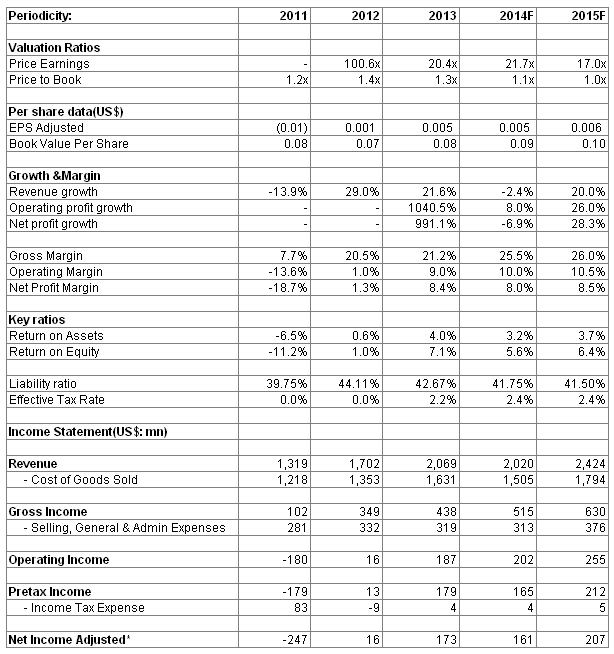

-According to the semi-annual report of 2014 of SMIC, its revenue has reached 962 million US$ (same as below), decreasing 7.72% year on year. Net profit attributable to shareholders is 77.06 million, decreasing 66.43% year on year. Among which the revenue of 2Q14 is 511 million, decreasing 5.53% year on year, but increasing 13.36% quarter on quarter. Net profit attributable to the shareholders is 56.8 million, decreasing 24.67% year on year, but increasing 180.35% quarter on quarter.

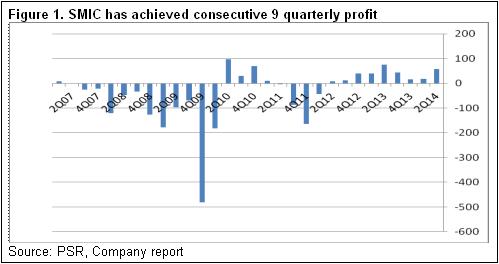

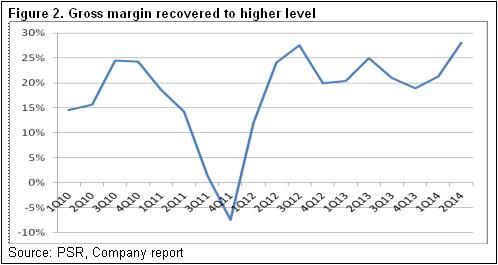

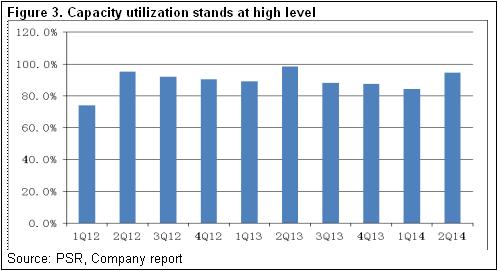

-After excluding Wuhan Xinxin, the revenue of the second quarter even creates a new high and is profitable for successively nine quarters. The gross profit margin of 27.98% for a single quarter also reaches the top since 2005, increasing 6.7 percentage points comparing with that of the last quarter. Generally speaking, the increase in its revenue is mainly due to the raise in the capacity utilization, which increased from 84.2% of the first quarter to 94.6% of the second quarter. Besides benefiting from the capacity utilization, improvements in product structure, operation efficiency and cost control are also contributable to the increase of profitability.

-In early July, Qualcomm of America and SMIC announced jointly that they would cooperate with each other concerning 28nm wafer production. Qualcomm is the market leader of global mobile communication field. Snapdragon processor is its core product, being wildly used by manufacturers of smart phone. Now it is mainly delivered to TSMC, the leading company of wafer foundry services. Through cooperation, we anticipate to strengthen the strategic relationship of both sides and improve the maturity of the production line of 28NM processing of SMIC. Considering its lower production cost than TSMC and the industry chain of smart phone transferring to the mainland, the production of 28NM processing may rapidly increase at that time so as to further promote the profitability of the company.

