Company Profile

China Southern Airlines (CSA) is one of China's Big-3 Carriers and a member of the SkyTeam. CSA owns 440 Boeing and Airbus planes currently. With the headquarters located in Guangzhou, CSA is the largest airline for the domestic passenger volumes. It listed in HKEx in 1997 and SSE in 2003.

Summary

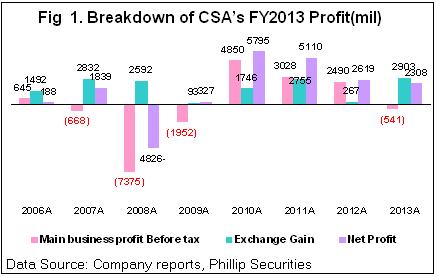

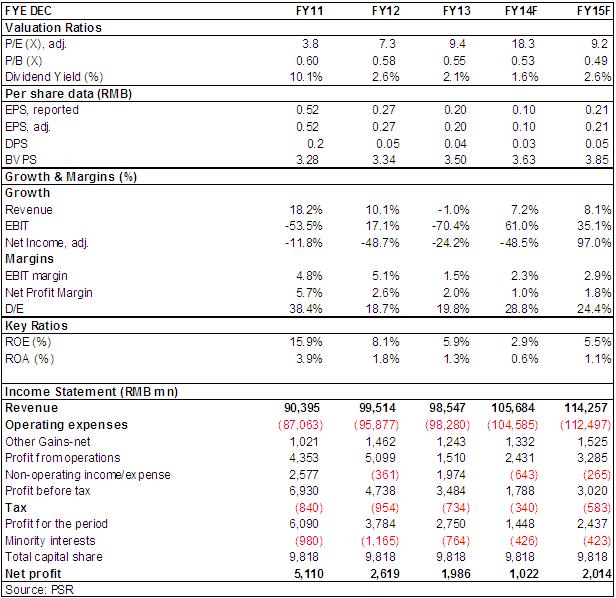

-Net profit dropped 24% in 2013: CSA announced 2013 results recently (Based on IFRS), the Company's revenues amounted to 98.5 billion (RMB, similarly hereinafter), down 1% y-y, operating expenses increased by 2.5% y-y. Net profit attributable to the equity holders of the company recorded 1.896 billion, down 24.2% y-y, with the EPS of 0.2 and the DPS of 0.04, the dividend payout ratio was around 20%.

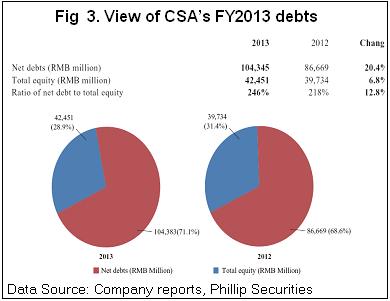

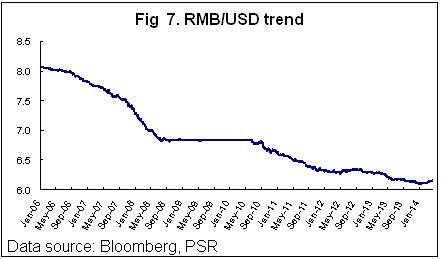

-Main businesses turned into losses from profits: Excluding newly added exchange gains of 2.6 billion due to the appreciation of RMB, and the additional asset impairment loss of 0.54 billion, the profit before tax of the Company's main businesses turned in losses from profits, our adjusted real EPS was -0.03, nonrecurring items such as exchange gains play the key roles of the final profit contribution. Due to the growth of financing, debt to equity ratio located at quite high level, and trended to go up, net debt to equity increased from 218% last year to 246%, we expect the capital interest expenses will face large pressure in future.

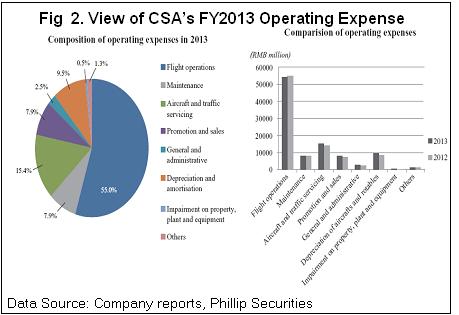

-The volume rose with the non-increase of revenues due to the decrease of ticket price: CSA's passenger traffic volume in 2013 increased by 9.5% y-y, but the Company's volume rose with the non-increase of revenues due the large decrease of flight ticket price of the industry. On the other hand, the control of the capacity lags behind the changes of demand, and the Company's profitability is damaged due to the relative rigidity of costs. Under the decrease of 1.2% in the fuel cost, the Company's main operating expenses increased by 2.5% to 9.83 billion compared with the end of 2012, the operating expenses of flights (excluding fuel cost) grew by 6.8%, aircraft and transportation expenses and depreciation increased largely, up 15.4% and 9.5% y-y respectively, moreover, net interest expense increased by 17.8% y-y to 1.34 billion due to the growth of liabilities.

