|

|

|

*Advertisement* |

|

|

|

|

|

25 Jul, 2014 (Friday) |

KANGDA ENV(6136)

Analysis¡G

Kangda (6136), which just listed this month, announced the acquisition 100% equity of Guodian Langxinming Puyang Water with RMB 56.88 million. The company is principally engaged in the investment in sewage treatment infrastructure, and has franchise right of BOT project of Puyang second sewage treatment plant. The daily capacity charged for the sewage treatment plant is 50,000 tons per day. Through this acquisition, the Group can expand its sewage treatment business in China. Share price rose as high as $3.37 after the listing, has recently pulled back to $2.8 IPO price level. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $2.85, Target Price: $3.10, Cut Loss Price: $2.70

|

|

HKEX(388)

Analysis¡G

Benefited by the macroeconomic and market prospects become more stable in mainland, and the HK - Shanghai connect that will be implemented in the second half, HKEx (388) will gain from enhance the long-term of trading volume. Analysts generally believed the limit amount of the HK - Shanghai connect will gradually increase, while HKEx linkages with the other mainland exchanges will gradually expand, for example, if the HK - Shanghai connect is running smoothly, the Shenzhen Stock Exchange may also have the intention to set up exchange connect mechanism. In addition, since the HK - Shanghai connect is working through a revenue sharing arrangement, HKEx will also benefit from the transaction in the Mainland, and the overall trading volume should rise.

