¡¦s performance maintained stable, especially for the strong growth of intermediate business incomes. The risks are under control although the asset quality trends to deteriorate in future.

Investment Action

Under the current lower valuation of the bank, we estimate the 12-m target price of HSB would be HK$4.10, around 22.8% higher than the latest closing price, equivalent to 5.8xP/E and 0.9xP/B in 2015 respectively, and the valuation is attractive.

Click Here for PDF format...