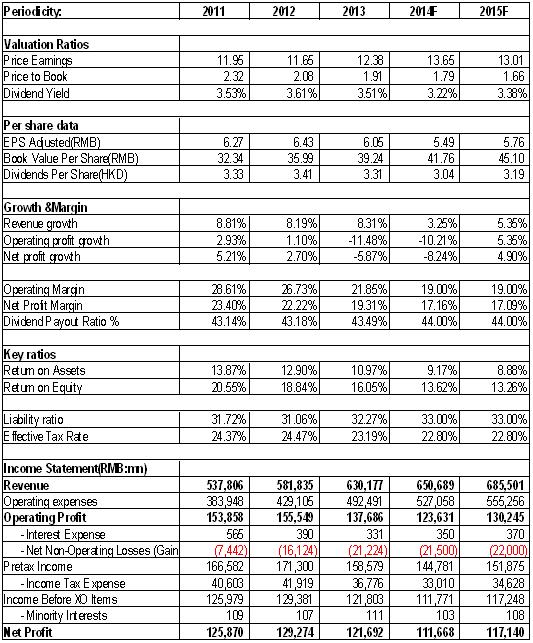

-According to the latest interim report of CM, it has realized operation revenue of 324.7 billion RMB (similarly hereinafter) in 1H14, a 7.1% increase on a year-on-year basis, while its net profit is 57.7 billion yuan decreased by 8.5%. Since this June, the reform of transformation from business tax to VAT has begun in telecommunication industry. And this is the main reason for the slow-down of revenue increase of CM. Therefore, it has seen a continuous slide of four seasons in the performance.

-However, on account of the adjustment of inter-network settlement costs, capital expenditure of speeding up 4G network establishment, etc. in the first half year, the performance of their financial statement is better than our expectation. Moreover, the company¡¦s revenue structure has been constantly optimized. The proportion of data services accounting for whole communication service income has increased to 40.9%.

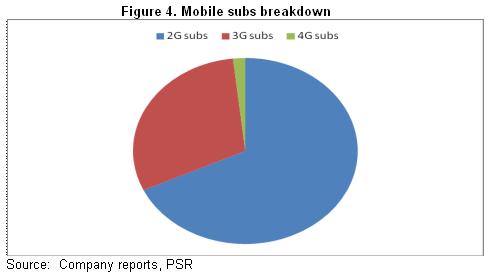

-The company may be the biggest beneficiary of 4G, the conservative estimate of the number of newly increased 4G users in the whole year may be more than 50 million. It has established the biggest 4G network in the world. Furthermore, the company has the largest proportion¡X68%¡Xof 2G user, which surpassed 52% of China Unicom and 40% of China Telecom. This also shows the biggest potential for their 4G upgrade. Besides, there is sufficient supply of TD-LTE 4G smart phones. We believe that the number of 4G newly increased users may surge in the second half year.

-4G network is expected to promote the flow operation strategy of the company, amd we don`t exclude that the turning point of ARPU will appear in one year or two years. In the first half year, ARPU has decreased 2.6% to 63.5 yuan on a year-on-year basis. However, data ARPU has risen markedly 19% to 26 yuan. With the increase of data ARPU, it is expected to offset the decrease of voice ARPU in the future. The increase of flow income will be the main driving force of income rise.

-Expense control is relatively a positive factor in that this will relieve the pressure of transformation from business tax to VAT. Meanwhile, we think its negative impact to 4G expansion is limited, because subsidy cut is relative, and it still supports 4G. Besides, there are nearly 150 kinds of 4G smart phones available with the price below a thousand yuan. Therefore, the universal low price is expected to reduce the customers` sensitivity of subsidy cut.

Investment Action

In general, with the outside competition such as the license granting of virtual network operators and fast growth of WeChat and other OTTs, and the inner pressure from the tariff adjustment of operators, the operators are facing increasingly great market pressure. However, with the help of prior-launch advantage, completed infrastructure of 4G network and improved 4G user experience, the company may be the biggest beneficiary of 4G.

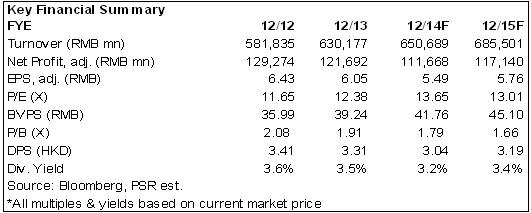

In the 3G age, China Unicom enjoyed at least 20X PE for its leading position. Entering into 4G age, China mobile may take more competitive status, we grant it a corresponding 15-time valuation level for earnings per share in 2014, with the target price of HK$103.75 and ¡§Accumulate¡¨ rating.

