|

|

|

*Advertisement* |

|

|

|

|

|

23 Jul, 2014 (Wednesday) |

MOBI DEV(947)

Analysis¡G

MOBI Development (947) issued profit alert, which expected the consolidated net profit for 1H14 to increase significantly yoy. This was mainly benefit from the 4G construction of the 4G network operators that significantly increased the sales of 4G-related products to China 4G network equipment providers and system operators. Besides, the Group`s sales to major customers have shown positive growth in cross products selling, coupled with the effective control of the company selling and distribution expenses, and general and administrative expenses, which pumped up the net profit in the first half. China Mobile (941) planned to strengthen the 4G network construction, by building more than 500,000 4G network base stations during the year. Moreover, the MIIT had issued the FDD trial license to China Telecom (728) and China Unicom (762) last month, permitting them to integrate the 4G networks in 16 cities, this will accelerate their construction speed of base stations, which will favor MOBI. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $1.75, Target Price: $1.95, Cut Loss Price: $1.65

|

|

GOME(493)

Analysis¡G

Gome (493) issued positive profit alert yesterday, which expected 1H14, ended June 30, net profit for general business will increased significantly to more than 80%, forecasted net profit margin will exceed 2%. If a non-recurring income was including in calculation, net profit for the first half will significantly grow over 110%. Company noted that the improved performance was mainly due to forecasted revenue growth in comparable store sales exceeded 7% and the total transaction volume of e-commerce is expected to grow more than 50% yoy with forecasted consolidated gross profit margin exceeded 18%. The Group noted that it will continue to build the "all channels" operating platforms as the core of the business model. Actually, the e-commerce development of the Group had been lagging behind, compared to the peers, which put its share price under pressure these two years. It is expected the above business will have good performance starting from this year, with its vast physical networks, the share price is expected to return to historical level in the long run.

Strategy¡G

Buy-in Price: $1.28, Target Price: $1.45, Cut Loss Price: $1.24

|

| |

|

CITIC Securities (6030.HK) - The industry leader with better-than-expected profit performance in 1H2014