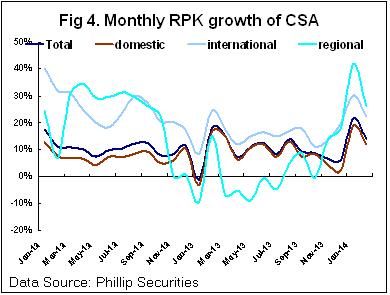

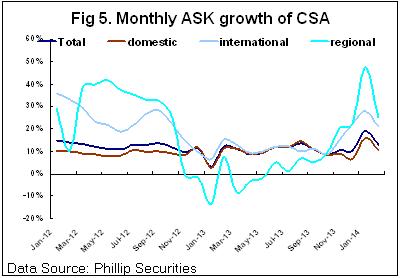

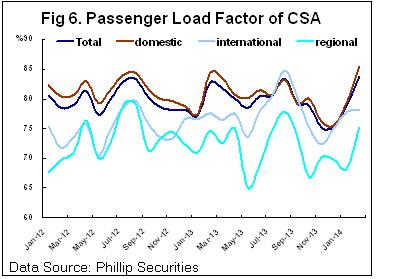

-Operating data was worse than the peers: CSA's yield per RPK dropped from 0.68 in 2012 to 0.59, lower than Air China's 0.62 and CEA's 0.6. The Company's passenger capacity increased by 10.2%, and the load factor decreased by 0.6ppts y-y to 79.5%, higher than CEA but lower than Air China. According to routes, in terms of RPK, the volume in domestic, regional and international routes increased by 8.2%, 1.5%, 15.6% respectively, and load factors decreased by 1.2, 1.6 and up 3ppts to 80.2%, 71.6% and 77.3%. Yield per RPK recorded 0.61, 0.84 and 0.5 respectively. CSA obviously located at the weaker position under the industrial demand structure of ¡§weaker internally, and stronger externally¡¨ due to its larger proportion in domestic routes.

-No bright points fundamentally: CSA's capacity will stay at the high level in the next two years because of the previous aircraft orders. As for the demand, there is a small possibility that the price level trends to go up in domestic routes under the improvement of the relationship between the demand and supply due to the sluggish economic growth, the continued limitation in the consumption of public funds from the government, and the pressure of the outflow of short-medium haul passenger to the high-speed railways. CSA's international routes, including the rapid expanded route in Australia in recent years, are still facing the fiercer competition to try to gain the market shares, and the profitability needs to be further improved. Overall, there are no bright points fundamentally.

-Negative impacts: CSA's debt to equity ratio in USD recorded as high as 96%, the profits has the large elasticity of the changes of RMB exchange rate. Predictably, the previous ¡§profit contributor¡¨, exchange gains, will transfer to ¡§profit killer¡¨ due to the depreciation of RMB in 1Q2014. The company just predicted its FY2014Q1 EPS to -0.03-0.036.

-Possible activators: The possible authorization of wide-bodied aircraft A380 in international routes will bring the improvement of the utilization efficiency.

Large capital injection from the government

The improvement of the company's operating efficiency due to the reform of state-owned enterprises.

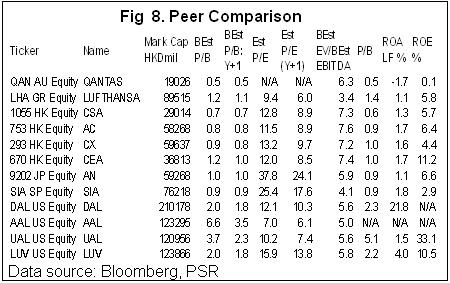

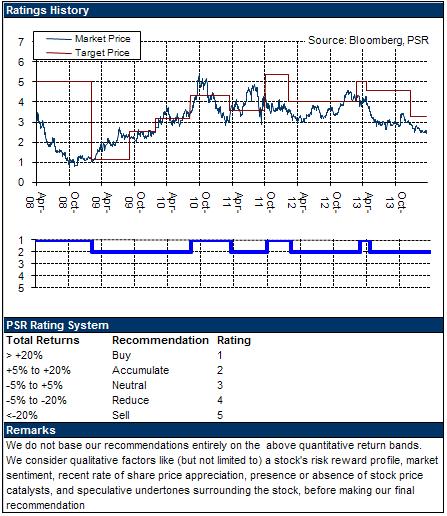

-Valuation and rating: We cut the Company's estimated EPS to 0.10, 0.21 in 2014/2015 respectively. Though its valuation still owns safety margins to some extent as the current P/B locates at the historical trough, there is a limitation of the price increase under weak fundamentals. Our 12-m-target price is HK$2.6, implying an upside potential of 7%, equivalent to 0.56/0.53xP/B, and 19.6/9.9xP/E for 2014/2015 respectively. We recommend Accumulate rating.

Click Here for PDF format...