-The Group released its performance in the first half of the year 2014. In 2014, the Group realized a turnover of HK$ 373 million, up by 68.68% year on year. The gross margins stood at HK$235 million with the gross margin rate reaching 62.9%, or 0.9 percentage points higher than the same period of last year. Profits attributable to shareholders were HK$179 million, growing by 99.8% year on year. EPS was HK$0.13 and mid-term dividends would not be distributed. The H1 performance was a little bit higher than expected, mainly because the Group finalized two large acquisitions in the first half of the year 2014.

-In the first half of the year 2014, the Group realized HK$177 million revenues from operations & service of sewage treatment, growing by 44.7% year on year. The scale of sewage treatment in the first half of this year reached 475,000 cubic meters, increasing by 110,000 cubic meters from the end of 2013.

-In The first half of the year 2014, the Group realized HK$96 million of revenues from its sludge business. As a new business of the Group, the sludge business, within half a year, has become the second largest business of the Group only after the sewage treatment. At present, the Group has 693,000-ton sludge treatment capacity.

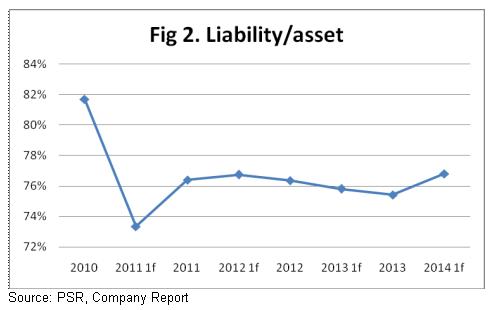

-We believe the Group has sufficient fund to carry out or purchase new projects. At present, the Group has HK$246 million in cash. When its debt ratio reached 65% of that at the end of 2012, the Group can still obtain HK550 million of loans.

