-Forgame issued a negative profit alert on July 17, which expected to have a net loss of RMB 15Mn to RMB 25Mn for 1H14. The profit warning was mainly due to decreasing revenue from its existing matured web games, while cost and expenses remained heavy.

-The company scheduled to have 12 web games and 12 mobile games for 2014 in the beginning of this year. But we are disappointed to find that no any one new product has been launching in the first half.

-The acquisition of Magic Feature Inc. (developer of Tower of Saviors) had encountered obstruction and self-developed mobile games underperformed that made the transformation lagged.

-We downgraded the rating to ¡§Neutral¡¨ with target price reduced to HK$ 18.97, equivalent to 7.5x of 2015 forecasted EPS plus cash per share of HK$ 11.72.

Financial Highlights

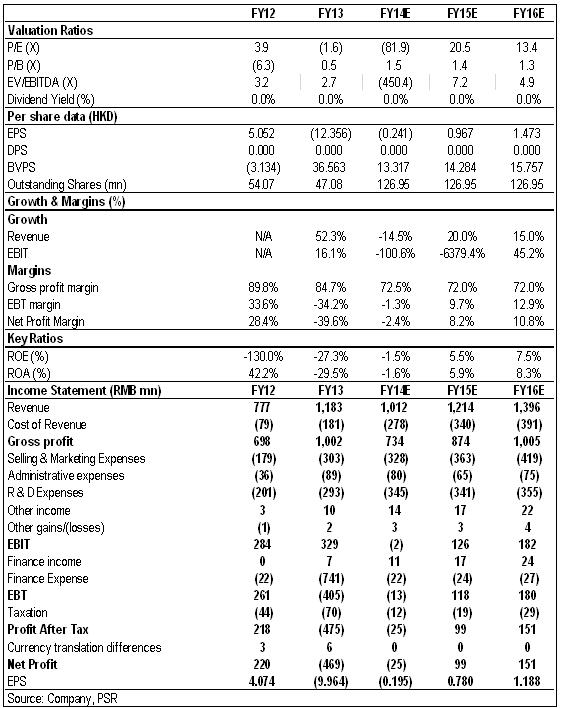

Forgame issued a negative profit alert on July 17, which expected to have a net loss of RMB 15Mn to RMB 25Mn for 1H14. According to the announcement, the profit warning were due to 1) maturity of existing web games led to decrease of revenue; 2) missing of new web games in 1H since the company strategically delayed the launching; 3) the cost and expenses retained even revenue dropped. The company remarked that the net loss is comparatively lower than 1H13. However, when the non operational fair value adjustment on preference share was excluded in 1H13¡¦s calculation, it showed an even larger loss yoy.

How we view this

We are disappointed with Forgame¡¦s poor performance in 1H14. In the last report, we expected the company to accelerate the new game launching to existing huge customer base, especially the planned 12 new games adding to existing 6 mobile games this year. However, not to say the mobile business which was still a new area for the company, it even failed to publish any one new web game in order to maintain the web game launching speed, which was expected to be its strength. With the average product life of 12-24 months for web game, its existing web games would certainly losing attraction to the customers.

Investment Action

We expected Forgame will continue to lag behind its schedule. It is still a doubt whether the company can launch half of its 2014 target in 2H. Thus, We cut the previous estimated revenue and remain the cost and expenses on the company. Take reference from the lowest PE of Nasdaq listed MMORPG company of 7.5x, the business value for 2015 forecasted EPS is HK$ 7.25. With cash per share of HK$ 11.72, we downgraded the rating to ¡§Neutral¡¨ with target price reduced to HK$ 18.97.

Performance missed expectation

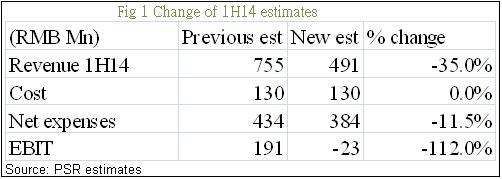

After Forgame¡¦s negative profit alert, we lowered the 1H14 forecasted revenue by 35% to RMB 491Mn. The forecasted 2014 revenue also cut by 35.7% to RMB 1.012Bn. While retaining the cost and lowering the expenses a bit, the calculated EBIT sharply slumped to negative.

Revenue expected to slightly go up due to summer holiday effect, refer to last year

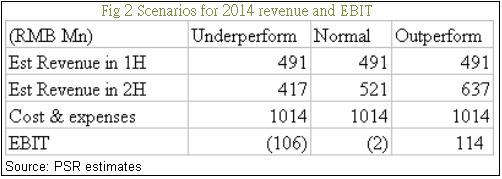

In normal case, assuming no other growth momentum and further drop of existing client contribution, revenue is expected to grow slightly in the 2H due to seasonal effect of summer holiday. However, if the operating situation continued to worsen, EBIT could have a sharp plump down to over RMB 100Mn.

Missing new game launching in 1H14

The company scheduled to have 12 web games and 12 mobile games for 2014 in the beginning of this year. However, no any one planned new product has been launching in the first half, not even the web games previously working on progress. Since the average product life for web game was about 12-24 months, delay in launching new games could break the company¡¦s cash flow.

Acquisition of Magic Feature Inc. had encountered obstruction

The comapny announced in 1Q14 to acquire the mobile game developer Magic Feature Inc. which had successfully published the famous mobile game ¡§Tower of Saviors¡¨. However, Forgame had further announcement on May 19 that the acquisition may not be proceeded. Without ¡§Tower of Saviors¡¨ to act as a flagship game of entering the mobile game industry, the company needs to develop or acquire another pop game, which is certainly a challenge.

Self developed mobile games underperformed

Forgame used to develop web games and was the leader in the industry. However, the development of mobile game is different from web game. The company planned to simply transform its web games into mobile interface may find it difficult to please the mobile users. Besides, the company had also shifted some manpower from the web team to work on mobile game development. There was a high probability for the team to suffer from bottleneck in developing.

Potential Risks

The revenue diminishing on web games speeds up;

The company is unable to transform to mobile game area;

Click Here for PDF format...