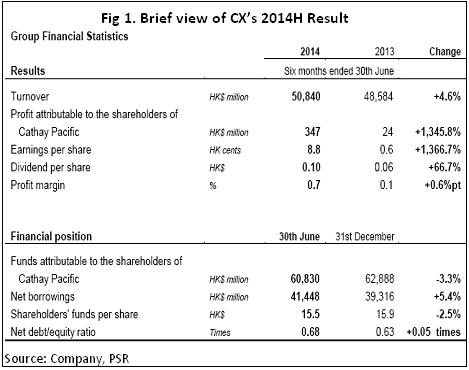

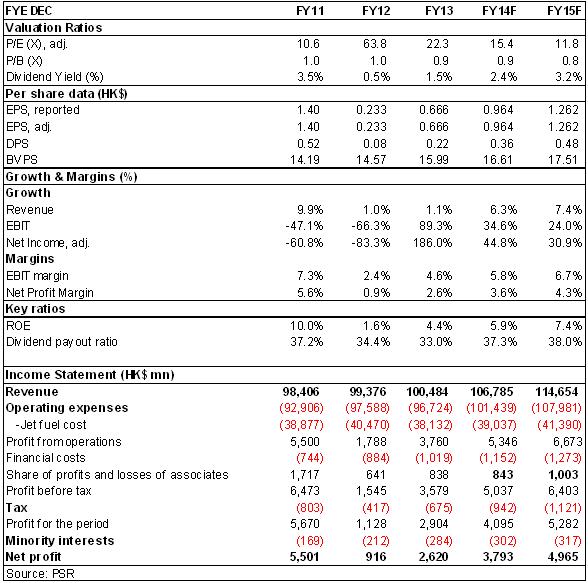

-The 1H turnover increased by 4.6%, reaching 50.84 billion Yuan. The net profit increases by 13.46 times yearly, reaching 347 million Yuan, with the earnings per share of 8.8 cents. Interim dividend per share stood 10 cents, slightly lower than our and the market's consistent expectation.

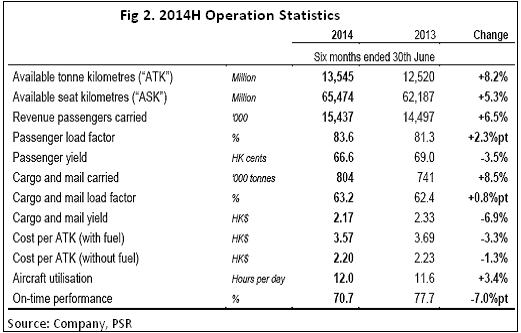

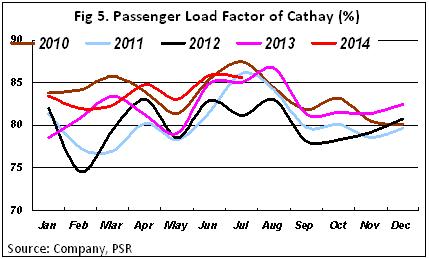

-On the whole, the passenger business tends to improve. The load factors increased by 2.3%, reaching 83.6%. The passenger volume rose by 8.3%. While the yield is under pressure all sidedly, dropping by 2.4 cents, reaching 0.666 Hong Kong dollars.

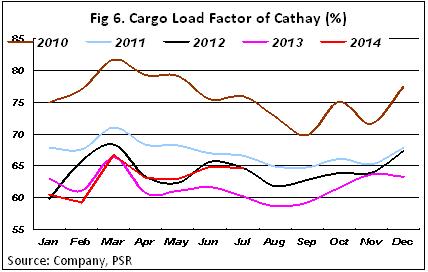

-Freight business keeps weak. The weight of carried cargos and mails increased by 8.5% yearly, reaching 8.04 billion tons. The cargo load factor slightly increases by 0.08%, reaching 63.2%. But the yield dropped by 16 cents or 6.9%, reaching 2.17 Hong Kong dollars.

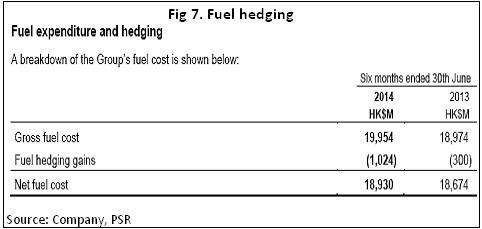

-Benefiting from 1.02 billion hedge earnings brought by the company's hedged operation when the oil price dropped, the ratio of net amount of fuel cost in the total operation amount decreased by 0.09%, reaching 37.9%, making the cost per ATK with fuel decreased by 3.3%, reaching 3.57 Hong Kong dollars, which significantly boosts the performance.

-The company recorded a loss of 265 million in investment earning, which is because that Air China, 20.13% of whose stock is held by Cathay Pacific Airways, is severely hit by the downturn of domestic industry and the depreciation of RMB exchange rate since the beginning of the year changing from appreciation.

How we view this

While from the middle of the year, the exchange rate of RMB begins to appreciate slightly. It is supposed to repair the exchange earning of Air China, so as to benefit the investment premium of the company to rebound in the second half year. However, the slowdown of domestic macroeconomic increase and the weakening of official business demand will be negative factors to restrict the thorough rebound of earnings of Air China. On the other hand, as the airline business enters the traditional peak period, there is space for the increase speed of the demand of international airline to continuously improve. For example, America routes will continue to benefit from American economic recovery; the demand for travels to Southeast Asian countries like Thailand is expected to recover with the political stability. The expectation should not be too high.