Profits increased slightly in 1H2014

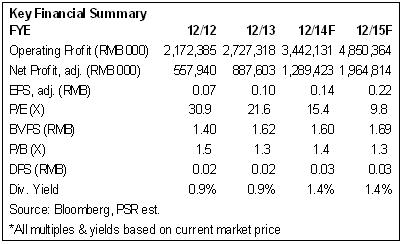

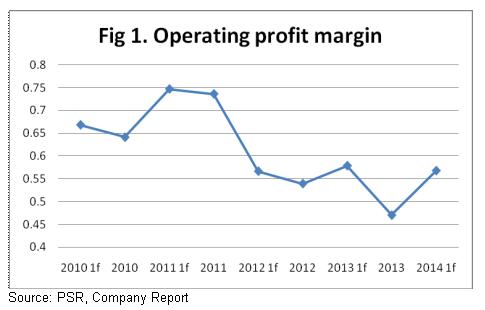

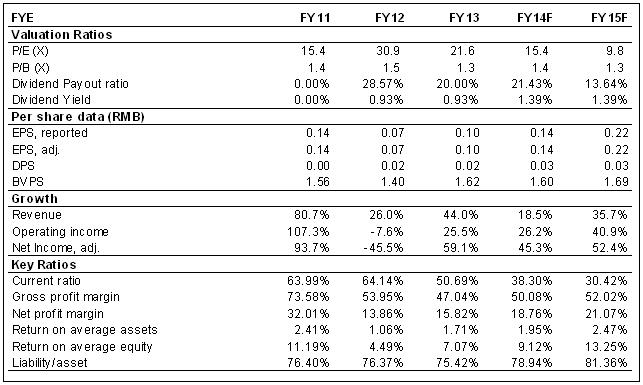

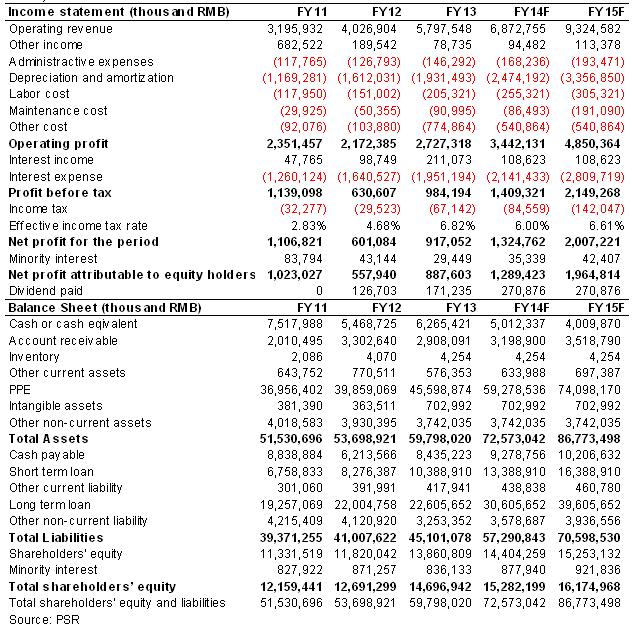

The Company's revenue amounted to RMB2.996 billion, up 2.4% y-y, and net profit attributable to equity shareholders was RMB686 million, increased slightly by 2.9% y-y, with the EPS of RMB0.076, slower than our expectation. The Company's wind power generation decreased slightly compared with the same period of last year due to the poor wind condition, but still recorded good returns because of the improvement of cost control and the increase of electrovalence.

Installed capacity will increase in 2H

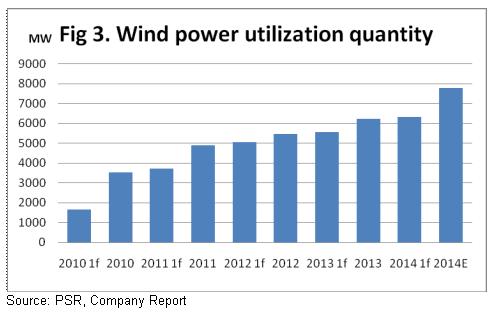

As at the end of 1H, the Company's total installed capacity of wind power plants reached to 6,320MW, up 99MW compared with the end of 2013, the newly added capacity was all in Yunnan Province, and the capacity of solar power plants recorded 400MW, increased by 70MW during the same period. Currently, the Company has projects of 2GW under construction, which would be put into operation in Oct, and the wind power capacity would reach to 8GW by the end of 2014, moreover, the Company is trying to expand new projects in areas where have no strict policies for abandoning wind power and power brownouts in recent years, therefore new projects will improve the Company's performance effectively.

The efficiency of power generation decreased

The utilization hours of the Company's wind power projects recorded 960 hours in 1H, declined largely compared with 1,096 hours in 1H2013, and according to areas, the largest decrease were in Shaanxi, Liaoning, Guizhou, and Shanxi, all dropped over 20%. The main reason was the poor wind condition in 1H, in fact, the situation of power grid transmission has improved obviously compared with the past, and the abandon rate of wind power decreased largely. We expect the utilization hours will increase in 2H, and maintain over 2,000 hours in the whole year.

On-grid tariff trends to go down

The cost of wind power projects is going down gradually due to the decrease of the price of wind turbine and the improvement of abandoning wind power and power brownouts. National Development and Reform Commission (NDRC) currently plans to decrease on-grid tariff of wind power, which would cut RMB0.02 - 0.04/kWh in different areas. The tariff trends to go down although the final plan has not been decided yet, therefore the profitability of wind power projects will decline in future.

Risks

No improvement of wind condition in 2HDelay of new projects

Valuation

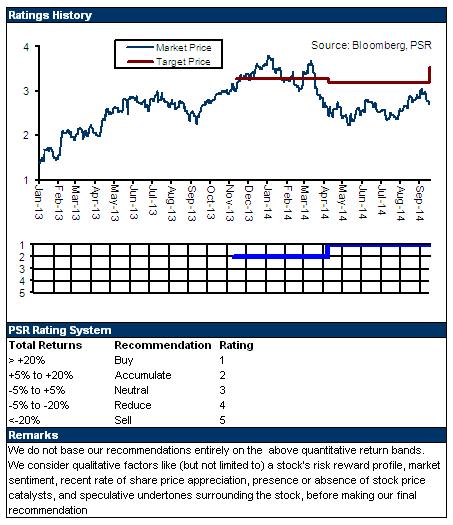

Although the Company's performance is lower than our expectation because of the issues of wind condition in 1H, it would be supported by the large scale of new projects in operation in 2H and the development of power grid environment. On-grid tariff trends to decrease, but it may be implemented after 2015, the Company's performance will not be affected in the next two years, we increase the Company's 12-month target price to HK3.54, equivalent to 13xP/E2015E, which is `Buy` rating.

Click Here for PDF format...