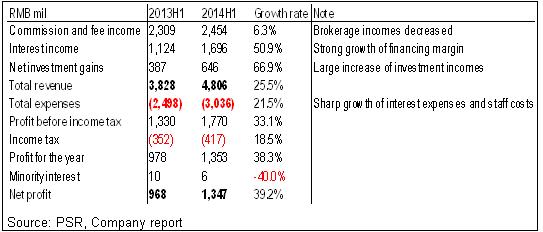

-According to 1H2014 results of China Galaxy Securities (hereinafter referred to as CGS or the Group), the Group¡¦s performance met our expectation. As at the end of June, commission and fee income increased by 6.28% y-y to RMB2.454 billion. Meanwhile, interest income and investment gains also increased largely during the same period. Total revenue grew 25.55% y-y to RMB4.796 billion;

-According to the businesses, brokerage business is still one of key competitive advantages of CGS. Securities brokerage net revenue ranked No.1 from 2008 to 2013. By the end of 1H2014, incomes of securities brokerage business reached to RMB3.073 billion, up 13.44% y-y. However, the growth of the commission fee continued to go down due to the fiercer competition, and we believe the market share of CGS will go down in future. On the other hand, due to the improvement of the market, margin financing and securities lending increased significantly in 2014, and CGS recorded RMB21.271 billion in such business during the period, up 81.3% y-y strongly. We believe its growth would increase over 100% in 2014;

-CGS also made great efforts to expand asset management business except traditionally brokerage business in 2014. Incomes of investment banking business grew obviously due to the re-opening of IPOs in A Shares. By the end of 1H2014, incomes of CGS¡¦s investment banking business amounted to RMB506 million, up 161.73% y-y largely. Asset management business and overseas business maintained strong growth, increased significantly by 22.39% and 78.57% y-y to RMB84 million and 100 million respectively. The performance of the Group¡¦s investment banking business is in line with our expectation;

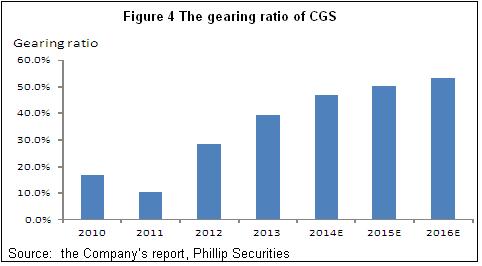

-CGS¡¦s assets maintained stable growth. As at the end of 1H2014, total assets achieved to RMB90.328 billion, up 15.39% compared with the end of 2013. Net assets increased by 4.44% to RMB26.294 billion. Meanwhile, current liabilities increased by 20.6% to RMB63.735 billion, which caused the gearing ratio to increase by 4.51ppts to 43.74%;

-The market environment in 2014 will be better than that of 2013, and CGS will maintain the competitive advantages in its brokerage business, and other businesses such as investment banking will also increase strongly, therefore we expect its profit growth would maintain at the stable level in future, and increase the profit estimation in the next two years. We are confident of the Group¡¦s performance in future and increase its 12-m target price to HK$7.2.

How we view this

CGS¡¦s performance increased stably, and the operating performance is better than expected. Although the income growth of traditional brokerage business slows down, it will improve after new businesses such as Shanghai-Hong Kong Stock Connect are implemented in future, and the activity of trading will increase obviously, we believe the Group¡¦s commission incomes will increase strongly, and considering the strong growth of businesses such as investment banking and wealth management, therefore profits will continue to increase largely.

We estimate CGS¡¦s net profit would increase by 20% y-y approximately in average in the next two years.