Investment Action

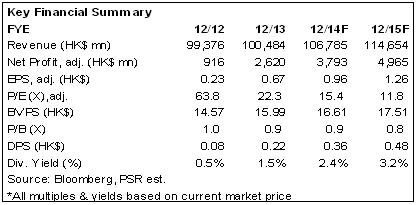

From the revised financial forecast, we revised our target price to HK$16.84, based on 17.5/13.3xP/E in2014/2015, and the suggestions of ¡§Accumulate¡¨ rating be given.

Earn 13.5 times more than before, reaching 350 million in the middle stage, but lower than expectation

Cathay Pacific Airways announced the performance of half a year by the end of June this year. The turnover increased by 4.6%, reaching 50.84 billion Yuan. The net profit increases by 13.46 times yearly, reaching 347 million Yuan, with the earnings per share of 8.8 cents. Interim dividend per share increased by 4 cents yoy, stood 10 cents. There is a clear rise in the performance (because the cardinal number of last year is very low), but the performance is still not reach our and the market's consistent expectation.

Passenger transportation demand continues to improve, only the yield is under pressure all sidedly

In the first half year, the company carried 15.437 million passengers, increasing by 6.5% yearly. The passenger volume rose by 8.3%. On the whole, the passenger business tends to improve. The load factors increased by 2.3%, reaching 83.6%. But all airlines performed differently: there is a great demand for tours from Hong Kong; a strong demand continuously appears in tours to North Asia (Japan, Korea and Taiwan), commercial business trips, students` trips and leisure trips to London, and airlines from North America. Due to local political unrest or fierce competition or other factors, airlines to and from Southeast Asia, South Africa, the Middle East, Canada, India, etc., are adversely affected. The yield is under pressure all sidedly, dropping by 2.4 cents, reaching 0.666 Hong Kong dollars. The load capacity of the first half year is 5.3% higher than that of the corresponding period of last year, reflecting the new airlines entering the market and the rising number of long-haul routes. Cathay Pacific Airways still maintains 6-7% for the load capacity increase index this year.

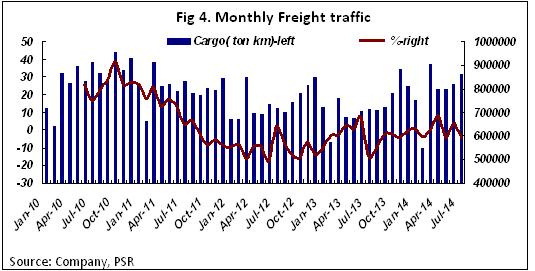

Freight business keeps weak

The freight business of the company has been weak since 2011. In this first half year, the weight of carried cargos and mails increased by 8.5% yearly, reaching 8.04 billion tons. The cargo load factor slightly increases by 0.08%, reaching 63.2%. But the yield dropped by 16 cents or 6.9%, reaching 2.17 Hong Kong dollars. The main reasons are excessive supply and increasing number of self-equipped freight carriers of logistic companies. In order to improve the efficiency, the company puts back 6 747-400F freight carriers. Now 13 747-8F freight carriers, which consume fuel more economically, are put into operation. New freight stations have started to handle goods for external customers since May. We expect that it will accelerate the lessening of loss in this business.

Hedging gains assisting the percentage of fuel cost continues to decrease

Benefiting from quickening the decommissioning of old types and introducing new types of better fuel efficiency, the total volume of fuel cost increased by 5.2% compared to the same period, lower than the rate of increase in passenger capacity and load capacity. What's more, benefiting from 1.02 billion hedge earnings brought by the company's hedged operation when the oil price dropped, the ratio of net amount of fuel cost in the total operation amount decreased by 0.09%, reaching 37.9%, making the cost per ATK with fuel decreased by 3.3%, reaching 3.57 Hong Kong dollars, which significantly boosts the performance. The hedging will last till 2017. For this year and next year, hedge ratio is about 44-47%. In 2016 and 2017, it will be about 25%. The benefit of cost control of the company continues to appear, out of a 0.9% decrease of cost per ATK without fuel, which is 2.16 Hong Kong dollars.

The investment premium from Air China is expected to bounce back

In the period, the company is recorded a loss of 265 million in affiliated company, which is the worst since the financial crisis in 2008. The performance of Air China, 20.13% of whose stock is held by Cathay Pacific Airways, is severely hit by the downturn of domestic industry and the depreciation of RMB exchange rate since the beginning of the year changing from appreciation. It is a negative impact on the investment premium of the company. While from the middle of the year, the exchange rate of RMB begins to appreciate slightly. It is supposed to repair the exchange earning of Air China, so as to benefit the investment premium of the company to rebound in the second half year. However, the slowdown of domestic macroeconomic increase and the weakening of official business demand will be negative factors to restrict the thorough rebound of earnings of Air China. The expectation should not be too high.

Valuation and Rating

As the airline business enters the traditional peak period, there is space for the increase speed of the demand of international airline to continuously improve. For example, America routes will continue to benefit from American economic recovery; the demand for travels to Southeast Asian countries like Thailand is expected to recover with the political stability. The risk of going down lies in the remaining fierce industrial competition, or the pressure posed by the improvement of yield. After overall consideration, according to the latest earnings predict, we adjust the target price of the company of 12 months to 16.84 Hong Kong dollars, corresponding to 17.5/13.3 times of 2014/2015 prospective PE ratio, 1.0/1.0 times of prospective price-to-book. The valuation is at a historically low level, reiterating "accumulate" rating.

Click Here for PDF format...