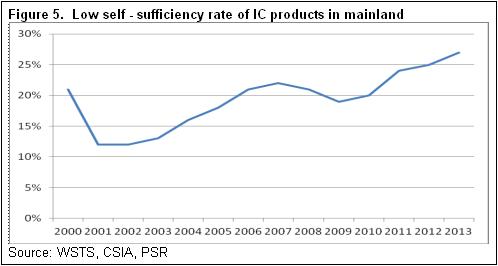

-Chip localization has a great potential to improve. In 2012, the imported chip from China accounted for 56% of the total global demand, while its self-sufficiency rate was only 11%. Mainland corporations like Huahong Grace are capability-limited with backward craftsmanship. Thus, SMIC is expected to win more market shares during this round of the rapid rising course of the domestic integrated circuit industry. Moreover, the government will hopefully give more support to integrated circuit industry like the national integrated circuit industry supporting fund. From this trend, domestic integrated circuit industry will hopefully enter a new round of development phase. As a leader in the manufacturing link in the sector, SMIC is expected to benefit obviously from this process.

Investment Action

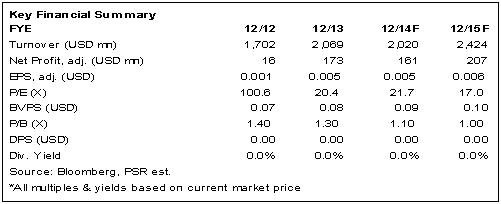

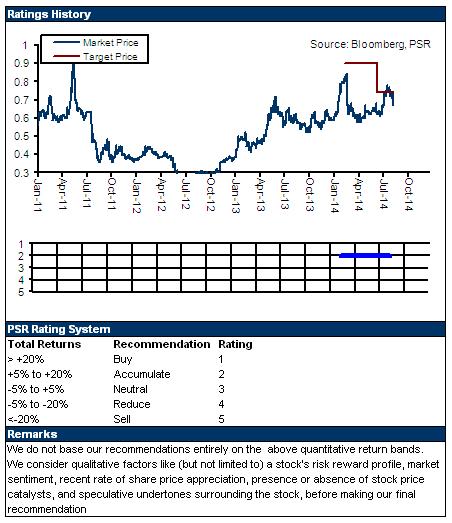

The company's long-, medium- and short-term strategies are all going smoothly. More advanced workmanship will usher in the medium- and long-term growths. The broader market of the mainland and booming communications industry will still sustain the medium- and short-term growths. In addition, the industry is booming and there may be some supporting policies. Therefore, as the biggest leading company of wafer foundry services with the most advanced technology in mainland, the company is expected to be benefited continuously and enter a new profitable channel constantly. We fix the company stock's target price at HK$ 1 with 1.35X 2015BVPS. We upgrade it ¡§Buy¡¨ rating.

Being profitable for successively nine quarters

According to the semi-annual report of 2014 of SMI, its revenue for the first half year has reached 962 million, decreasing 7.72% year on year. Net profit attributable to shareholders is 77.06 million, decreasing 66.43% year on year. Among which the revenue of the second quarter is 511 million, decreasing 5.53% year on year, but increasing 13.36% quarter on quarter. Net profit attributable to the shareholders is 56.8 million, decreasing 24.67% year on year, but increasing 180.35% quarter on quarter. However, after excluding Wuhan Xinxin, the revenue of the second quarter has even created a new high and is profitable for successively nine quarters. The gross profit margin of 27.98% for a single quarter also reaches the top since 2005, increasing 6.7 percentage points comparing with that of the last quarter.

Overall speaking, the increase in its revenue is mainly due to the raise in the capacity utilization. The utilization of the second quarter has increased to 94.6% from 84.2% of the first quarter. The shipment quantity has also increased 11.5% comparing with that of the last quarter. Besides benefiting from the capacity utilization, improvements in product structure, operation efficiency and cost control are also contributable to the increase of profitability.

