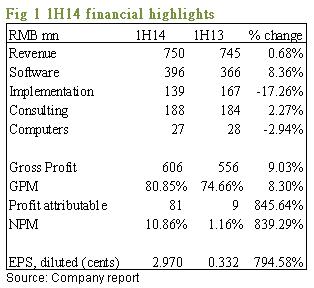

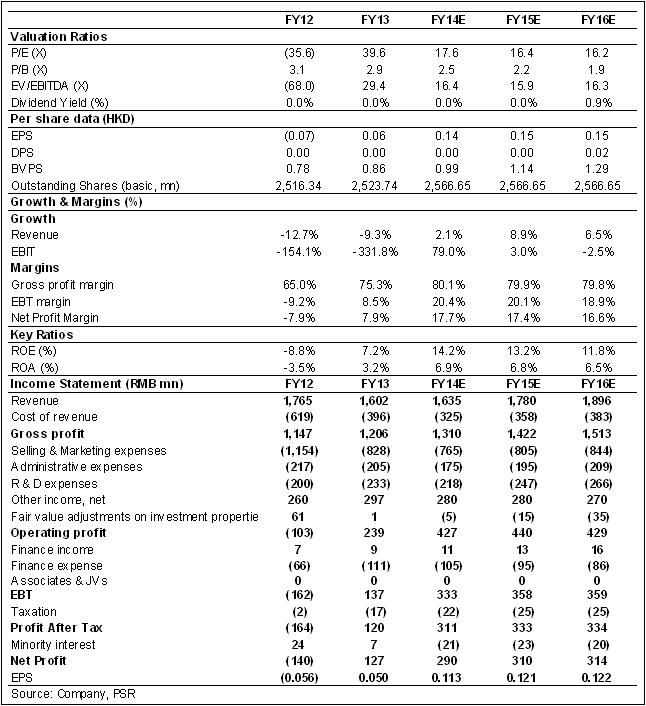

-Kingdee's 1H14 total revenue was slightly up 0.7% while gross profit rose 9% yoy. GPM increased from 74.7% last year to 80.9%. With sharply reduced operating expenses, profit attributable to stakeholders surged 846% yoy. Diluted EPS soared to RMB 2.97 cents.

-Revenue from cloud business surged 124% yoy, accounted for 5.4% of the total revenue.

-After further shifting the business to indirect sales channel, both the cost and expenses recorded significant drop yoy as well as to percentage to revenue.

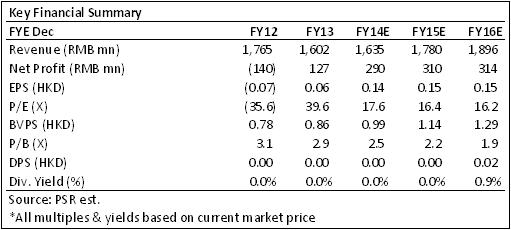

-We upgrade Kingdee's rating to ¡§BUY¡¨ with target price HK$ 3.05, equivalent to 19.3x/18x of 2014 and 2015 forecasted EPS, plus HK$ 0.35 net cash per share.

Financial Highlights

Kingdee announced its encouraging 1H14 result. Total revenue just slightly up 0.7% yoy to RMB 750 mn while gross profit up 9% yoy to RMB 606 mn. GPM was 80.9%, increased from 74.7% last year. Profit attributable to stakeholders surged 846% yoy to RMB 81.5 mn (2013: RMB 8.6 mn), meaning that the operating expenses had sharply reduced. Diluted EPS soared to RMB 2.97 cents (2013: RMB 0.332 cents).

How we view this

Mentioned in the last report, Kingdee obtained stable growth during these years but the cost and expenses were out of control. After further shifting its software sales business to indirect sales channel, it was able to reduce the cost, by cutting unnecessary headcount or administration expenses, thus improved both the GPM and NPM. We expect this will still be the case in the next few years, which the proportion of indirect sales revenue to total will continue to increase.

Investment Action

According to IDC, Kingdee was the largest application software provider for SMEs in mainland China, in 10 consecutive years. The good reputation will help in capturing SMEs` cloud business. Meanwhile, the PRC government is now promoting local software and servers, we believe more and more large company will turn to collaborate with Kingdee in enterprise software.

We upgrade Kingdee's rating to ¡§BUY¡¨ with target price HK$ 3.05, equivalent to 19.3x/18x of 2014 and 2015 forecasted EPS, plus HK$ 0.35 net cash per share.

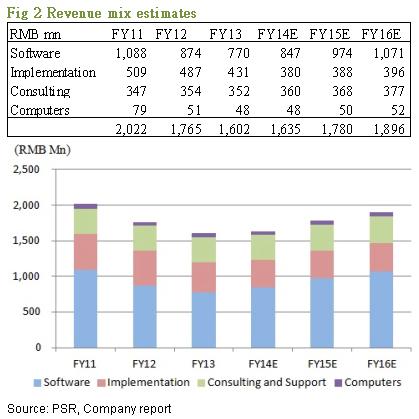

Revenue growth flat, software still the major source of income

The revenue growth of Kingdee missed our estimates, especially for solution implementation, which suffered -17% of negative growth. We thus cut the forecasted 2014 implementation revenue down 23% to RMB 380 mn, in believing the down trend to continue and slightly adjusted down 2.6% of the software revenue. Both 2015 and 2016 estimates have downward amendments.

According to the company financial report, the SME ERP business obtained stable growth, which revenue from KIS software grew 29.6% yoy. However, for the LME business, EAS's revenue dropped 10.5% yoy that pullback the total growth on software section.

On the other hand, revenue from newly developed cloud business surged 124% yoy, accounted for 5.4% of total revenue, which the K/3 Cloud obtained nearly 3 times yearly growth. We believed instead of one time software sales revenue, the cloud business may be able to generate future revenue series from administration services or maintenance fee.

Cost reduced, brought the company sharp increase in profit

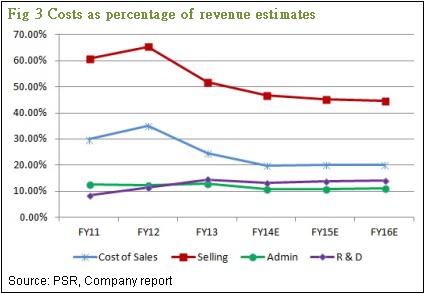

In 1H14, cost of sales decreased 24% yoy to RMB 144 mn that pushed up the GPM for 6.2 percentage points to 80.9%. At the same time, selling, administration and R&D expenses all reduced 12%, 14% and 11% on yoy respectively.

Actually, the ever increasing cost and expense had been a major challenge of Kingdee in these years. The company started to shift the software distribution channel from direct sales to indirect last year, which showed the effectiveness to cost control. In 1H14 it had further shifted to indirect sales channel, which sharply reduced the cost, by cutting unnecessary headcount or administration expenses, and thus improved both the GPM and NPM. We expect this will still be the case in the next few years, which the proportion of indirect sales revenue to total will continue to increase.

Valuation

According to IDC, Kingdee was the largest application software provider for SMEs in mainland China, for 10 consecutive years. We believe the good reputation on ERP software launching will help the company to capture SMEs` attention also in the newly developed cloud business. Meanwhile, although there was revenue drop on the LME service, with the state policy to promote local software and servers, we believe more and more large company will try on using Kingdee's service due to its goodwill on SME market.

Potential Risks

The growth on cloud business slows down;

Cost and expenses rebound.

Click Here for PDF format...