Performance slide in 1H14 less than our expectation

According to the latest interim report of CM, it has realized operation revenue of 324.7 billion yuan in 1H14, a 7.1% increase on a year-on-year basis, while its net profit is 57.7 billion yuan decreased by 8.5%. In the second quarter, the operation revenue is 169.9 billion yuan and the net profit is 32.5 billion yuan, a 6.5% increase and a 7.8% decrease YoY respectively. Compared with 6.9% in 1Q14, the service revenue only increase 2.6% YoY in 2Q14, which is attributable to the reform of transformation from business tax to VAT since June. Therefore, it has seen a continuous slide of four seasons in the performance.

However, on account of the adjustment of inter-network settlement costs, capital expenditure of speeding up 4G network establishment in the first half year, etc., the performance of the financial statement is better than our expectation. It is worth mentioning that although there is just single-digit growth in the operation revenue, it has surpassed the 3.6% of China Unicom in the same period.

Besides, the revenue structure of the company still keeps optimizing. In the first half year, the communication service income has realized 292.7 billion yuan, among which data services surged 27.8% YoY to 121.3 billion yuan. And its proportion in the communication service has also risen to 40.9%. Also, WIFI business of the company has reached an income of 72 billion yuan, and jumped 51.8% on a year-on-year basis, showing that the company is benefitting from 4G business.

4G contribution will speed up

After gaining TD LTE license in the last December, CM has launched 4G business service in advance. Up to the end of June, the number of their 4G users has reached 13.94 million. And the number is still growing every month. According to the latest data, the company has 6.5 million newly added 4G users in July, a 11.5% increase higher than 5.83 million of June. This shows that the 4G transfer is speeding up.

We predict that the company may be the biggest beneficiary of 4G, and the conservative estimate of the number of newly increased 4G users in the whole year may be more than 50 million. The company has established the biggest 4G network in the world. Up to the end of June, they have built up 410 thousand 4G base stations covering more than 300 cities, accomplishing 80% of their goal with an obvious improvement in network speed. Moreover, user experience is believed to improve most. Up to the end of June, the company has the largest proportion¡X68%¡Xof 2G user, which surpassed 52% of China Unicom and 40% of China Telecom. This also shows the biggest potential for their 4G upgrade. Moreover, the supply of TD-LTE 4G smart phone is sufficient with nearly 250 kinds, and there are nearly 150 kinds of 4G smart phones with the price below 1000 yuan. Meanwhile, there will be flagship phone available in the second half year to meet the needs of different classes. Plus with expectable tariff adjustment measures, we believe that the number of newly increased 4G users will increase more in the second half year.

Besides, 4G network is expected to promote the flow operation strategy of the company, so we don`t exclude that the turning point of ARPU will appear in one year or two years. In recent years, ARPU of the company has slid constantly. In the first half year of 2014, it has decreased 2.6% to 63.5 yuan on a year-on-year basis, and the decrease of voice ARPU is the main cause. It has decreased 11.8% to 35.3 yuan. However, data ARPU has risen markedly 19% to 26 yuan. With the increase of data ARPU in future, it is expected to offset the decrease of voice ARPU. It is worth mentioning that the mobile data flow has maintained the surge of 91.4% on a year-on-year basis in the first half year. In the future, based on the optimizing network, this trend is believed to be continued, and the increase of flow income will be the main driving force of income rise.

Positive impact on performance by expense control

CM has clearly noted that there will be a strict marketing expense control in 2014-2016. Under this guidance, the company¡¦s marketing expense will decrease 20 billion yuan in 2014, among which 5 billion yuan is terminal subsidy. Specifically, it means to directly benefit customers in package tariff from phone subsidy and payment with given fee. The predicted phone subsidy is only 21 billion yuan in 2014, far less than the 34 billion yuan of last year.

We consider that expense control is relatively a positive factor, because it will relieve the pressure of the reform of transformation from business tax to VAT. As for the negative impact for 4G expansion worried by the market, we believe it is limited. Because subsidy cut is relative, it controls 2G, 3G but still supports 4G. Besides, there are nearly 150 kinds of 4G smart phones available with the price below 1000 yuan. Therefore, the universal low price may reduce the customers` sensitivity of subsidy cuts.

Catalyst

Number of newly increased 4G users exceeds our expectation;

ARPU improvement.

Risks

Fiercer 4G market competition;

Performance slide exceeds our expectation.

Click Here for PDF format...