-The growth rate of passenger turnover in September was reduced to 5.2% on a yoy basis. The domestic routes, with a yoy growth rate increasing to 3.1% and a mom decrease of 9.4%; the international routes maintained a relatively rapid growth, but the growth rate dropped, with a yoy increase of 8.6% and a mom decrease of 10%; the regional routes were almost the same as the international routes, up 11.6% yoy and down 11.4% mom.

-The available seat kilometres increased by 7.7% yoy. There was a yoy growth of 4% in the domestic routes; other routes maintained a sharp growth trend. The international routes increased by 14% on a yoy basis, while the regional routes increased by 16.4%. These three all had a mom decrease of 8.7%, 2.7% and 5.1% respectively.

-The average P L/F in September is 79.4%, down 1.9ppts yoy, 2.7 ppts mom. The domestic routes reported an 80.8% P L/F, the minimum fallback of all routes, down 0.7ppts yoy and 0.6 ppts mom. P L/F of the international routes and regional routes decrease 3.9 and 3.1 ppts yoy because of excessive supply respectively, to 77.9% and 72.2%.

-Air China's freight business in September had strong performance, and its freight traffic rebounded greatly by 21.6% yoy and 16.3% mom. Domestic, international and regional routes` freight traffic grew by 0.2%, 30.6% and 31.1% yoy respectively, and by 11.25, 18.6% and -2.2% mom.

How we view this

Benefited from the effects of reducing costs and increasing demands, we predict that profitability improvement brought about by freight business rebounds will obviously show in its third-quarter's result that is to be released.In the coming two years, the company will have greater efforts to increase the transportation capacity, and it is scheduled to have a net increase of 22 airplanes, and is expected to increase the input of transportation capacity for remote routes of Europe and America, which is beneficial for sharing the fruit of the North America routes recovery. But the continuous flow diverting to high speed rails and the intensified industry competition will continue to challenge the improvement of demand-end profitability. On the other hand, the negative impact brought about by the cost-end fuel price and exchange rate factor is expected to diminish.

Investment Action

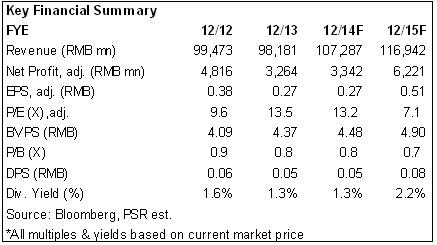

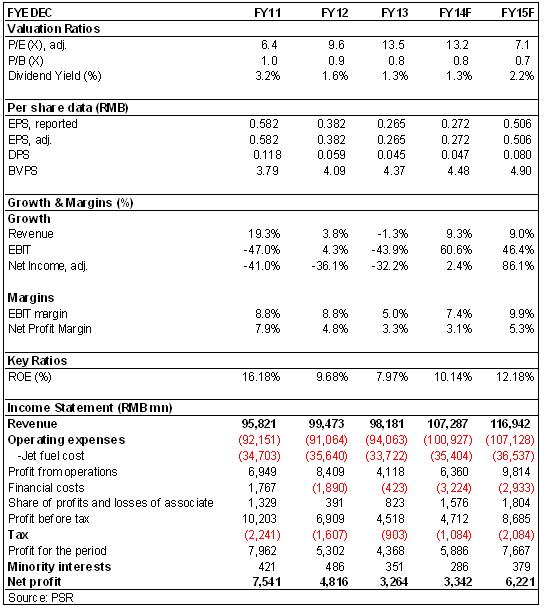

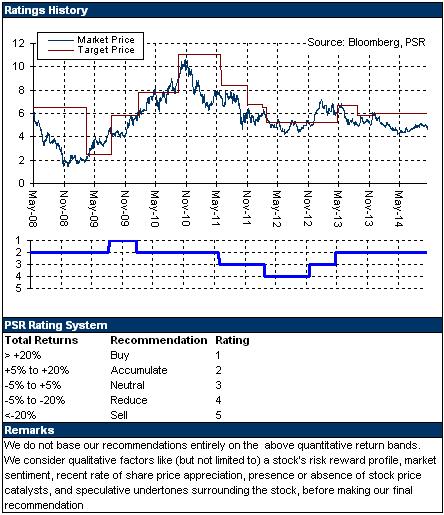

We revised the Company¡¦s estimated EPS to 0.272/0.506 in 2014/2015 respectively. Our 12-monthly-target price is HK$5.16, equivalent to 15 /8x P/E in 2014/2015 respectively. We maintain the accumulate rating.

