Summary

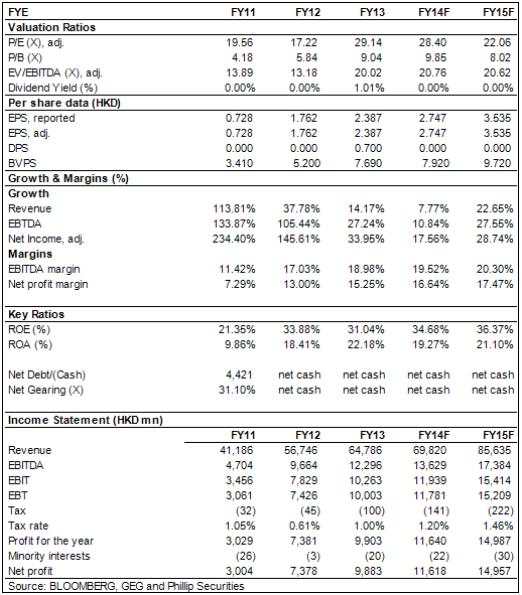

Thanks to the increase in gaming revenues of Galaxy Macao and Star World Macao, the company has earned HKD 66.032 billion in 2013, a 16.4% growth compared with the same period of last year.

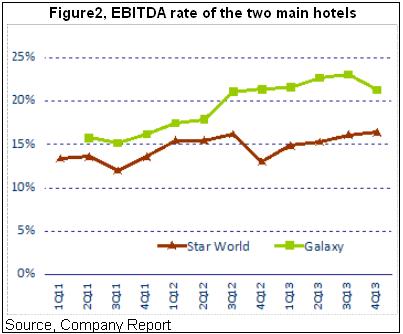

For the whole year, the adjusted EBITDA of the company has a 28% growth on a year-on-year basis to HKD 12.58 billion . This is mainly due to the significant rise of 36% in the adjusted EBITDA of Galaxy Macao, which led a steady development of the group. In 2013, the profit attributable to shareholders has increased by 36.2% on a year-on-year basis to HKD 10.05 billion . The company announced to giving a special dividend of 0.7 HKD per share.

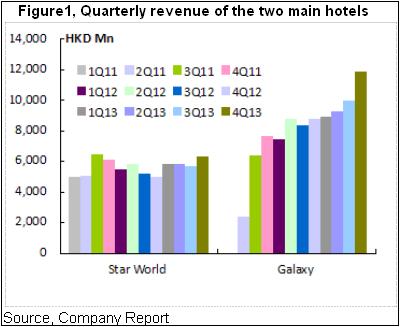

Galaxy Macao is located in the Flagship Resort of Cotai region. Its period's earning was HKD 40 billion , a 21% growth year on year, and accounted for 60.6% of the gross revenue. Therein, the gaming revenue of VIP hall has increased to HKD 26.5 billion , a 15% growth year on year; the revenue of center field has soared to HKD 10.46 billion , a 44% growth year on year; and the revenue of the slot machine has added to HKD 1.52 billion , a 25% growth year on year. In addition, the non-gaming revenue of Galaxy Macao has reached HKD1.5 billion , which is basically flat with that of 2012. During the period, the average occupancy rate of three five-star hotels in the resort is 98%.

The annual revenue of Star World Macao¡X¡Xanother core project of the company¡X¡Xhas increased to HKD 23.5 billion , a 9% growth year on year, which accounted for 35.6% of the total revenue. This mainly resulted from the excellent performance of the center field business. During the period, the gaming revenue of VIP hall has increased by 4% to HKD 19.08 billion ; the center field has soared by 59% year on year to HKD 3.86 billion ; while the slot machine has decreased by 15% year on year to HKD 0.21 billion . Furthermore, during the period, the non-gaming revenue has decreased by 12.5% year on year to HKD 0.364 billion; while the occupancy rate has still maintained at 99%.

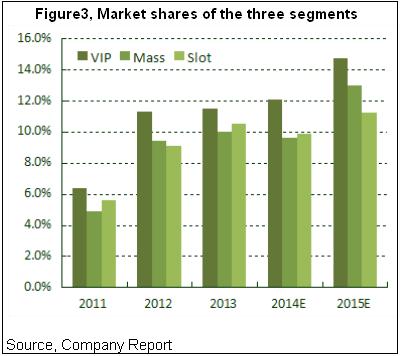

Last year, the revenue of the fourth quarter as well as EBITDA increased by 16% and 10% quarter on quarter to 18.9 billion and 3.55 billion respectively, consistent with the market expectation. Overall, the market share of the fourth quarter in 2013 has risen from 0.6% to 19.1%. In the first two months of 2014, the market share has increased further to 20.6%.

The open-up of the second phase of Galaxy Macao will hopefully lead to another torrent of business increasing. However, the growing rate is expected to be slower than that of the first phase because of the industry factor that the growing rate of gaming revenue of Macao will fall back to normal. The third and fourth phase of Galaxy Macao as well as the vacation project of Hengqin Island will become the source of profit-growing in the middle of this year.

We believe that Galaxy Entertainment Group is the best choice of gaming stock of Macao owing to its excellent power of execution of the management, relatively high asset quality and energetic mid-and-long term profit growing force. On account of its continued positive development, the further decreased liability and our long-term optimistic expectation of the future of the company, we give the group the rank of "Accumulate", and the target price of 78 HKD of 12 months which equals to 24.6 times of the anticipated PE ratio of 2014.

Click Here for PDF format...