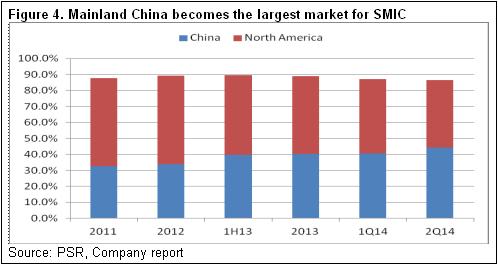

It is worth mentioning that the increase of mainland clients is one of the main contributors to the performance. The proportion of the mainland clients of the company has increased to 44.4%, surpassing the other regions for the first time and becoming the largest region. We believe that the emerging of IC design in the mainland will become an important driving force for the growth of the company. As the largest chip manufacturer in the mainland, the company enjoys local advantages as well. In the future, the company will hopefully benefit from the rising of domestic IC industry chain continuously.

The product structure may constantly be improved

Although the strategy is shifted from technology-oriented to product-oriented, the improvement of product structure still maintains one of the main motivations for the growing of the performance of the company. In the first half year, the proportion of 40nm has increased. In the second quarter, its proportion has increased to 13.2%, higher than 12% of the whole year of 2013 and 9.8% of the first quarter of this year. We expect that at the end of the year, the proportion may increase to about 18%.

Besides, the 28NM processing is believed to be produced massively at the end of the year or at the beginning of next year. In early 2014, the company became the first foundry providing 28NM processing chip in the mainland. In early July, Qualcomm of America and SMIC announced jointly that they would cooperate with each other concerning 28nm wafer production. SMIC will manufacture Snapdragon processor exclusively designed for mobile terminal for Qualcomm in mainland. According to the management of SMIC, the relevant income may be recorded at the beginning of 2015.

Qualcomm is the market leader of global mobile communication field. It has strong technical reserve in CDMA and LTE 4G. In the first quarter of 2014, its global base band market share has reached 66%, far more than 15% of the No.2 Media Tek. Snapdragon processor is its core product, being wildly used by manufacturers of smart phone. Now it is mainly delivered to TSMC, the leading company of wafer foundry services. Through cooperation, we anticipate to strengthen the strategic relationship of both sides and improve the maturity of the production line of 28NM processing of SMIC. Considering its lower production cost than TSMC and the industry chain of smart phone transferring to the mainland, the production of 28NM processing may rapidly increase at that time so as to further promote the profitability of the company.

Benefit from import substitution and supporting policies

The proportion of sales volume of the down-stream products of domestic integrated circuit has reached 33%, becoming the largest market in the world. However, the self-sufficiency rate of domestic integrated circuit is only 27%. Among which the chip localization has more potential to grow. In 2012, the imported chip of China accounted for 56% of the total global demand, but the self-sufficiency rate was only 11%.

It is worth mentioning that mainland corporations like Huahong Grace are capability-limited with backward craftsmanship. Thus, SMIC is expected to win more market shares during this round of the rapid rising course of the domestic integrated circuit industry.

Moreover, for the rising of Chinese integrated circuit industry, manufacture is the key. But this field is often depending on great investment, so policy supporting is essential. Considering the previous prism gate affair and national information security, we hold that in the future the government will hopefully launch more supporting policies for integrated circuit industry. It is reported that the general development guidelines of integrated circuit are going to be issued. The Ministry of Telecommunications takes the lead to design the supporting fund scenario for national integrated circuit industry. It is said that the amount of the first supporting fund of this year will increase to RMB130-150 billion from previous plan of 100-120 billion. From this trend, domestic integrated circuit industry will hopefully enter a new developing phase. As the leader in manufacture link, SMIC is expected to obviously benefit from this process.

Catalyst

Launch of the industrial supporting policies;

Mass production of advanced technology in advance.

Risks

Severer competition among the industry;

Depreciation increase affecting the improvement of profitability.

Click Here for PDF format...