There was an accelerating callback in the passenger traffic in September

After the busy seasons in the summer, the growth rate of the RPK of Air China continues to decrease. The growth rate of passenger turnover volume in September was reduced to 5.2% on a yoy basis. The performance varied among routes. The domestic routes were not adversely affected by the high base of the same period as well as the flow control, with a yoy growth rate increasing to 3.1% and a mom decrease of 9.4%; Even with a relatively high base, the international routes maintained a relatively rapid growth, but the growth rate dropped, with a yoy increase of 8.6% and a mom decrease of 10%; the regional routes were almost the same as the international routes, up 11.6% yoy and down 11.4% mom.

The domestic routes capacity had the largest contraction amplitude

The growth rate of capacity also decreased. In September, the available seat kilometres increased by 7.7% yoy. Due to the repeated macro-economic recoveries, along with the control of the government consumptions, demands of the domestic passenger market remain weak. The company mainly controlled the in-put of domestic routes and there was a yoy growth of 4% in the domestic routes; other routes maintained a sharp growth trend. The international routes increased by 14% on a yoy basis, while the regional routes increased by 16.4%. These three all had a mom decrease of 8.7%, 2.7% and 5.1% respectively.

The passenger load factor continued to fall

The average P L/F in September is 79.4%, down 1.9ppts yoy, 2.7 ppts mom. Due to the implementation of controlled capacity, P L/F fallback is prevailing, and the domestic routes reported an 80.8% P L/F, the minimum fallback of all routes, down 0.7ppts yoy and 0.6 ppts mom respectively. P L/F of the international routes and regional routes decrease 3.9 and 3.1 ppts yoy because of excessive supply respectively, to 77.9% and 72.2%.

Freight business has strong performance

Driven by continuously increasing airfreight demands, Air China's freight business in September had strong performance, and its freight traffic rebound greatly 21.6% yoy and 16.3% mom. International routes, especially the continuously blooming North American route, are the main promotion factor. International routes in September accounted for as high as 74% of the total freight traffic. Domestic, international and regional routes` freight traffic grew by 0.2%, 30.6% and 31.1% yoy respectively, and by 11.25, 18.6% and -2.2% mom. In the first half year, the company introduced in B777F air freighters that had better fuel efficiency to replace the old B747F plane. Benefited from the effects of reducing costs and increasing demands, we predict that profitability improvement brought about by freight business rebounds will obviously show in its third-quarter's result that is to be released.

The first half year's result was better than that of peers

In the first half year, Air China's turnover achieved a yoy growth of 8.5% to RMB 49.932 billion. The total cost's yoy growth was 6.72%, net profit is RMB 0.51 billion, down by 55.4% yoy, corresponding earnings per share was RMB 4.15 cents, and that of the same period last year were respectively RMB 1.144 billion and RMB 9.31 cents. The dramatic fall of profit followed the first half year's RMB devaluation which led to 720 million Yuan's worth of net foreign exchange loss, while during the same time last year it was a net foreign exchange gain of RMB 1.12 billion Yuan. But because of the rebounded profit from Cathay, the investment gain risen by 45% to RMB 244.6 million Yuan yoy. In addition, due to the earlier arrival of government subsidy, other incomings have grew 55.8% yoy to RMB 2.42 billion Yuan. The latter two items have partly made up for the exchange losses. In terms of yield, the gain for each kilometer per customer has dropped by 2 cents to 0.58 Yuan, and domestic, international and regional routes have respectively dropped 1cent, 3 cents and 6 cents.

How we view this

In the coming two years, the company will have greater efforts to increase the transportation capacity, and it is scheduled to have a net increase of 22 airplanes, and is expected to increase the input of transportation capacity for remote routes of Europe and America, which is beneficial for sharing the fruit of the North America routes recovery. But the continuous flow diverting to high speed rails and the intensified industry competition will continue to challenge the improvement of demand-end profitability. On the other hand, the negative impact brought about by the cost-end fuel price and exchange rate factor is expected to diminish.

Click Here for PDF format...