-Comba Telecom Systems (Comba) owns four product lines including wireless access, antennas & RF Sub, wireless enhancement, and wireless transmission, and has mastered key technologies in relevant fields. At present, the company has applied for more than 1700 domestic and foreign patents, and its overall product technical level has reached the leading position at home. According to the latest report released by the American market research institute EJL Wireless Research, Comba's market share of the base station antenna has been in the top three in the world for three years in a row, and it has been rated as the first-tier supplier of global base station antenna.

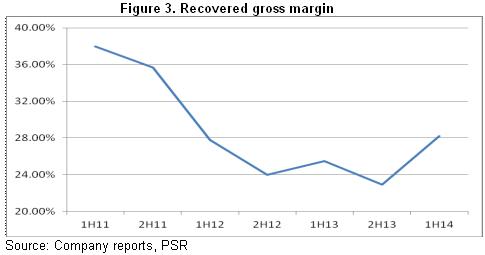

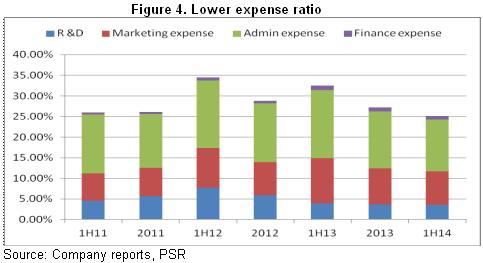

-The company began to turn losses into gains since the first half of 2014 with the net profit of 72.3 million HKD during this period, which was far better than the loss of 0.15 billion HKD in 1H13. It mainly benefited from the great increase of the base station antenna and relevant service because of the operators` implementation of 4G network construction, and the company's turnover increased by 39.8% by year to RMB 3.024 billion HKD. At the same time, the company's gross profit margin increased by 2.7 percentage points to 28.2%. Primarily, the change of product mix and the launching of high-end product made the gross profit margin improve by no less than 2 percentage points, and scale economies effect and effective cost control measures also made the operational expenses in total revenue decrease by over 5 percentage points.

-As the construction of 4G network is advancing rapidly in mainland, the company's antenna and subsystem business will still benefit from that.

-In the light of the construction speed of China Mobile, many big cities need to finish overall coverage of 4G network in 2015. Therefore, we anticipate that there will be many cities to enter the phase of deep coverage and network optimization from the second half of 2014, and Comba occupies the leading position in this market. Thus, its wireless enhancement service will also enter the new phase of accelerated contribution.

Investment Action

Benefited from the arrival of 4G investments and construction peak, Comba begins to turn losses into gains after losses for two years in a row. What deserves to be mentioned especially is that the company occupies the domestic leading place in the field of wireless optimization, and accelerated construction of network by China Mobile will drive the needs in this field to be released in advance.

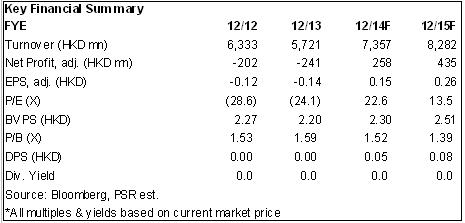

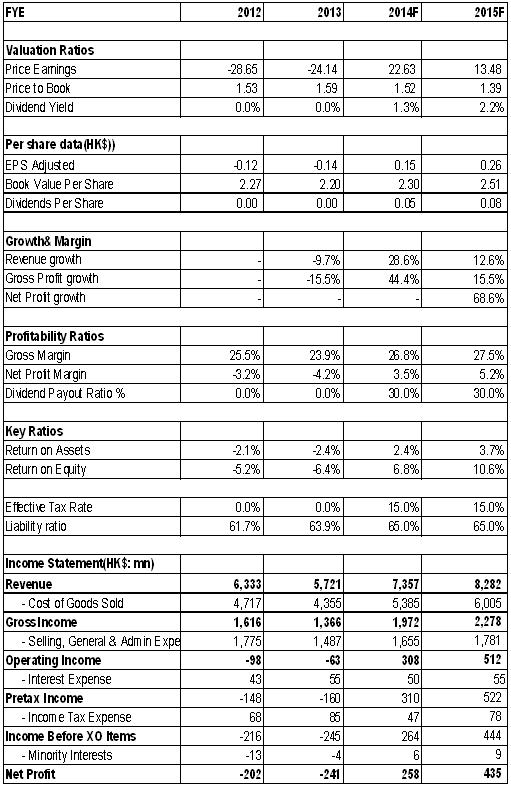

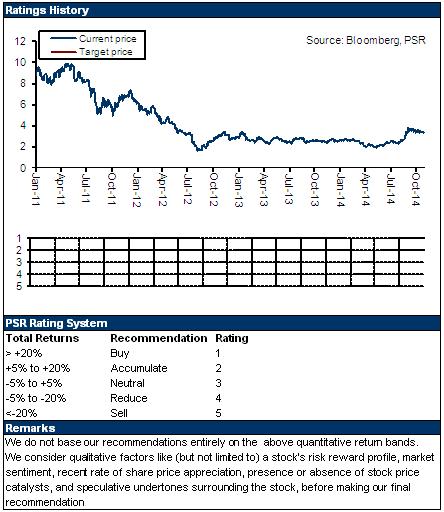

Based on the company's return to growth, we refer to PER method. Investigating the era of 3G, the company's trading range is 15-20X, we grant it 15X 2015EPS conservatively, with the target price of HKD3.88. We initially grant it "Accumulate" rating.