Investment Action

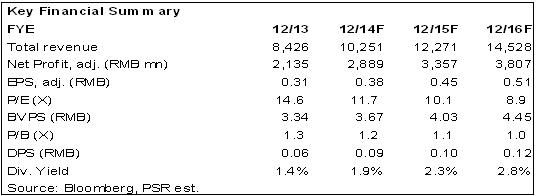

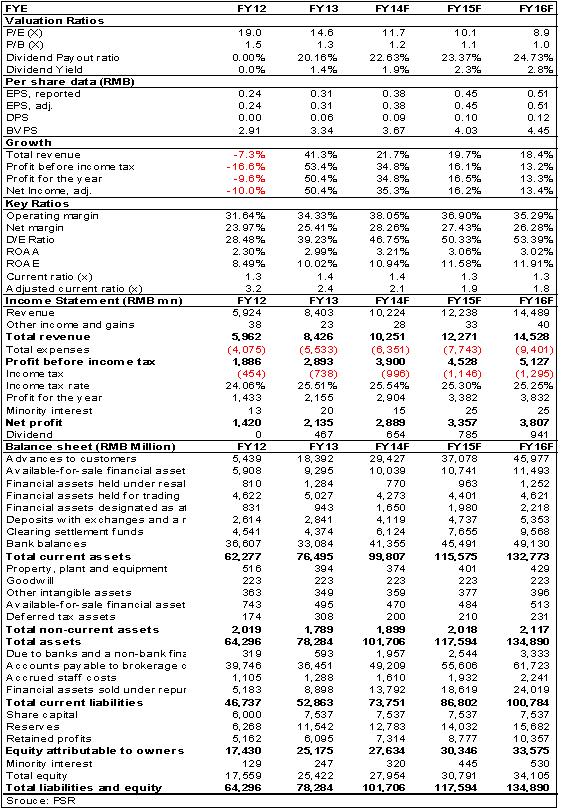

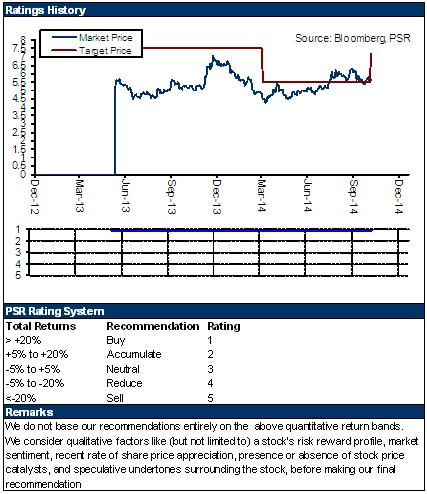

We believe the market environment in 2014 will be better, and CGS¡¦s incomes will increase obviously, and the profit growth will maintain at the stable level in future. Therefore we are confident of the Group¡¦s performance in future and increase its profit estimation in the next two years, and increase its 12-m target price to HK$7.2, 26.5% higher than the latest closing price, equivalent to 12.8xP/E and 1.4xP/B in 2015 respectively, the valuation is attractive, and recommend Buy rating.

Obvious advantages of the brokerage business

CGS is one of the largest brokers in China, and its securities brokerage net revenue ranked No.1 in recent years. CGS has the widest networks in the industry. By the end of 2013, the incomes of brokerage business amounted to RMB3.9 billion, with the market share of 5.14%. As at the end of June 2014, the Group has completed the establishment of 7 branch offices and 64 securities branches, and there were another 36 branches that were in the process of establishment.

During the period, CGS insisted on combining online and offline services, organizing and conducting new marketing services for clients through online channels such as payment by third parties and marketing through Baidu Search. The Group received the letter of approval from CSRC, and became the first batch of securities traders with qualification for doing internet securities business on a pilot basis in the industry. Meanwhile, the Group also increased the supplies of financing products. By the end of 1H2014, the sales of financial products amounted to RMB6.348 billion, up 68.7% y-y.

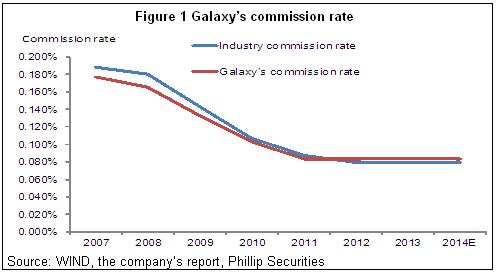

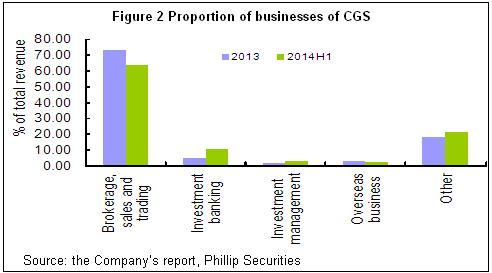

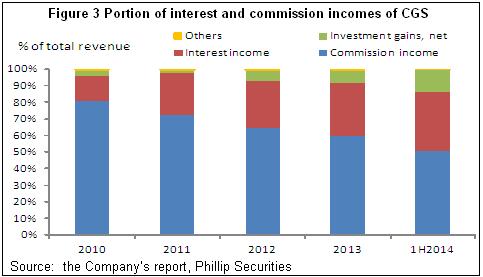

Due to obvious advantages of brokerage business, the proportion of incomes of such businesses was around 80% in recent years, much higher than the peers. However, the growth of the commission fee continued to go down due to the fiercer competition. By the end of June, incomes of securities brokerage business reached to RMB3.073 billion, up 13.44% y-y, around 64% of total revenue, mainly caused by the low level of commission rate, and we expect the proportion will go down continually in future.

CGS also made great efforts to expand asset management business except traditionally brokerage business in 2014. Incomes of investment banking business grew obviously due to the re-opening of IPOs in A Shares. By the end of 1H2014, incomes of CGS¡¦s investment banking business amounted to RMB506 million, up 161.73% y-y largely. Asset management business and overseas business maintained strong growth, increased significantly by 22.39% and 78.57% y-y to RMB84 million and 100 million respectively. The performance of the Group¡¦s investment banking business is in line with our expectation.

Strong growth of new businesses

Due to the improvement of the market, margin financing and securities lending also increased significantly in 2014, and as at the end of June, CGS recorded RMB21.271 billion in such business, up 81.3% y-y strongly. We believe its growth would increase over 100% in 2014;

According to the type of business, interest income increased largely due to the strong growth of margin financing, the proportion grew from 14.7% in 2010 to 31.6% in 2013. As at the end of June, the proportion of interest income to total revenue increased to 35.3%.We believe it will continue to go up in future.

Stable growth of asset scale

Due to the demand of the business development in recent years, CGS¡¦s capital pressure increased. Considering the increased demand of the capital, The Group was listed in H Shares in 2013, raising proceeds together with interest income amounting to HK$8.148 billion, equivalent to RMB6.498 billion.

CGS¡¦s assets maintained stable growth. As at the end of 1H2014, total assets achieved to RMB90.328 billion, up 15.39% compared with the end of 2013. Net assets increased by 4.44% to RMB26.294 billion. Meanwhile, current liabilities increased by 20.6% to RMB63.735 billion, which caused the gearing ratio to increase by 4.51ppts to 43.74%.

We expect the Group¡¦s gearing ratio will increase continually in future.

Risks

Decrease of fee and commission income;

Investment gains dropped significantly;

Share price declined sharply affected by the market environment.

Click Here for PDF format...