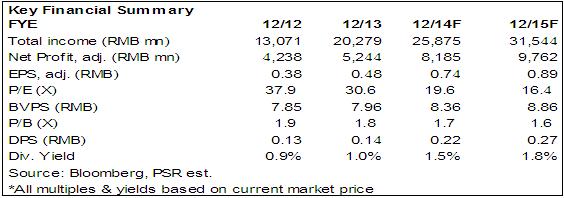

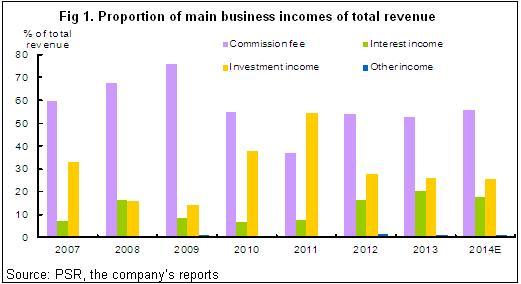

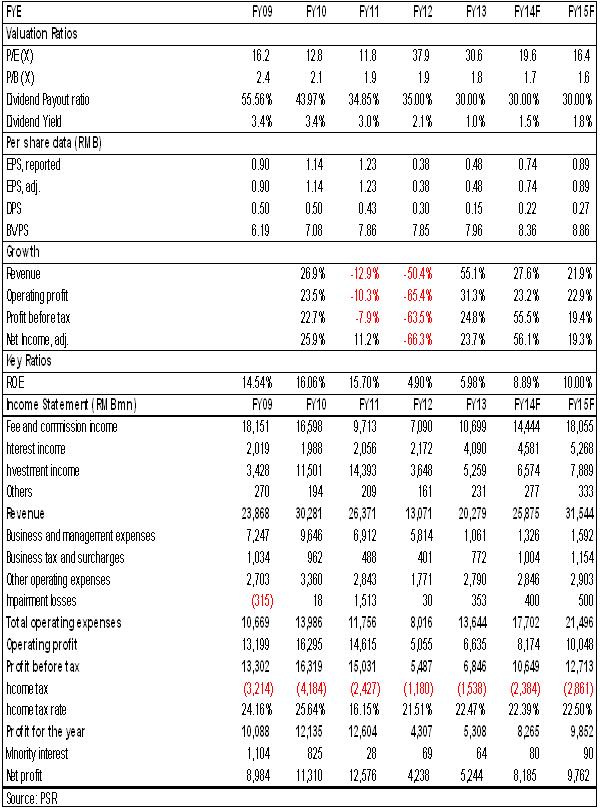

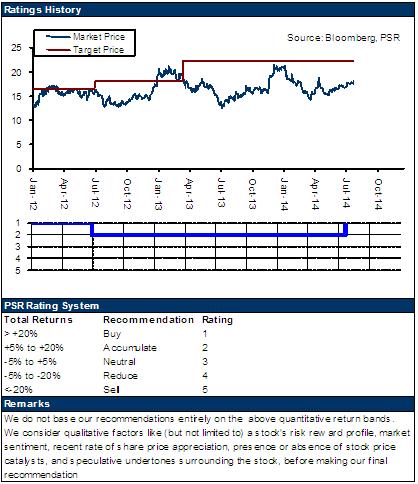

-According to the preliminary result of CITIC Securities (¡§CS¡¨ or ¡§the Group¡¨) announced yesterday (21st Jul), in 1H2014, profit for the year of CS increased significantly by 114.35% y-y to RMB5, 824 million with net profit of RMB4,076 million, up 93% y-y approximately; -Total assets increased strongly by 25.2% to RMB33.9747 billion compared with the end of 2013, and the BVPS was RMB8.14, up 2.3% during the same period; -The large profit growth of CS is mainly due to the increase in the number of companies that was consolidated to CS¡¦s financial statements, and non-recurring operating gains grew significantly because of the transfer of the entire equity interests in its wholly-owned subsidiaries of Tianjin Jingzheng Property Services Limited and Tianjin Shenzheng Property Services Limited to CITIC Qihang Securities Investment Private Fund; -Due to the strong market demand, CS¡¦s businesses recovered obviously in the recent two years, and the profit growth is stronger than our expectation according to the performance in 2013 and 1H2014, however, considering the increase of the market volatility and the Group¡¦s operating expenses in future, we maintain CS¡¦s 12-month target price on HK$22.30, 22.7% higher than the current price, equivalent to 20.3xP/E and 2.0xP/B in 2015E respectively. Upgrade to Buy rating. How we view this CS is the largest securities company in China with the leading position in the industry, especially the Group¡¦s innovative business experienced strong development. The commission fees and investment incomes increased strongly in the recent two years because of the recovery of domestic capital market. The commission fee grew largely 50.9% and 110.4% y-y respectively in 2013 and 1Q2014, and we expect such income would increase by 100% y-y approximately in 1H2014, but the Group¡¦ profit should be lower than that of 2009. Investment ActionCurrently the market environment trends to be positive, we believe there are large development of the market environment if the cross-border trading between Shanghai and Hong Kong could be implemented successfully in this Oct, investments will become more active, and we hold the optimistic view on CS¡¦s future development based on the leading position in the industry, its incomes will maintain strong growth, and therefore we maintain CS¡¦s 12-month target price on HK$22.30, 22.7% higher than the current price, equivalent to 20.3xP/E and 2.0xP/B in 2015E respectively. Upgrade to Buy rating.

RiskLarger-than-expected decrease of commission fees; Investment gains declined strongly; Share decrease of share price affected by the market environment.

Click Here for PDF format...

| Recommendation on 23-7-2014 | | Recommendation | Buy | | Price on Recommendation Date | $ 18.180 | | Suggested purchase price | N/A | | Target Price | $ 22.300 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

| Phillip Research - Hong Kong ½÷¥ß¬ã¨s³¡ ¡V »´ä¤Î¤¤°ê |

| Company |

Stock Code |

Last Update |

Suggestion |

Target Price |

Price on Recom |

| | CITIC Securities | 6030 | 23/07/2014 | Buy | 22.30 | 0.000 | | Hanhua Financial Holding | 3903 | 15/07/2014 | Buy | 2.5 | 1.52 | | | Dongfeng Group | 489 | 17/07/2014 | Accumulate | 16.5 | 14.6 | | GAC Group | 2238 | 10/07/2014 | Accumulate | 10 | 9.42 | | | NEW WORLD CHINA LAND | 917 | 19/06/2014 | Accumulate | 5.5 | 5.12 | | Wanda Commercial Properties Group | 169 | 12/06/2014 | Neutral | 2.6 | 2.5 | | | | China State Construction International Holdings Ltd | 3311 | 16/05/2014 | Buy | 15.8 | 13.16 | | Hysan Development | 0014 | 18/03/2014 | Accumulate | 36.8 | 33.35 | | Hotels and Entertainment | | N/A N/A | N/A |

| | Galaxy Entertainment | 27 | 16/07/2014 | Accumulate | 72 | 62.95 | | Galaxy Entertainment Group | 27 | 16/04/2014 | Accumulate | 78 | 68.7 | | | Singyes Solar | 750 | 22/07/2014 | Buy | 14.96 | 11.34 | | Jingneng Clean Energy | 579 | 08/07/2014 | Buy | 5.1 | 3.74 | | | Anta Sports | 2020 | 18/07/2014 | Accumulate | 13.31 | 12.46 | | Bolina | 1190 | 05/06/2014 | Accumulate | 3.23 | 2.87 | | | China Communication Service Co., LTD. | 552 | 21/07/2014 | Buy | 4.7 | 3.87 | | Sunny Optical | 2382 | 04/07/2014 | Accumulate | 11.8 | 11.04 | | | SPT Energy | 1251 | 27/06/2014 | Accumulate | 4.6 | 4.2 | | Anton Oilfield Services Group | 3337 | 25/04/2014 | Accumulate | 6.2 | 5.29 | | | ZTE Corporation | 763 | 14/07/2014 | Buy | 21 | 14.78 | | OURGAME | 6899 | 11/07/2014 | Accumulate | 4.1 | 3.75 |

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2014 Phillip Securities (HK) Ltd. All Rights Reserved.

|