Technological superiority brings leading market share

Comba owns four product lines of wireless access, antennas & RF Sub, wireless enhancement, and wireless transmission, and has mastered key technologies in relevant fields. At present, the company has applied for more than 1700 domestic and foreign patents, and its overall product technical level has achieved the leading place at home and abroad. The company participated in drafting and formulating more than 30 national and industrial standards, which has highlighted its leading position in the industrial competition.

Early in the era of 3G, according to the analysis report of mobile communication in 2009 issued by American ABI, Comba was already in the top three of base station antenna of mobile communication, with the market share of 9%. While in accordance with the latest report released by the American market research institute EJL Wireless Research, Comba¡¦s market share of base station antenna has been in the top three in the world for three years in a row, and it has been rated as the first-tier supplier of global base station antenna.

What also deserves to be mentioned is that Comba arranged 2G/ 3G/ 4G LTE, iDEN and WiFi one-stop wireless solutions for the world cup's 8 stadiums out of 12 in The Brazilian World Cup 2014 and provided operation and maintenance guarantee service for the competition, which has gained high recognition from the Brazilian operators and also proved the company's competitiveness in the market abroad.

Turning losses into gains in the first half of 2014

At the end of the era of 3G, competition was intensified due to the reduction of investment by operators and the expansion of industrial homogenization. The company began to present its falling of earning capabilities and revenue since 2012, and the dilemma of losses was caused for two years in a row. Nevertheless, the company began to turn losses into gains since the first half of 2014 with the net profit of 72.3 million HKD during this period, which was far better than the loss of 0.15 billion HKD in 1H13.

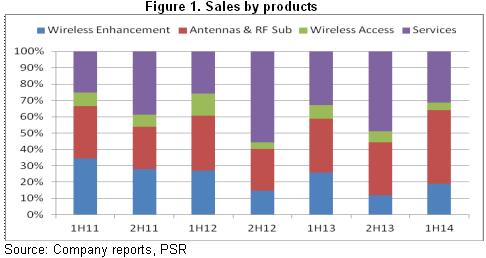

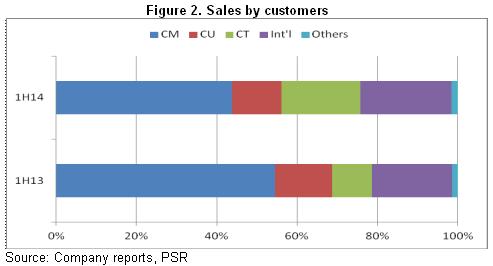

Specifically speaking, the company's turnover annually increases 39.8% to HK$ 3.024 billion, and it is mainly benefited from the 4G network construction promoted by the operators, which makes base station antenna and related services` businesses greatly increase; for instance, antenna and sub-system's business revenue increases 90.4% to HK$ 1.356 billion, accounting for 44.9% of the total revenue; the year-on-year growth of revenue from services is 32.8% to HK$0.945 billion, accounting for 31.3%. Concerning clients, the revenue from China Telecom sharply increases 177.8% to HK$0.596 billion, accounting for 19.7%; the revenue from international clients also greatly increase 58.7% to HK$0.685 billion, accounting for 22.7%; China Mobile has the biggest contribution with 43.8%, but its increase is relatively smaller with only 12.1%.

Moreover, the company's profitability is also improved. The gross margin increases 2.7 percentage points to 28.2%. It is mostly the change of product mix and the release of high-end products that make the margin increase no less than 2 percentage points. Meanwhile, effects of scale economy and effective measures of controlling costs leads to over 5 percentage points drop of expense ratio.

To benefit from the 4G industry chain continually

Generally speaking, the Mainland China's 4G network construction is being rapidly promoted. From the early stage of base station construction, we believe that the company's antenna and sub-system business will keep benefiting. China Mobile has already changed its goal of building 500 thousand 4G base stations by the end of 2014 to 700 thousand, and it is expected to be one million next year. China Unicom and China Telecom also received 16 cities` FDD LTE trial commercial license at the end of June, and it was expanded to 40 cities by the end of August. We estimate that the national commercial FDD LTE license will be granted within one year, and it is expected that the 4G base stations of the two companies will be the target of 300 thousand to 400 thousand in the next year. In fact, by the end of this September,

Comba has supplied about 560 thousand base station antennas which are 20 thousand more than that of last year.

Moreover, in the late stage of 4G network construction, it is about the construction of depth coverage, network optimization and the like. In the first half year, although the revenue of this branch of the company only increased 4%, according to China Mobile's construction speed, many major cities require that 4G network's overall coverage will be finished in 2015. Therefore, we expect that, starting from the next half year of 2014; many cities will enter the stage of depth coverage and network optimization. Especially in the 4G era, its frequency is higher than 3G frequency, making 4G radio wave's ability of diffraction worse, so greater demands for its depth coverage and network optimization are required compared to 3G.

At the moment, 4G network's depth coverage and network optimization mainly focus on indoor distribution. To solve that, there are two major means: first, applying the light distribution system; second, using new technology Small Cell. Comba has produced major products in both of the two aspects, among which, MDAS is the light distribution system that has been applied successfully in World Cup Brazil. Moreover, Comba's Small Cell, as a new product, has also been employed as an important pattern of 4G LTE network deployment by major mobile network operators all over the world. Hence, we estimate that the company will even more greatly benefit from the LTE construction both in the Mainland China and overseas from the next half year of 2014.

Catalyst

4G construction progress is beyond expectation;

More overseas orders.

Risk

More fierce competition leads to market loss.

Click Here for PDF format...