Strategy¡G

Buy-in Price: $158.00, Target Price: $170.00, Cut Loss Price: $153.00

|

| |

|

Brilliance China (1114.HK) - Accelerated segmentation product strategy

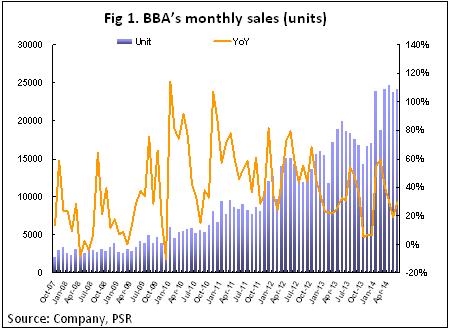

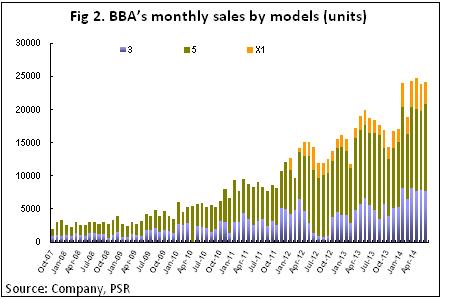

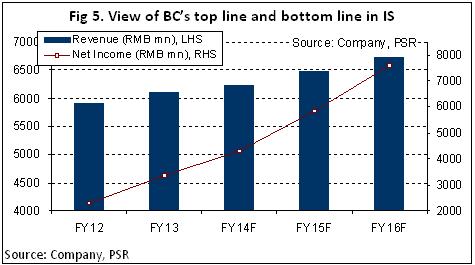

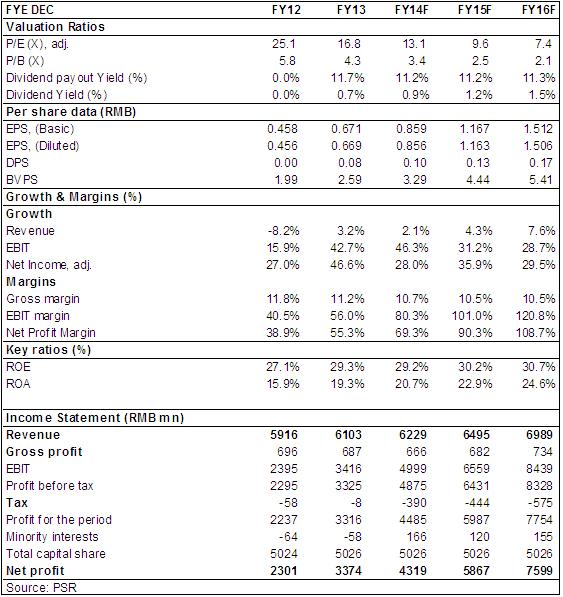

-Strong growth for BBA 1H2014: Owning to the continuing effect of capacity release, BBA (Brilliance BMW) delivered 140 thousand cars in the first half of 2014, a year-on-year increase of 37%, out of which SUV model X1 increased by 107% year-on-year to 22 thousand, X3 increased by 55% to 46 thousand, and X5 increased by 51% to 71 thousand. The company's sales goal in 2014 is 260 thousand cars, a 30% year-on-year increase, and in half a year it has achieved 53.8% of the sales goal for the year. Since the capacity of Dadong factory for production of series 5 has been approaching its limit, we believe in the coming one-year BBA's sales increase will be mainly contributed by series 3 and X1. -JV Contract renewal in advance is expected to eliminate uncertainty: 4 years ahead of the expiration of the joint venture contract, BMW Group and the company have announced recently that joint venture contract would be extended to 2028; this move is expected to eliminate the uncertainty of the source for future profitability, and is conducive to the introduction of new BMW models and their technologies, which is beneficial to the company's stock performance and the level of valuation. -Accelerated segmentation product strategy: BMW Group has issued the guidance on the future planning of Chinese market, including: 3 new models will realize localized production in China; Continue to increase the total capacity of BBA's Dadong factory and Tiexi factory in Shenyang; BMW¡¦s 3-cylinder and 4-cylinder gasoline engines are going to be put into production in China in 2016. It is learned that the 3 new models for domestic production in future are respectively BMW 2X Active Tourer van, BMW X3 and one new entry-level model lower than the level of X3, which will increase the vehicle types of domestic production in China from currently 3 models to 6 models. For SUV model X3, the wheelbase will be extended, which is more likely to meet the vehicle purchase needs of domestic consumers at present, and the future performance is worthy of expectation. After the completion of BBA's new engine plant, production of advanced 3-cylinder and 4-cylinder gasoline engines will be officially started in 2016, which will positively improve the capacity and quality of BBA.

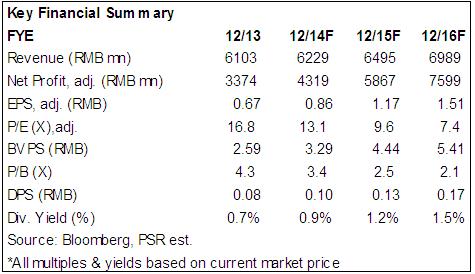

How we view thisWe believe that, after experiencing the explosive growth in past few years, the increase rate of China's luxury car market begins to slow down, with structure-based and pluralism market development trend becoming apparent, so BMW's accelerated introduction of segmentation products is conducive to continuous development of new segment markets. Investment ActionAccording to above, we revised our target price to HK$16.45, based on 15/11/8.5xP/E in2014/2015/2016, which we believe is rational considering its high ROE and fast growth ahead among peers, and the suggestions of ¡§accumulate¡¨ rating be given.

Click Here for PDF format...

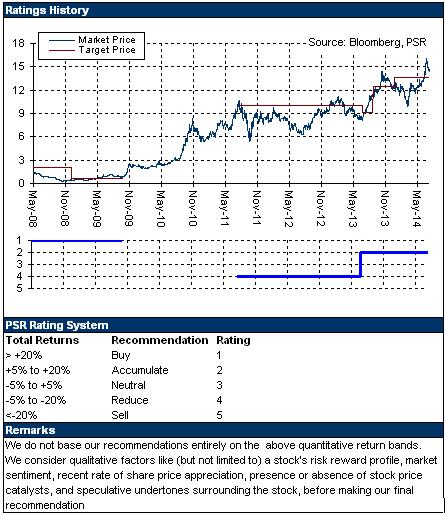

| Recommendation on 25-7-2014 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 14.320 | | Suggested purchase price | N/A | | Target Price | $ 16.450 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | CITIC Securities | 6030 | 23/07/2014 | Buy | 22.3 | 18.18 | | Hanhua Financial Holding | 3903 | 15/07/2014 | Buy | 2.5 | 1.52 | | | Brilliance China | 1114 | 25/07/2014 | Accumulate | 16.45 | 0.000 | | Dongfeng Group | 489 | 17/07/2014 | Accumulate | 16.5 | 14.6 | | | NEW WORLD CHINA LAND | 917 | 19/06/2014 | Accumulate | 5.5 | 5.12 | | Wanda Commercial Properties Group | 169 | 12/06/2014 | Neutral | 2.6 | 2.5 | | | | China State Construction International Holdings Ltd | 3311 | 16/05/2014 | Buy | 15.8 | 13.16 | | Hysan Development | 0014 | 18/03/2014 | Accumulate | 36.8 | 33.35 | | Hotels and Entertainment | | N/A N/A | N/A |

| | Galaxy Entertainment | 27 | 16/07/2014 | Accumulate | 72 | 62.95 | | Galaxy Entertainment Group | 27 | 16/04/2014 | Accumulate | 78 | 68.7 | | | Singyes Solar | 750 | 22/07/2014 | Buy | 14.96 | 11.34 | | Jingneng Clean Energy | 579 | 08/07/2014 | Buy | 5.1 | 3.74 | | | Anta Sports | 2020 | 18/07/2014 | Accumulate | 13.31 | 12.46 | | Bolina | 1190 | 05/06/2014 | Accumulate | 3.23 | 2.87 | | | China Communication Service Co., LTD. | 552 | 21/07/2014 | Buy | 4.7 | 3.87 | | Sunny Optical | 2382 | 04/07/2014 | Accumulate | 11.8 | 11.04 | | | SPT Energy | 1251 | 27/06/2014 | Accumulate | 4.6 | 4.2 | | Anton Oilfield Services Group | 3337 | 25/04/2014 | Accumulate | 6.2 | 5.29 | | | Tencent Holdings | 700 | 24/07/2014 | Accumulate | 136 | 124.3 | | ZTE Corporation | 763 | 14/07/2014 | Buy | 21 | 14.78 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2014 Phillip Securities (HK) Ltd. All Rights Reserved.

|