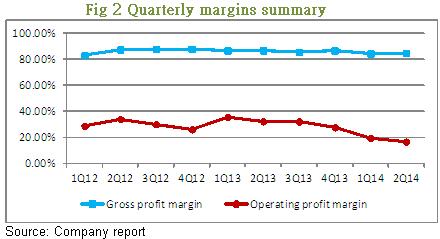

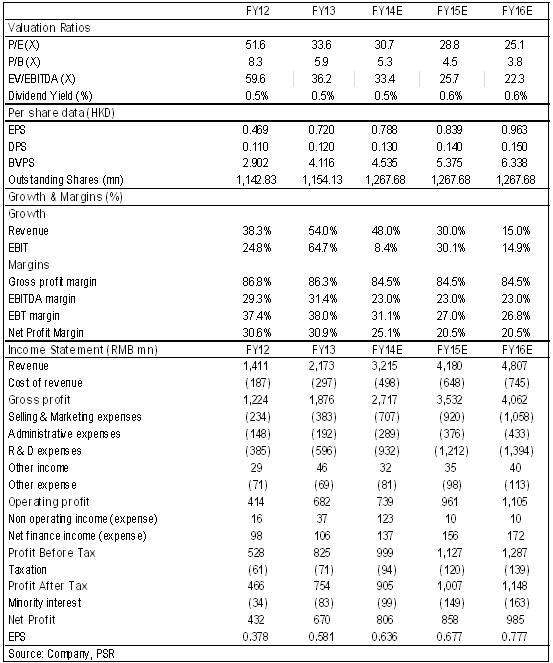

-Kingsoft¡¦s 2Q14 revenue resumed growth that increased 51% yoy and 11% qoq. Gross profit rose 47% yoy but operating profit dropped 22.3% yoy.

-Operating profit margin further dropped to the new low 16.5%, indicated continuous increase in cost and expenses. Without the gain on disposal in the last quarter, profit attributable to parent slumped 52% qoq.

-The company will focus on the mobile business in the near future, including mobile games, Android WPS mobile office, enterprise WPS and Kingsoft cloud.

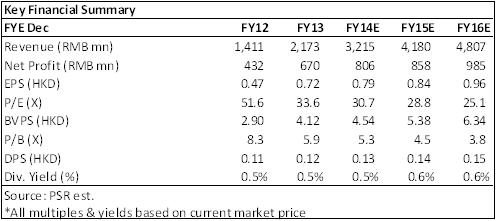

-We maintain the rating of Kingsoft as ¡§Neutral¡¨ with slightly upgraded target price HK$ 23.17 to reflect increased cash in hand.

Financial Highlights

Kingsoft announced its 2Q14 results yesterday with total revenue increased 51% yoy and 11% qoq to RMB 750.5 millions. Although the gross profit increased 47% yoy to RMB 634 millions, the gross profit margin dropped 2.2 percentage points to 84.5% compared to last year. Operating profit amounted to RMB 124 millions, decreased 22.3% yoy and 4.8% qoq due to continuously increases in R&D and selling expenses, with EBIT margin further dropped to 16.5% from 19.25% in 1Q, as the lowest in these years. Profit attributable to parent amounted to RMB 118 millions, sharply slumped 18.7% yoy and 52% qoq since the missing of the gain on disposal of investment last quarter.

How we view this

The result figures are quite unfavorable that although the revenue is still on growth, cost and expenses soar at a higher speed which sharply lowers the margins. Management explains that 2014 is a year of investment and development, so that they do expect the margins to drop, around 10% to 20% due to heavy R&D and promotion expenses on mobile business. They believe the contribution now will play out in the future and they tend to focus on several areas including the Cheetah mobile, mobile games, mobile WPS office applications faced to enterprises and the Kingsoft cloud.

Investment Action

The revenue in 2Q resumed growth and we therefore adjusted upward the estimates in all the three areas. However, profit margin was harmed by the further increasing cost and expenses and EPS is expected to be lowered. Although the management is keen on developing the mobile business and confident about the potential growth, we are looking forward to see any actual figure coming out in the future. Thus, we maintain our rating of Kingsoft as ¡§Neutral¡¨ with slightly upgraded target price to HK$ 23.17 to reflect increased cash in hand, equivalent to 29.4x/27.6x of 2014 and 2015 forecasted EPS.

Revenue on growth but cost and expenses rise at a higher speed

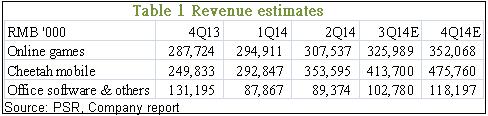

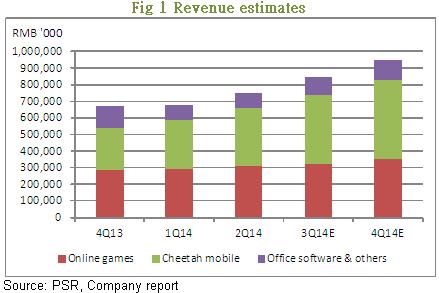

The 2Q14 revenue from online games obtained stable growth of 13.7% yoy and 4.3% qoq, mainly come from the flagship game JX Online III, which accounted for 54% of the online game revenue in the first half. Revenue from Cheetah mobile recorded growth of 145.7% yoy and 20.7% qoq, and the office software business resumed growth as expected of 8.9% yoy and 1.7% qoq.

We expect the quarterly growth on online games will speed up in 3Q & 4Q since there are 4 mobile games which will progress to beta testing in the 3Q, for a total of 12 games in pipeline. The growth in Cheetah mobile is expected to continue at a diminishing rate, while the revenue from WPS is forecasted to bottom up. The management has mentioned about the new round of 3-year government software purchase starts in 2Q and they are confident to grab a bigger slice than ever.

However, the cost and expenses also go up, at a higher speed. Cost rose 76% yoy and 9.1% qoq, while R&D and selling & distribution expenses rose 63.5% and 131.6% yearly, lead to a significant drop on the operating profit margin.

The future focus

Management explains the heavy R&D expense is due to the increase in headcount. They have specially recruited professionals and talents from large companies such as Microsoft, to join the mobile development team. In the near future, Kingsoft will focus in several areas:

1.Online game is still a main revenue contributor. The management forecasts the annual growth on revenue from JX Online will be 16% to 17% in 2014.

2.There are 12 mobile games under development which 4 of them will have close beta testing in the 3Q. The company will actively collaborate with Tencent and Xiaomi in the launching and distribution of its games.

3.The company has launched the WPS mobile office in Android OS, while the WPS will be developed to face more to the enterprise market.

4.The Kingsoft cloud is still at the investment stage but it will be a future storage and entertainment platform.

Valuation

We have adjusted upward the 2014 revenue forecasts as well as the cost and expenses. It turns out to have a lower EPS. However, we agree with the management that the investment and development is necessary in transforming its business model towards the mobile based. Thus, compared to 1Q, we tend to give a higher valuation on its business as HK$ 16.55, which equals to 21x of its 2014 forecasted EPS and net cash in hand of HK$ 6.62.

Potential Risks

Growth on mobile business does not meet expectation;

Cost and expenses continue to increase.

Click Here for PDF format...