-Fortune reported 1H14 NPI of HK$ 581 mn, up 32.8% yoy, among that Fortune Kingswood, which was acquired in Oct 2013, accounted for 24.8% of the growth.

-DPU increased 16% yoy to HK$ 0.2088, amounted to 6.2% of yield. NAV per unit increased to HK$ 11.01.

-The occupancy rate was strategically remained high as 99.1%, with rental reversion of 21.2%. Passing rent edged up as HK$ 34.2 psf.

-The company was not worrying on the slipping retail environment due to its focus on necessity consumption.

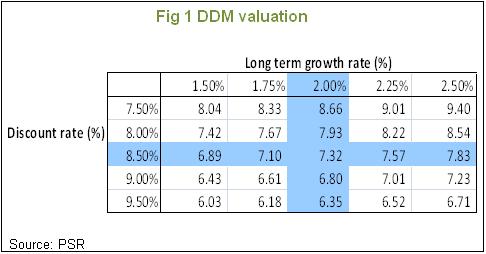

-Based on DDM valuation, we adjusted the target price to HK$ 7.32, maintain the rating as ¡§Accumulate¡¨.

Financial Highlights

In 1H14, Fortune reported total revenue of HK$ 813.5 mn, up 33.5% yoy with net property income of HK$ 581 mn, up 32.8% yoy. Only 8% was coming from the original portfolio, while 24.8% of growth was brought by the Fortune Kingswood acquired in Oct 2013. Distributable income reached HK$ 390.5 mn, rose 27.2% yoy. The dividend per unit was HK$ 0.2088, grew 16% yoy, which amounted to 6.2% of yield. NAV per unit increased 9.9% yoy to HK$ 11.01.

How we view this

Fortune obtained good result when compared to last year. However, the growth quickly slowed down in the 2Q. This was mainly due to that the 1Q growth was driven by Fortune Kingswood acquired last year, while no more acquisition was made in this year. The management reiterated they were always considering potential M&A but needed to coordinate with the parent company. The passing rent edged up to HK$ 34.2 psf from HK$ 33.9 psf in 1Q, which still has upside room, when compared to other HK property REITs.

Investment Action

We believed the final DPU would be at least the same as the interim payout, which in total would be HK$ 0.418 for FY14, increased 16% yoy compared to FY2013 and 4.7% higher than our previous estimate. Actually, according to Fortune¡¦s historical payouts, we are quite confident that it can achieve a long term dividend growth of 2%. In spite of the recent slump 10-yr US treasury yield, we adopt a conservative discount rate of 8.5%, based on the potential interest rate hike. We maintain the rating of ¡§Accumulate¡¨ to Fortune REIT with target price HK$ 7.32, based on DDM valuation.

Key takeaways from the management:

1. How the weak retail sales, esp decrease on the consumption of Individual Visit Scheme affect the Fortune¡¦s rental business

The decline on retail sales figures had not yet shown influence on company¡¦s rental business. Clients were still keen on the rental renewal. The management indicated that it was the luxury segment most affected by the weakened sales volume, while Fortune primarily focused on the necessity consumption, such as supermarkets and F&B. According to company¡¦s data, over 60% of the rentable area and rental income was coming from services & education, F&B and supermarkets.

The occupancy rate was 99.1% in 1H14. The management explained that they were trying to keep this rate high due to the renovation in Belvedere Square commenced in the 2H of 2014 would drag down the overall occupancy rate.

2. The influence on US interest rate hike to Fortune¡¦s borrowing cost and asset valuation

As at June 30, 55% of the total debt exposure was hedged. The effective interest cost reduced sharply from 2.81% in 1H13 to 2.2%. Although the gearing ratio increased from 20.9% in 1H13 to 31.1%, the management was feeling comfortable on it. From company¡¦s data, there are no refinancing needs until 2016.

The company did not deny on the potential pull back on asset valuation after the rise in interest rate. We expected that may happen in 2015 or 2016, which the overall property price in HK will drop, thus lower the NAV per unit for the company. However, the management indicated that the company is not going to sell out the assets for cash, while investors holding Fortune are aimed for stable dividend. Since the property price may not directly link to the rental income, thus the distributable income, this is not a major concern for investors.

Valuation

We assume the final DPU to be the same as the interim payout, which in total would be HK$ 0.418 for FY14. The DDM valuation is based on discount rate of 8.5% and long term growth rate of 2%. We thus maintain the rating of ¡§Accumulate¡¨ to Fortune REIT with target price HK$ 7.32.

Potential Risks

Faster than expected interest rate surging pushes up Hibor.

Click Here for PDF format...